Disliked{quote} That's an excellent question but the book does not specify. I am checking the notes in the appendix now to see if it will tell us or at least tell us where to look... I have an opinion about this but I'll withhold it until I get the official story...Ignored

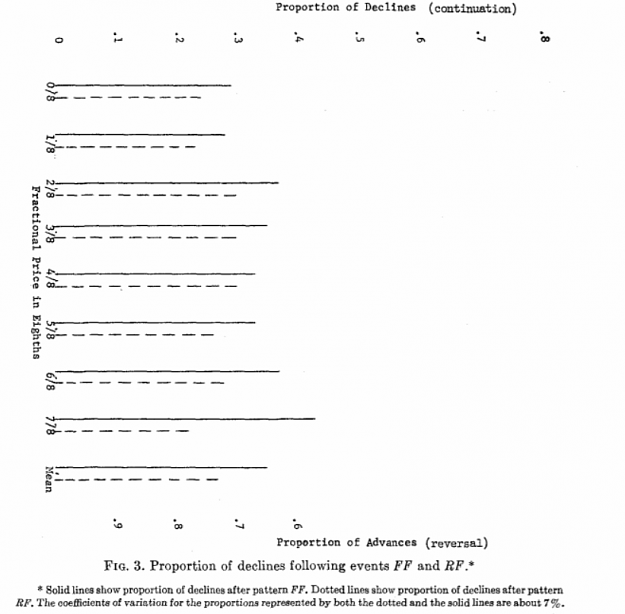

1. Osborne didn't make these conclusions alone but with a collaborator - Victor Niederhoffer -one of the fathers of statistical arbitrage. It might be worth adding his book to the reading list - the Education of a Speculator. However Neiderhoffer is most famous for tanking his Matador fund in 2007.

2. Weatherall refers to an article that he simply names Neiderhoffer and Osborne (1966). I believe it is this one: https://www.tandfonline.com/doi/abs/....1966.10482183

I have downloaded it and will add it to today's reading so you should have an answer (even if it's 'I don't know') soon.

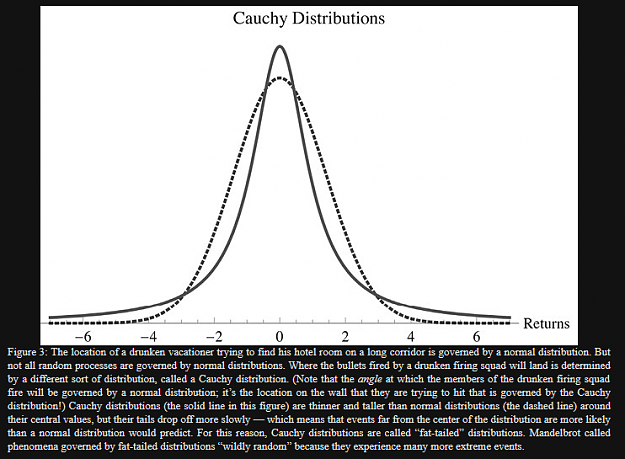

My own opinion is based on Mandelbrot's fractal work. Since all charts are basically snapshots of multifractal amplitude over multifractal time, what is 'a little bit' is relative to the local volatility as a whole. So no matter what your trading horizon is, five minutes or five months, prices are mean-reverting in the short term and trending in the long term (in general). But let's see what Osborne and Neiderhoffer have to say if anything.

1