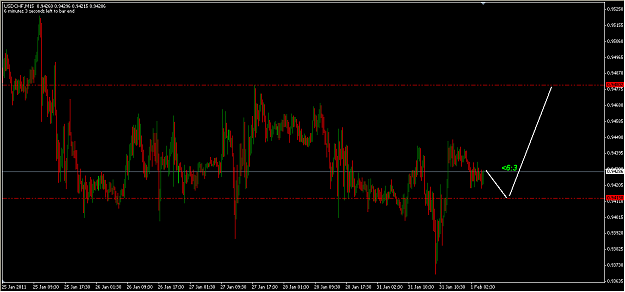

Interesting...

The sharp drop in USDCHF has been due to dollar

weakness rather than franc strength. In fact, on the Swiss

side things point to a weaker franc. Against the euro this

Franc strength has become a political issue in

Switzerland. Even if we do not expect any direct impact

on economic policies, the SNB has likely become even

The SNB has recently lowered its rates on short-term

money market operations. This may have been targeted

at increasing the yield differential to the Eurozone,

We think that the risks to our 3m EURCHF 1.28 forecast

are now on the upside and we also stick to our 1.02 view

Franc politics

The most recent drop in USDCHF seems essentially a

dollar story. We continue to think that more broadly the

dollar will rebound over the next few weeks and months,

and that long USDCHF is a good way to express this view

1.

On the Swiss side, however, there have been few if any

reasons for a stronger franc and we have indeed become

significantly less bullish than we were for most of 2010.

The first point to mention is the much increased political

noise about franc strength. It is highly unusual in

Switzerland that the Economy Ministry would call industry

and union representatives for a ‘summit’ on the franc (14

Jan), and for the government to discuss the issue

prominently in one of its weekly meetings (19 Jan). It is

also rather unusual for a major representative of one of the

three government parties to call for the resignation of the

SNB President amid book losses on the back of last year’s

FX interventions. It is very important to note that none of

this is likely to have a material impact on Swiss monetary,

exchange rate or even economic policy more broadly. The

independence of the SNB certainly remains a cornerstone of

Swiss economic policy and the government as well as the

vast majority of senior politicians miss no opportunity to

acknowledge as much. However, we do think that the SNB

may not be entirely insensitive to the animated discussions

and may at least sound more concerned about Swiss franc

The question is what the SNB could do if Swiss franc

strength indeed were to once again become a threat to price

stability, i.e. trigger a risk of deflation. We have argued

not currently an option anymore for the SNB. President

Hildebrand argued a couple of weeks ago that the danger of

deflation was ‘largely gone’. Only substantially worse-thanexpected

economic data could change this assessment.

Apart from intervening on the FX markets, the SNB has few

if any options left

2. In fact, the only palatable measure may

be to increase franc liquidity in the market, which would in

turn push forward-implied yields further into negative

territory. This happened in mid-2010 as a side effect of the

massive FX interventions, pushing implied yields to as low

as -160bp (Chart 1). The SNB then quickly remedied the

situation by mopping up the excess liquidity with bill

issuance and stepped up reverse repo activity. As a result,

the excess liquidity as showing up in sight deposits dropped

from a peak of CHF103 bn to now around CHF27 bn.

Interestingly, the SNB over the last few weeks has

continuously lowered the rates on its short-term money

market instruments. The 1-week reverse repo now stands at

just 9bp from a peak of 14bp in autumn last year while the

28-day SNB Bill dropped to just 11.4bp last week (Chart

2). The SNB has not publicly talked about this trend but

one interpretation could certainly be that the SNB has

release pressure on the franc. The move higher in Euro

rates may have been seen as an opportunity to widen the

differential to Swiss rates by keeping the later low. Indeed,

the differential between 3m Euribor and CHF Libor has

widened to as high as 88bp from as low as 39bp last year

(Chart 3). As a result, despite tightening expectations rising

even for the SNB along with a recently more hawkish ECB,

Conclusion

The current developments in Egypt have demonstrated that

even while global macroeconomic risks may be viewed as

under control, geopolitical tensions can rise somewhere in

the world at almost any moment. The Swiss franc will

remain the safe haven of choice for such occasions. Beyond

that, however, we argue that the main reason for the recent

drop in USDCHF has been entirely dollar driven and that

on the Swiss side things have become less bullish. In

particular, we would point to what appears to be a subtle

monetary easing by the SNB, which has recently moved

rates lower on short term money market operations. In fact,

rather than taking a cue from the ECB and sounding more

hawkish, the SNB appears to have taken the opportunity to

widen the yield differential to the Eurozone. As a result, we

now see the risk to our 3m EURCHF forecast of 1.28 on the

upside and would not be surprised if the cross moved

substantially above 1.30 over the next few weeks. On the

USDCHF side we stick to our 1.02 forecast as we expect the

FEN 31/01/2011