1. Christmas Vacation Stock markets in Australia, New Zealand, Europe, the U.K., Switzerland, Canada and the U.S. will remain closed on Monday, to make up for Christmas Day falling on a Sunday. Brits and Canadians get an extra day off for Boxing Day, so markets in those countries will also be closed on Tuesday. 2. U.S. December Consumer Confidence The Conference Board, a market research group, is to publish data on December consumer confidence at 10:00AM ET (15:00GMT) on Tuesday, with market players expecting the index to rise to 108.5 from 107.1 a month earlier. If confirmed it would be the strongest reading since July 2007. 3. U.S. Pending Home Sales for November The National Association of Realtors is to release data on November pending home sales at 10:00AM ET (15:00GMT) on Wednesday. The report is expected to show pending home sales rose 0.5% last month, after inching up 0.1% in October. 4. U.S. Weekly Initial Jobless Claims The U.S. is to release a weekly report on initial jobless claims at 8:30AM ET (13:30GMT) Thursday, amid expectations for an increase of 2,000 to 277,000 in the week ending December 23. 5. Japanese November CPI Japan's Statistics Bureau will publish November inflation figures at 23:30GMT Monday (6:30PM ET). Market analysts expect the headline figure to remain negative, falling 0.4% year-on-year, which would be the 12th straight month of declines. The country has been struggling to hit its 2% consumer price target, keeping pressure on the Bank of Japan to maintain its aggressive stimulus package.

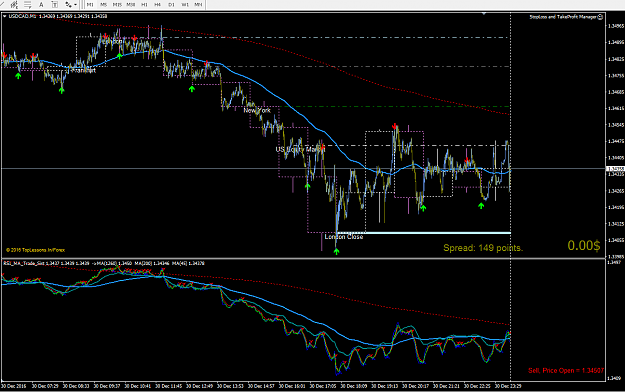

Only the price on the chart can show the entrance to the deal...

Tuesday

11:30

03/01/17

GB Index PMI in construction (GB Construction PMI), England, GBPUSD

Average reaction when trigger 30.00 points in the first minute after the release.

10% probability trades.

Tuesday

17:00

03/01/17

US ISM index of business optimism

(US ISM Manufacturing PMI), USA, USDJPY

Average reaction when trigger 25.00 points in the first minute after the release.

10% probability trades.

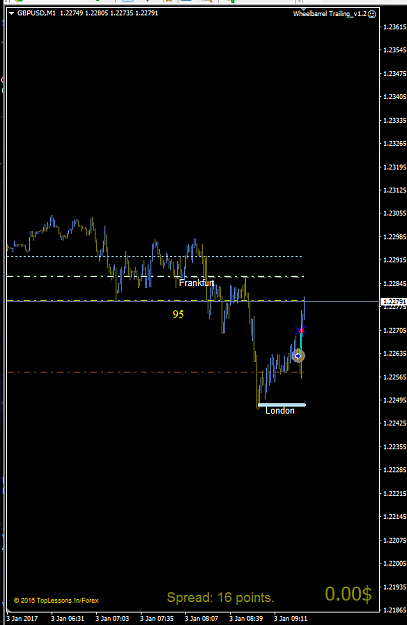

Only the price on the chart can show the entrance to the deal...

Wednesday

11:30

04/01/17

GB Index PMI in construction

(GB Construction PMI), England, GBPUSD

Average reaction when trigger 30.00 points in the first minute after the release.

10% probability trades

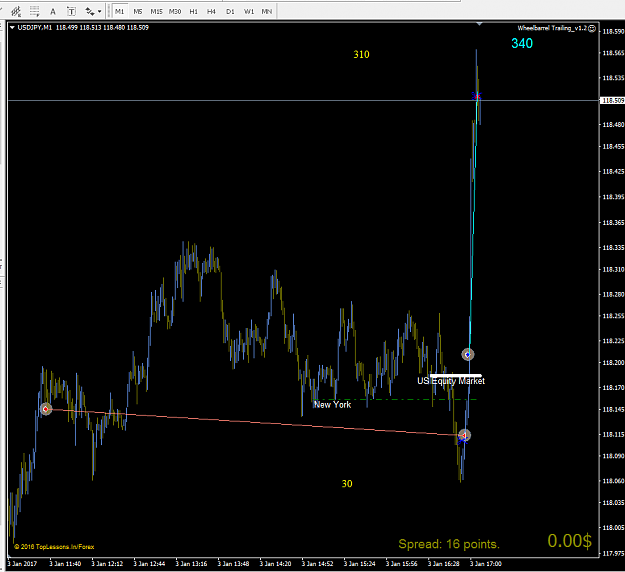

Only the price on the chart can show the entrance to the deal...

