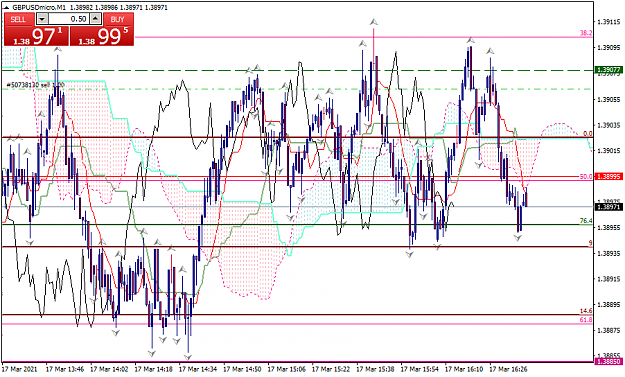

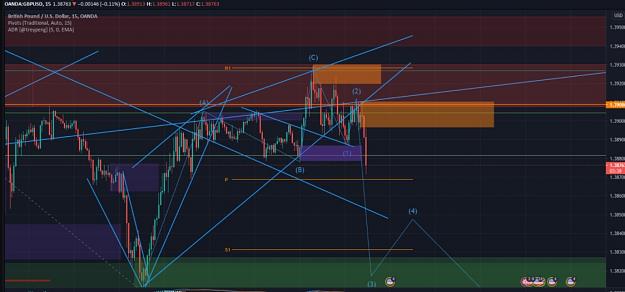

DislikedThis is not elliott wave , it is impulsive/corrective structure Blue is daily Red is 4H as always any trades taken would need to have confirming structure on lower timeframes {image}Ignored

Cable Update (GBPUSD)

Cable Update (GBPUSD)

- #584,405

- Mar 17, 2021 9:37am Mar 17, 2021 9:37am

- Joined Apr 2013 | Status: Trader | 1,926 Posts

If you don't know how to earn money, don't loose it.

- #584,409

- Mar 17, 2021 9:50am Mar 17, 2021 9:50am

- Joined Aug 2010 | Status: Trader | 5,508 Posts

dolce vita

- #584,412

- Mar 17, 2021 9:52am Mar 17, 2021 9:52am

- Joined Oct 2010 | Status: Trader | 4,465 Posts

Follow The Markets Structure - Patience and Discipline

- #584,413

- Mar 17, 2021 9:53am Mar 17, 2021 9:53am

- Joined Apr 2020 | Status: Trader | 8,815 Posts

Trader with an Edge.

- #584,416

- Mar 17, 2021 9:56am Mar 17, 2021 9:56am

- | Additional Username | Joined Mar 2020 | 1,607 Posts

- #584,417

- Mar 17, 2021 9:57am Mar 17, 2021 9:57am

- Joined Aug 2018 | Status: Joyful and Proud | 2,002 Posts

Risk Management is of utmost importance!

- #584,418

- Mar 17, 2021 9:58am Mar 17, 2021 9:58am

- Joined Apr 2013 | Status: Trader | 1,926 Posts

If you don't know how to earn money, don't loose it.

- #584,419

- Mar 17, 2021 9:58am Mar 17, 2021 9:58am

- Joined Oct 2010 | Status: Trader | 4,465 Posts

Follow The Markets Structure - Patience and Discipline

- #584,420

- Mar 17, 2021 10:04am Mar 17, 2021 10:04am

- Joined Dec 2017 | Status: Trader | 30,715 Posts

yes yes yes