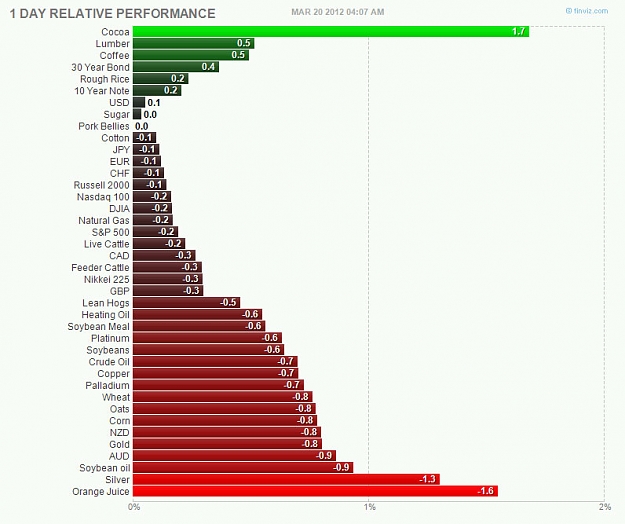

Well, we know Asia will drive price higher. I'm looking to short at the top of the channel 1.328. Based on Euro session confirmation

Ignored

Price could possibly retrace back to resistance turned support on EU/US.. The USDX is showing a strong chance of retracing back to resistance before heading for support at 79.1

I have multiple personalities... Bull today Bear tomorrow!

I've noticed that talking-forex.com and forexlive.com are disinformation websites that function for one of the biggest banks/brokers in the world. My first guess is BIS (something Jonahky has mentioned many times) . I've been monitoring these 2 web sites for a long time now.

Here's a typical sampling of how they operate. The following are posts in the News section of FF from March 19th:

"Fed's Fisher: no one presently believes that the Fed are going to proceed with Q3." talking-forex.com.

The MOMENT this was released price sat at 3150 and the buyer started to come into the market for its 110 pip move. Here was my timestamped comment telegraphing the move!:

Post #1 me: "heh I guess they are planning on buying euros in an hour or so...pretty sure this statement is like a month old."

Post #2 GUEST: "don't buy...euro drop to 1.3000 for today."

As you can see I predicted the rise in price of the euro based upon trading contrary to this disinfo site and their propaganda. Post #2 is typical of how this web site acts. They will try to reinforce their posts by posting as guests to reinforce traders moving in the wrong direction of the big move about to play out. This idiot calls for 1.300 at the very moment I cast doubt on this web site even as price is about to skyrocket to 1.326. This person works for talking-forex.

FF knows full well the type of practice this website and forexlive engage in, and they are never going to censor it, but you can profit off trading against these web sites by careful observing the language in relationship to price action and recent moves in the market. These guys practically give away their moves by telegraphing signals on the internet opposite of their true intentions. Sometimes they throw out false signals, but the vast majority of the time they always telegraph the opposite of what they are going to do.

After the move has broken first resistance they try to offer some completely bullshit explanation for the move through another one of their website affiliates: forexlive. This post is also found in the News section:

"CHF buying tips dollar slump" forexlive.com

First off, the talking-forex post was a repaste of something Fisher said in April. Secondly, if you observe the price action of CHF and EUR against the USD on a minute time chart, you can clearly see that both moved in tandem--at the same time. Every non-idiot in forex knows that big moves against the dollar synchronized with the EURUSD are moving BECAUSE of the EURUSD.

So why do they even bother offering such bullshit explanations to cover the real cause of the move?--That a REAL BIG PLAYER, most likely the BIS, is buying euros today despite crap news, crap fundamntals, and crap liquidity throughout March. They do this to create more confusion and misunderstanding in the average trader about WHY these moves REALLY occur.

You can call this a conspiracy theory if you like, but if I bothered I could show you many many instances where major moves occured perfectly timed with the disinformation released by these dishonest lying web sites. There is no doubt in my mind the entire global financial game is completely corrupt and manipulated. The fact that these web sites are operated by one of the biggest money movers in the world is obvious to anybody that researches them long enough.

I cannot offer you a perfect system for trading these web sites "feeds," but by creating general awareness perhaps you can hone your skills at comprehending what these web sites are really saying and position yourselves for the big moves that happen sometimes. These guys are PROFESSIONALS and they are very clever. Don't be fooled and think this is easy to do. They will throw out false leads and false signals to confuse you. Some of the releases are just bluffs while others signal major moves are about to happen.