Thursday

11:30

05/01/17

GB activity index in the services sector

(GB Services PMI), England, GBPUSD

Average reaction when trigger 30.00 points in the first minute after the release.

10% probability trades.

Thursday

15:15

05/01/17

US ADP number of employed

(US ADP Non-Farm Employment Change), the United States, USDJPY

Average reaction when trigger 25.00 points in the first minute after the release.

15% probability trades.

Thursday

15:30

05/01/17

US weekly jobless report

(US Unemployment Claims), the United States, USDJPY

Average reaction when trigger 25.00 points in the first minute after the release.

5% probability trades.

Thursday

17:00

05/01/17

US sector activity index from the ISM services

(US ISM Non-Manufacturing PMI), US, USDJPY

Average reaction when trigger 25.00 points in the first minute after the release.

5% probability trades.

Thursday

17:30

05/01/17

US Natural Gas Reserves (US Natural Gas Storage), the United States, #NG

Average reaction when trigger 60.00 points in the first minute after the release.

25% probability trades.

Thursday

18:00

05/01/17

US reserves of crude oil and petroleum products

(US Crude Oil Inventories), USA, #CL

Average reaction when trigger 35.00 points in the first minute after the release.

10% probability trades.

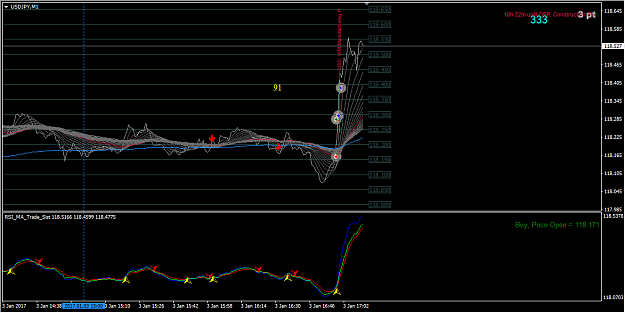

Only the price on the chart can show the entrance to the deal...

Friday

15:30

06/01/17

US Number of employed outside agriculture HOT!

(US Non-Farm Employment Change), the United States, USDJPY

Average reaction when trigger 60.00 points in the first minute after the release.

50% probability trades.

Only the price on the chart can show the entrance to the deal...

Week Ahead: Waiting For Trump; Buy N-Term USD Dips

The recent minor stalling of the USD rally is corrective in nature, in our view, and the USD uptrend should resume before long.

Indeed, we suspect that investors may want to wait until after President Donald Trump’s inauguration before adding to their USD-longs. One risk to this view is that concerns may abound about a repeat of Q1 2016, when the aggressive USD rally fuelled fears about the sustainability of the EM USD debt and triggered a spike in global risk aversion. That development forced the Fed to turn more cautious and effectively killed the USD rally last March.

Any dovish shift at the FOMC in response to further tightening in the global financial conditions is less likely this time, in our view. What is different is that global economic data are improving and inflation gauges nudging ever closer to the central banks’ targets.

In addition, the Trump victory should continue to invigorate animal spirits in the US. A more hawkish Fed should magnify any potential spike in global risk aversion on the back of fears about the EM FX debt sustainability, too aggressive USD appreciation and growing US protectionism.

The USD remains buy on dips in the near term, and we expect the upcoming US data releases and the Fed speakers to encourage further convergence in the Fed and market rate expectations. We estimate that the closing of that gap should boost USD TWI by more than 2% over the medium term.

We continue to think that being short commodity currencies vs the USD, especially the AUD, is a good way to express both a more aggressive FOMC and concerns about US protectionism.

EUR/USD should remain close to the lows for now on the back of lingering political risks and growing divergence between the hawkish Fed and dovish ECB. EUR could continue to suffer against some G10 smalls as well. In particular, we suspect the EUR underperformance against Scandi currencies could grow next week ahead of Swedish and Norwegian CPI data.

In contrast, EUR/GBP could remain supported ahead of the UK data and next week’s Supreme Court ruling. We expect the court to rule in favour of greater parliamentary involvement in Brexit, which might limit the risks of a hard Brexit over the long term but could add to the political uncertainty in the interim, adding to the headwinds for the economy.

Only the price on the chart can show the entrance to the deal...

I apologize to some subscribers.

Last time I did not send the answers to your questions in private messages. Maybe there are some problems with the site.

Only the price on the chart can show the entrance to the deal...