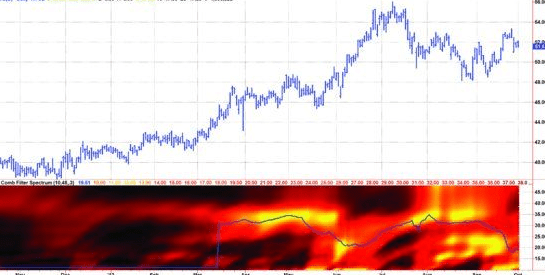

A real gem from John Ehlers

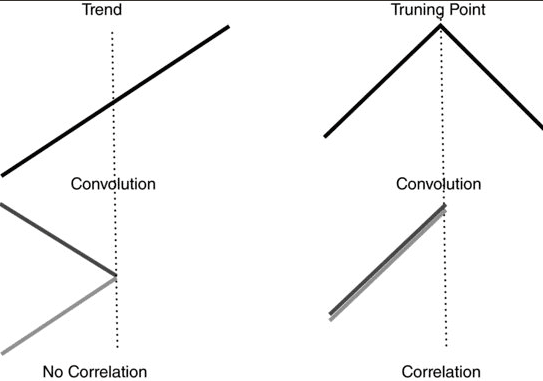

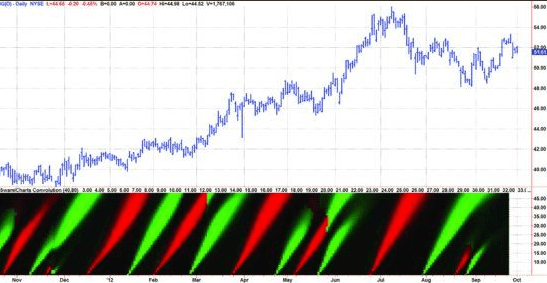

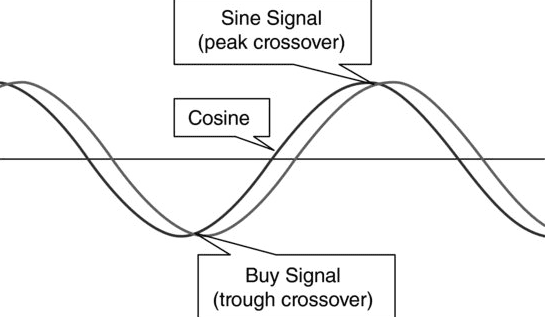

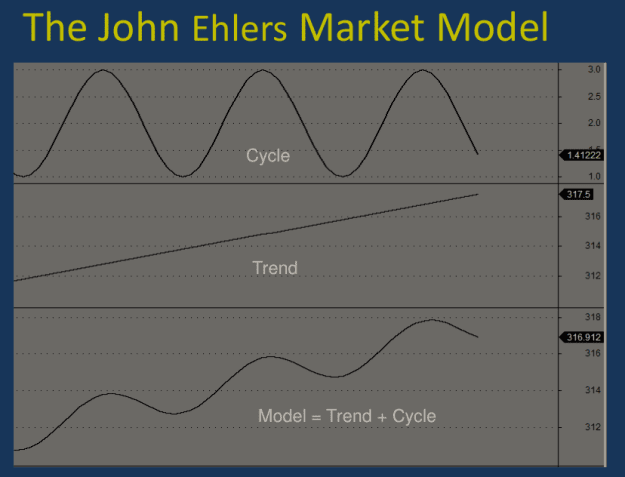

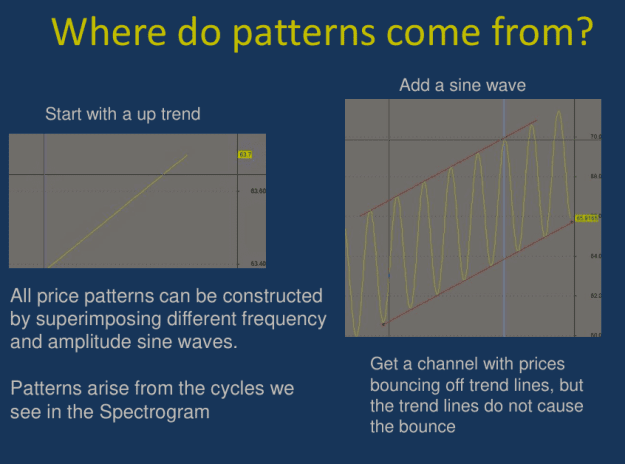

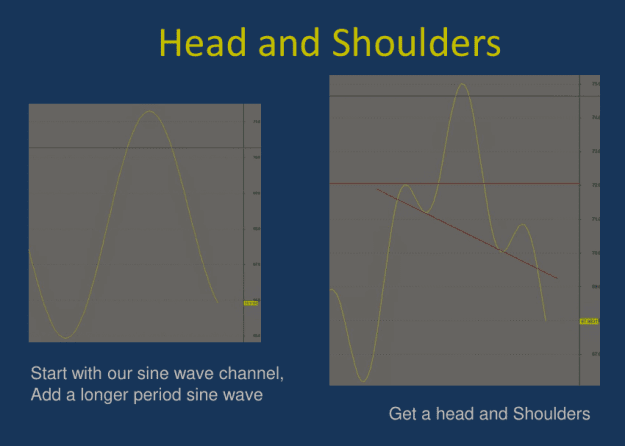

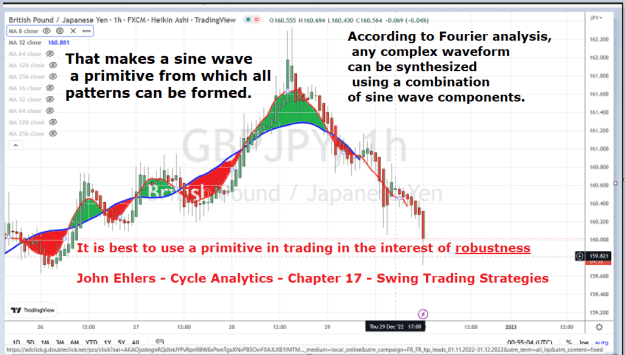

According to Fourier analysis, any complex waveform can be synthesized using a combination of sine wave components.