If you think everything I just said is bullshit, just remember I predicted a 100 pip move today based upon trading contrary to these manipulators and liars. Exercise extreme caution when you trade around releases these guys issue, especially when the market is trading in low liquidity around low news. These guys blow through technicals and fundamentals.

I've noticed that talking-forex.com and forexlive.com are disinformation websites that function for one of the biggest banks/brokers in the world. My first guess is BIS (something Jonahky has mentioned many times) . I've been monitoring these 2 web sites for a long time now.

Here's a typical sampling of how they operate. The following are posts in the News section of FF from March 19th:

"Fed's Fisher: no one presently believes that the Fed are going to proceed with Q3." talking-forex.com.

The MOMENT this was released price sat at...

Ignored

DailyFX is another Great detective work!

I have multiple personalities... Bull today Bear tomorrow!

Due to the WAY the daily chart descended last week and bounced strongly on Friday, my bias, after a short rejection around 1.33, remains to the upside. I am unable to see a daily H&S formation forming next, as I am unable to see what could change my bias for the moment. Future candles need to be drawn before finding new reasons…As of now, I am in favor of some shorts at the green zone, then looking to unload for a break above. Good luck and trade safe!

I've noticed that talking-forex.com and forexlive.com are disinformation websites that function for one of the biggest banks/brokers in the world. My first guess is BIS (something Jonahky has mentioned many times) . I've been monitoring these 2 web sites for a long time now.

Here's a typical sampling of how they operate. The following are posts in the News section of FF from March 19th:

"Fed's Fisher: no one presently believes that the Fed are going to proceed with Q3." talking-forex.com.

The MOMENT this was released price sat at...

Ignored

Totally agreed

I also have been noticing these websites and especially 'talking-forex.com' is totally a bullshit site for me so whenever news come from there site I say to myself these sucker are long on the sucker of all(euro) so I dont trade and try to find the next better opportunity to short the papa sucker(euro)

I was so annoyed today when this news come out today from 'forexlive.com' GBPUSD moves above the 200 day MA at 1.5858 and shows some life , and still dont know why the F**K the news was marked with 'medium impact expected'

I've noticed that talking-forex.com and forexlive.com are disinformation websites that function for one of the biggest banks/brokers in the world. My first guess is BIS (something Jonahky has mentioned many times) . I've been monitoring these 2 web sites for a long time now.....

Ignored

Hmmmm... I've noticed similar, but I've been putting this into the frame of human psychology. Do you know how gamblers when playing a slot machine start thinking that game is playing against them in purpose? This same applies when playing video game or computer game. When you lose, instead of taking your loss, you start blaming machine for foul play.

This sounds similar. When trader makes analysis and they fail, instead of admitting that they were wrong they have to find someone to blame. (I do the same - when price starts moving to wrong direction I blame big institutions or chinese for foul play - though it is not their fault I lose - or my analyses are wrong... )

Your proof could be just a coincidence or maybe it is true? Who knows? Can we sue them? No. Can we read their analyses and news with caution? Yes.

Can we use this misinformation to our benefit? Absolutely Yes!

I've noticed that talking-forex.com and forexlive.com are disinformation websites that function for one of the biggest banks/brokers in the world. My first guess is BIS (something Jonahky has mentioned many times) . I've been monitoring these 2 web sites for a long time now.

Here's a typical sampling of how they operate. The following are posts in the News section of FF from March 19th:

"Fed's Fisher: no one presently believes that the Fed are going to proceed with Q3." talking-forex.com.

I've noticed that talking-forex.com and forexlive.com are disinformation websites that function for one of the biggest banks/brokers in the world. My first guess is BIS (something Jonahky has mentioned many times) . I've been monitoring these 2 web sites for a long time now.

Here's a typical sampling of how they operate. The following are posts in the News section of FF from March 19th:

"Fed's Fisher: no one presently believes that the Fed are going to proceed with Q3." talking-forex.com.

The MOMENT this was released price sat at...

Ignored

You just have to learn to weed out the opinions from what they report. I use ForexLive to gather facts they report on news releases and known market orders.

