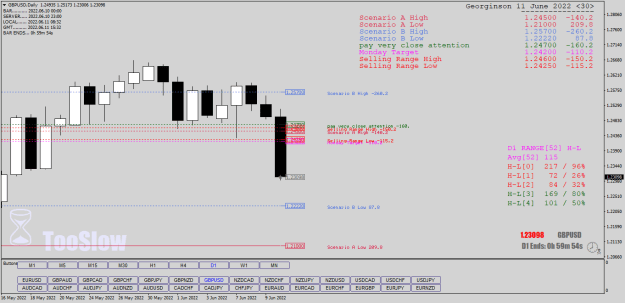

Just looking @ the prevailing fundies and data release event risks this coming busy week:

Mon We have Uk Gdp and some manuf and industr pmi data - both of which are more likely (not certain) to undershoot expectations than overshoot them. In this scenario we could see some more £ weakness. Should they overshoot we could see some £ buying and a 'relief' rally?

Tues Some Uk employment data which is more likely to be good than bad and again the above likely reactions apply. Also U.s PPi later that day.

Weds U.s Retail sales and U.s Fed's Fomc rate. Retail sales more likely to undershoot forecasts than overshoot, and Fomc more likely to realise them, or even a small chance of overshooting the expected +0.5% rise.

Thurs Uk Boe Mpc rate and vote, Likely to realise the expected +0.25% rate rise, but the vote (last 9-0-0) is important, and a very small chance of an overshoot on that expectation. (More chance of an undershoot but +0.25% remains the most likely outcome.)

Worth noting that whatever the Uk rate rise is, the market could ultimately be disappointed in ' just ' +0.25%, and we could in that scenario see further £ weakness, even after an intial knee-kerk rally?

Fri Uk retail sales, again more likely to undershoot expectations/forecasts than overshoot. Fed Chair Powell speaks in the Uk afternoon.

-------------------------------------------------

War in Ukraine/Cost of living crises/Inflation/ to an extent Gdp growth remain the predominant Fundie themes affecting this pairing.

NB: Should things get 'much worse' over the forthcoming months, the market could flip into a 'risk-off' mode?

Mon We have Uk Gdp and some manuf and industr pmi data - both of which are more likely (not certain) to undershoot expectations than overshoot them. In this scenario we could see some more £ weakness. Should they overshoot we could see some £ buying and a 'relief' rally?

Tues Some Uk employment data which is more likely to be good than bad and again the above likely reactions apply. Also U.s PPi later that day.

Weds U.s Retail sales and U.s Fed's Fomc rate. Retail sales more likely to undershoot forecasts than overshoot, and Fomc more likely to realise them, or even a small chance of overshooting the expected +0.5% rise.

Thurs Uk Boe Mpc rate and vote, Likely to realise the expected +0.25% rate rise, but the vote (last 9-0-0) is important, and a very small chance of an overshoot on that expectation. (More chance of an undershoot but +0.25% remains the most likely outcome.)

Worth noting that whatever the Uk rate rise is, the market could ultimately be disappointed in ' just ' +0.25%, and we could in that scenario see further £ weakness, even after an intial knee-kerk rally?

Fri Uk retail sales, again more likely to undershoot expectations/forecasts than overshoot. Fed Chair Powell speaks in the Uk afternoon.

-------------------------------------------------

War in Ukraine/Cost of living crises/Inflation/ to an extent Gdp growth remain the predominant Fundie themes affecting this pairing.

NB: Should things get 'much worse' over the forthcoming months, the market could flip into a 'risk-off' mode?

Trader with an Edge.

6