That makes a sine wave a primitive from which all patterns can be formed.

It is best to use a primitive in trading in the interest of robustness

Cycle Analytics Chapter 17 Swing Trading Strategies

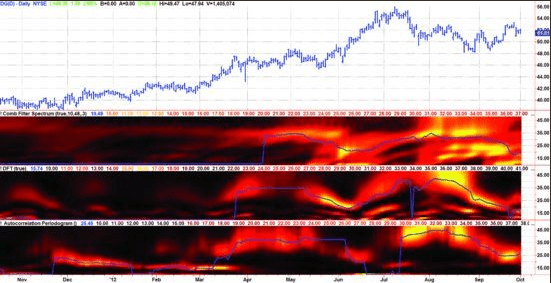

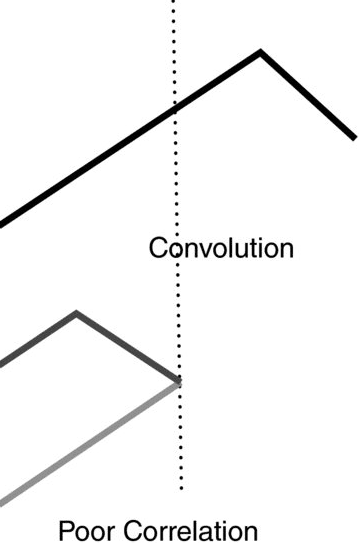

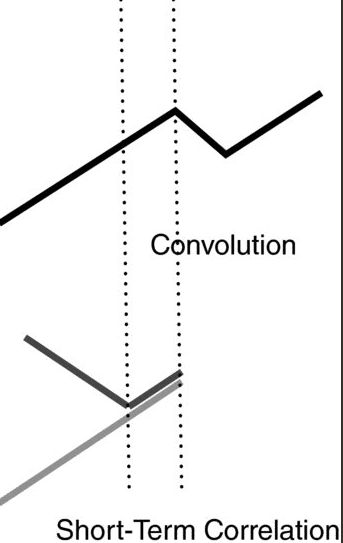

According to Fourier analysis, any complex waveform can be synthesized using a combination of sine wave components.

That makes a sine wave a primitive from which all patterns can be formed.