As for statements from third parties, I always verify the source and make sure it is reported by a reputable media company such as Reuters or Bloomberg or CNBC. I also always have CNBC TV on while trading so that I can be aware of breaking news... not analyst opinion. I don't care about what they say because their statements are always self serving.

The information I extract from ForexLive, which I believe to be reliable, has never turned out to be wrong as far as I can remember. As for the information that I ignore or dismiss, I have never even tried to verify it so I have no idea if they are in fact trying to manipulate the readers with their opinions.

Regarding talking-forex.com, I don't listen to them and nor do I even bother with the crap that's comes across Twitter feeds. Those are definitely misinformation and it's clear as day.

There's a lesson to be learned here and that is to not believe anything you hear and only believe half of what you see.

Cheers and have a great evening.

PT

Those who say it cannot be done should not interrupt those who are doing it

You just have to learn to weed out the opinions from what they report. I use ForexLive to gather facts they report on news releases and known market orders.

As for statements from third parties, I always verify the source and make sure it is reported by a reputable media company such as Reuters or Bloomberg or CNBC. I also always have CNBC TV on while trading so that I can be aware of breaking news... not analyst opinion. I don't care about what they say because their statements are always self serving.

The information I extract from ForexLive,...

Ignored

I like forexlive as well. Also it is difficult to separate cause from effect. I believe that the initial spike is caused by the priority new feeds which then might cause the subsequent talking-forex.com headline.

I think watching market reaction to twitter is useful because it allows you to judge market sentiment.

Joined Oct 2009

|

Status: Whn Market Warms u..U keep it Kool

|6,578 Posts

Sell from 1.3260 should able to produce a good yield (100 +) ... Long Raff is no more indicating any space on the Upper but major downward is not confirmed until the short Raff calm down and start decending.

Dear Friends,

Please note that the NAHB Housing Market Index had a reading of 28 for March, versus the expected reading of 30, which is a SLIGHT surprise given the recent momentum seen in the housing industry.

Apparently the wizards of "Expected or Surprised" blew this one.

Not to worry, it was only a slight surprise and MOPE would have you convinced the housing market is improving.

Regards,

Jim

Jim Sinclair’s Commentary

I want you to consider whether the tie between the Swiss Franc and the euro for intervention, not the Swiss Franc and the dollar, has any long term implications you should be considering.

Kno's Comments:

I was out all day on Monday however I wonder based on looking at the charts starting near 10:15 AM and near 1.3150 EUR/USD how this number affected the markets ? Any comments on this ?

Investors Who Can Separate "World Reality" From "Market Reality" Will Do Just Fine

As we looked around for something boffo to write about this weekend, we found nothing new and exciting. That suggests that something extraordinary is most likely to be around the corner. But what is it?

Maybe it's all been done. Maybe it's all been said. Maybe none of this matters? But we all know it matters. We all know that we could blow the whole world off and then come back and have a stack of bills waiting to be paid that bring us back to reality.

Around the world the same themes are apparent. Wars, atrocities, ideological madness and a continued and growing disparity in wealth. What it all amounts to is that little is being accomplished and that the current cycle is going to be in place for some time in the future.

Yes, if Israel attacks Iran the world will notice. Markets will move. And other unpredictable circumstances will unfold. North Korea remains unpredictable. And Spain, Portugal, and other countries in Europe are still insolvent, nearly insolvent, or on their way to being insolvent. And yes, the U.S. debt crisis continues to climb. Gasoline prices are skyrocketing. And the U.S. election is getting stranger by the minute.

None of that matters to the markets right now, though, because the world is currently built upon a giant mountain of paper money created out of thin air. And the public has little idea about that. There are still a lot of people out there that think that money is backed by something, if they bother to think about it at all. Many just go about their business day by day doing the best that they can and don't have the time or interest to worry about the macro issues or the minutiae about where money comes from, or if the economic data being put out by governments is the truth.

Many just don't care. And that's why governments and big trading firms get away with their actions and mostly escape unscathed. Too few people understand how the world works.

CONCLUSION !!!

We see a lot of rot in the underbelly of our society that has yet to come out and that will lead to major conflicts when it is exposed. We see "functional" people who work for a living but require painkillers and tranquilizers to make it through the day. And we see lives of previously productive people who have lost everything because of addiction to methamphetamine and cocaine. It's out there. And it's lurking.

