DislikedExactly right. At its root is eigenvectors; the "factor weights" are just (possibly renormalized) eigenvalues.Ignored

Other simple static approaches can be found e.g.

http://www.cutthespread.com/spread-b...urrent-reality

http://www.cutthespread.com/spread-b...s-dollar-index

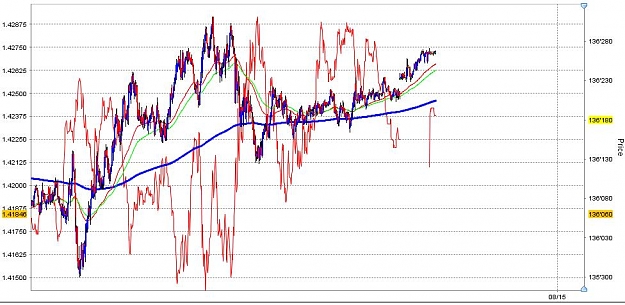

They do work better on the larger tfs but in my opinion are not so good on the smaller ones + they still suffer the same fundamental problem like the original indices when shit hits the fan.

Still have to come up with a fully automatic adaptive one... The key is somewhere in this definitly.