It is best to use a primitive in trading in the interest of robustness

Cycle Analytics Chapter 17 Swing Trading Strategies

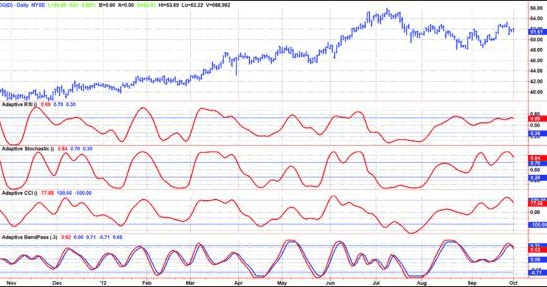

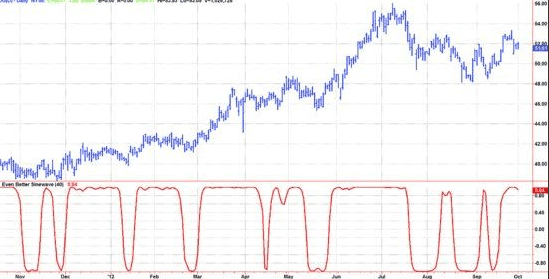

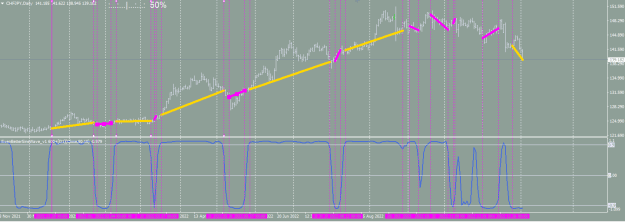

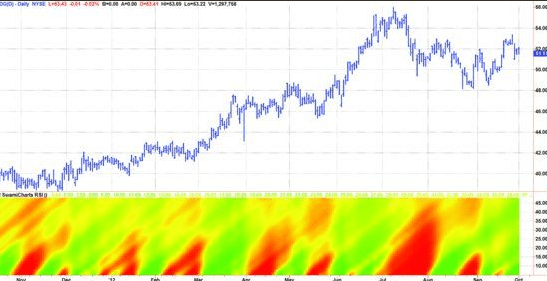

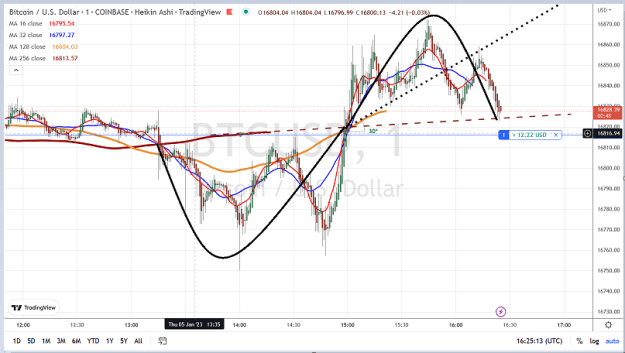

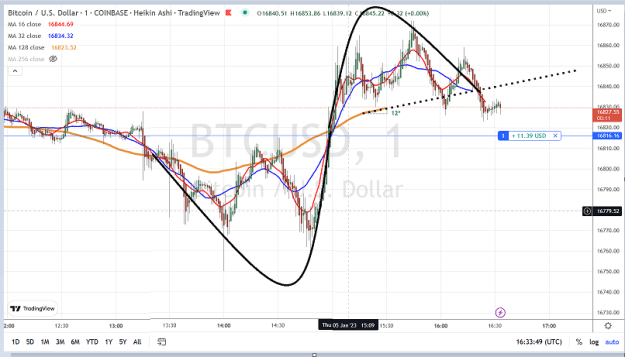

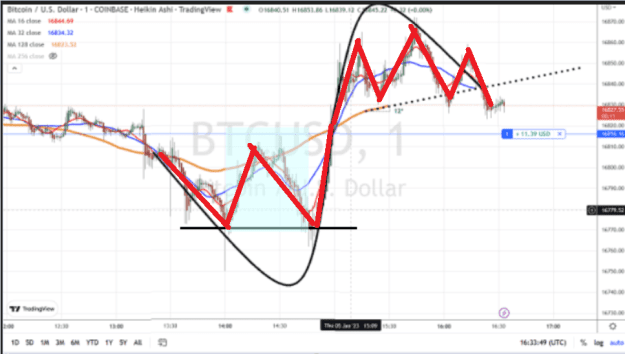

Attached Image (click to enlarge)

1