Big law firms in New York are indebted to the tune of hundreds of millions of dollars. And partners that were promised X amount of money for bringing their big book of clients to the firm are leaving. We've seen this to some degree in our neck of the woods.

At the same time, some everyday people are finding work and making the best of it. There are new segments of businesses that are catering to those who were down and out and are now trying to climb back toward a better life.

What does it all mean? It's all one big soup with multiple moving parts. Nothing is working in synchronicity with anything else. And as long as this goes on, the market can go higher because there will be no single opinion about prices. Markets like worry. And there is lots of it to go around. Conclusion

The world is on the verge of becoming a cauldron of Disorder. Yet the market is orderly for now and people refuse to fully acknowledge it. This inability to compartmentalize the "world reality" from the "market reality" is consting investors money.

The world isn't likely to end well in the not too distant future. But for now the market is doing just fine.

Forty-two months after the collapse of Lehman Brothers, negative banking stories continue appearing daily – not about the criminal prosecutions for events that happened five years ago, but on examples of greed and stupidity that are occurring today. On both sides of the Atlantic, massive regulatory efforts have been carried out that, if anything, have made matters worse. Nobody has confidence that another Lehman Brothers, with accompanying taxpayer rescue of major banks, could not happen next month.

Let’s face it: the current financial system simply does not work. It concentrates risk in the largest institutions, which have to be bailed out, it prevents management from being held to account for its misdeeds, it promotes sharp-elbowed “investment bankers” to run behemoths most of whose business is entirely routine and it makes shareholders a despised peon class whose dividends are subordinated to the stock options of its management. As I suggested a couple of weeks ago, financial services as a business may be about to decline back to its historic share of the economy; it seems clear from recent events that it will have to be restructured also.

The leaving letter by Greg Smith to his ex-employer Goldman Sachs, published March 14 in the New York Times, identifies some but not all of the problems. His claim that Goldman no longer puts clients’ interests first would certainly appear valid, from published information. However his timing on when that change occurred, allegedly within his mere decade at the firm, is laughably off-track; Goldman Sachs was run by Jon Corzine, of later MF Global notoriety, from 1994 to 1999, before Smith joined, and it had certainly become a trading-oriented client-exploiting behemoth by then.

The key piece of evidence is Lisa Endlich’s book, Goldman Sachs: The Culture of Success, published in 1999. It’s full of snide comments about how feeble and hidebound the old corporate finance guys were and how, beginning in the late 1980s, she and her trading colleagues took over the firm and remade it in their own image. It was always clear to me, reading the book when it was published, nearly a decade before the 2008 crash, that Endlich’s “feeble and hidebound” was pretty accurate code for the ethical, client-oriented values that Goldman progressively lost from about the mid 1980s, and that had been fully replaced by the trading-oriented culture by the time of Endlich’s book and Goldman’s 1999 flotation. In that respect however, Goldman was by no means unique; its trajectory was more visible because of Goldman’s outstanding success, but other houses followed the same unhappy route (or like the late unlamented Salomon Brothers, were never client-oriented in the first place).

The central problem of the current financial system is that the heavy blocks of capital necessary for nationwide commercial banking and insurance are given to speculators to play with. That was in retrospect the central virtue of the Glass-Steagall legislation separating commercial and investment banking; it ensured that the depositors’ funds and the capital generated by a commercial banking operation of the size of Citicorp or Chase Manhattan were used almost entirely for relatively low-risk commercial banking (although as Walter “Countries can’t go bust” Wriston of Citicorp demonstrated, foolish megalomania still got them in trouble from time to time).

Trading operations, along with brokerage and corporate finance, were then segregated in much smaller organizations, at that time owned directly by their partners, with unlimited liability. These trading, brokerage and corporate finance operations differed significantly from each other (Salomon Brothers had little corporate finance activity, relative to its size, while Morgan Stanley and Kuhn Loeb did very little trading until the 1970s). Nevertheless they were in no sense “too big to fail.”

Conclusions:

To those who protest that the derivatives market and its offshoots have all come into existence since 1980, and make the trading-oriented behemoths essential, I would respond that the economic value of those markets, other than as rent-seeking exercises, is in most case pretty marginal, and that their needs should not be allowed to drive the financial system. We now have hedge funds, full of aggressive, incentivized traders willing to take on any kinds of risks; the derivatives markets can thus be left safely in their hands. In any case, once interest rates are restored to their proper levels and proper legislation (or a modest Tobin tax) is brought in to curb insider trading (algorithmic or otherwise) based on knowledge of market flows, volumes in these markets are likely to decline.

Investment institutions have repeatedly expressed their view that a large part of their assets should be devoted to “alternative investments” – normally hedge funds and private equity funds with outsize fees attached.

Very well, let their money be devoted to propping up the derivatives and other trading markets, so that they are not attached to the massive pools of capital needed for banking and conventional insurance. If the hedge funds go bust, so that a few Harvard students have to pay their own way, a few California state pensioners find their pensions reduced; well, them’s the breaks. There is no reason why those costs should be paid by bank depositors or by taxpayers as a whole.

The seeds of a new financial system are already here, in the medium sized “boutiques” such as Greenhill and Evercore, whose client orientation is less sullied by their trading desks. Among commercial banks, those such as Barclays and Deutsche, where the investment banker/trader inmates have taken over the heavily capitalized asylum, are already looking like ineffective dinosaurs and will doubtless shortly go spectacularly bust. To replace them will come a new generation of pure commercial banks, such as Wells Fargo and PNC Corporation, far more capable than their competitors in their large low-risk niche, and content to avoid the perils of investment banking – and the unpleasantness of hyper-greedy investment banker colleagues.

Nothing will ever replace the sublime glory of merchant bank dining rooms. But the remainder of the pre-1986 London structure looks very much like the best way forward for the global financial system as a whole.

(The Bear's Lair is a weekly column intended to appear each Monday, an appropriately gloomy day of the week. Its rationale is that the proportion of "sell" recommendations put out by Wall Street houses remains far below that of “buy” recommendations. Accordingly, investors have an excess of positive information and very little negative information. The column thus takes the ursine view of life and the market, in the hope that it may be usefully different from what investors see elsewhere.)

Martin Hutchinson is the author of "Great Conservatives" (Academica Press, 2005)

I like forexlive as well. Also it is difficult to separate cause from effect. I believe that the initial spike is caused by the priority new feeds which then might cause the subsequent talking-forex.com headline.

I think watching market reaction to twitter is useful because it allows you to judge market sentiment.

Ignored

I'll have to agree on that. The key word is watching

Those who say it cannot be done should not interrupt those who are doing it

Joined Aug 2008

|

Status: Persist Until Something Happens

|17,898 Posts

Morning folks. Let's see which way this witch will decide to go today.

Of interesting note is the USDX's bounce off the H4 100ema and 38.2 fibo level depicted in the chart below

Attached Image (click to enlarge)

Also looks to be a bit risk off so far in the futures markets

Attached Image (click to enlarge)

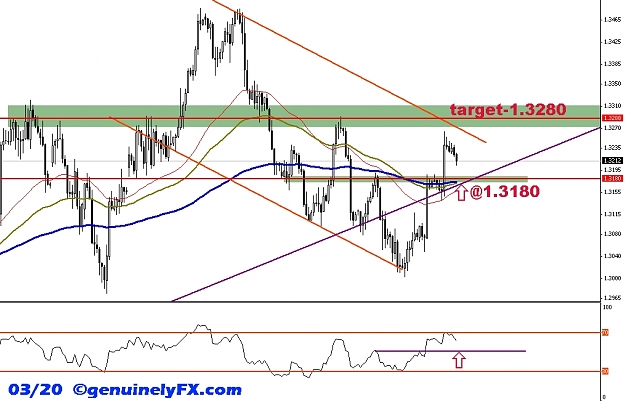

If E/U manages to close an H1 candle below the daily pivot at 1.3210 area and the rising channel support (RC-2), then that may be a signal of bearish continuation.

Attached Image (click to enlarge)

Those who say it cannot be done should not interrupt those who are doing it

Good morning! Price managed a slip to the daily pivot shortly after London open which until now still holds the ground. Below, strong support comes at 1.3180, which can be a good level for buying into a position, targeting the upper resistance at 1.3280-300. Make your plan, add the patience and execute with confidence. Good luck and trade safe!

![Click to Enlarge

Name: genuinelyFX_2012.03.19_eurusd_h4[2].jpg

Size: 186 KB](/attachment/image/923354/thumbnail?d=1365752777)