We are reaching at the end of the road. First round of closes coming from Europe so time to start wrapping up

10. Scenarios and Macro Expectations 2017

--> Dollar ... 'easy part of the move is gone'

After two very tiny, small and slow hikes in two years, we finally have a clear path for normalisation. All macro numbers are booming in all fronts marking a clear inflation expectations path for next year.

From a strictly monetary point of view, FED should easily be able to hike 3 or 4 times next year. However, we have a game changer in play since November. Trump is short-circuiting expectations across the board. in the case of Dollar, the infrastructure plan based on fiscal irresponsibility (US fiscal account are expected to a sharp correction to pre Obama levels in the mid term) with tax cuts for the rich and top corporation is a happy push.

Inflation expectation are jumping for next year and will easily carry Dollar with it Q1/ early Q2. However, fiscal issues with foreign policy jitters, protectionism, warmongering and less free flows and trade opportunities will charge a very big toll sooner rather than later in Dollar. Depending on how the honeymoon ends, momentum will completely fade out by Q3/Q4 after the next round of hikes as Europe (BOE first and ECB) rates expectations will enter in play.

On the TA side. 101.8x is the level to track for the yearly close. Dollar holding the break unlock 105.5x in a rather quick leg early in on the year and then a zigzag play to 100.xx and a bit below to close the year in wide chop zone until ECB, BOE and emerging currencies start pushing back.

---> Europe Economy and European Equities...."Europe is back...in play ...and one more time also with risk"

Most of EZ Equities looks solid. We found a bottom from Spain to Finland and everybody else in between. Europe macro environment looks very similar to the US 2 years ago. Two big hurdles ahead will keep Equities on check.

First we need to clear a series of elections including France and the climax with Germany. If they stay on track and don't fall for the populist trap we will see a very sharp, consistent rally across the board.

Second, the Brexit fiasco. As per today UK looks set to be the only loser in economic terms. However things can change fast (and the above mentioned elections) and UK and Europe entering in a backward spiral that can destroy the common market will be devastating for the continent leading for a sharp recession that will spread across the world.

Expecting (DAX and CAC as references) to break ATH early in the year. All macro pointing up, US on steroids, free money from ECB guarantee and political risk still a few months down the road. We are set to mark the high of 2017 rather early (Q1/Q2) and then will enter in extended narrow chop zone till risk and brexit are cleared. Only a major fck up from Brexit (e.g end of common market) or war nearby (eyes on Russia this year) will derail the recovery.

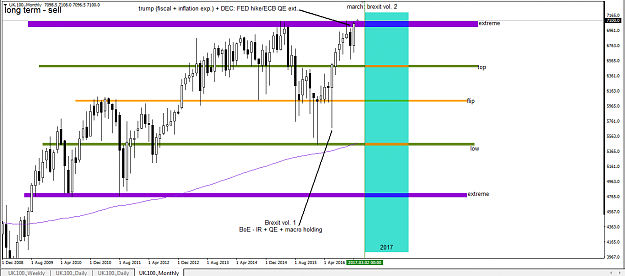

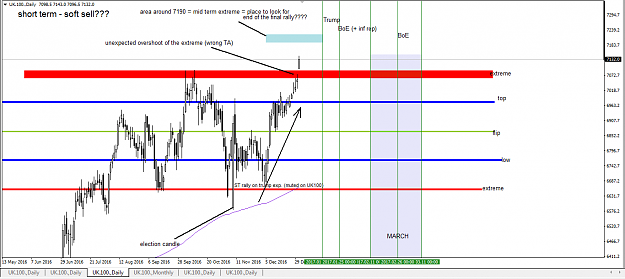

On FTSE, it will benefit from the collateral impact until Brexit details get confirmed but the 'minutes' are counted. Only a major shift on the Brexit front will align FTSE with the rest of the world. The high in this current leg will mark a long and mid term high that will hold for a few years.

---> OIL & commodities...."Trump? ... it's my best friend"

Oil and commodities found a clear bottom. Both political factors, supply and demand factors are all aligned one more time. On top Trump initial plans (both in foreign policy and economics) are a huge gift for commodities across the world.

Expecting OIL to carry the rally fuelled by equities hand in hand. We couldn't complete the test $56.xx this year but we already unlocked the $65 handle. Exact same scenario for NG with $4.0x but also already unlocked $4.3x.

Things get a lot trickier later in the year. Geopolitical risk on the rise (Trump and Russia and all that), China is still far from picking pace, Brexit put Europe out of business for a while, emerging economies wont raise their head above ground, OPEC agreement is myopic and very feeble especially with the huge divergences between the Saudis and Russia, Iran and the rest.

Gold is very tricky this year and it will be a very hard one to trade. Between hikes early in the year and ECB/BOE and BOJ at the end and with a plethora of potential hiccups via risk in between it's set for a rather unclean but volatile legs.

On the short term, 'all roses' is the name of the game Q1/Q2. Gold losing 1135.x unlock that pending (from last year) 940.xx. However, anything beyond that is pretty much locked in a steel support that wont be cracked without a major game changer. Sidelined until 1135. is solved. Expecting a zigzag and then Q3 narrow chop zone for a flattish year.

---> US equites ...."if Trump walks the talk ....the end of happy years"

If Trumps walk the talk, US will experience for the fist time the terrible effects of protectionism and wont be nice neither for the average voter, neither...

....TBC

sisse

+++++ Yearly overview +++++

10. Scenarios and Macro Expectations 2017

--> Dollar ... 'easy part of the move is gone'

After two very tiny, small and slow hikes in two years, we finally have a clear path for normalisation. All macro numbers are booming in all fronts marking a clear inflation expectations path for next year.

From a strictly monetary point of view, FED should easily be able to hike 3 or 4 times next year. However, we have a game changer in play since November. Trump is short-circuiting expectations across the board. in the case of Dollar, the infrastructure plan based on fiscal irresponsibility (US fiscal account are expected to a sharp correction to pre Obama levels in the mid term) with tax cuts for the rich and top corporation is a happy push.

Inflation expectation are jumping for next year and will easily carry Dollar with it Q1/ early Q2. However, fiscal issues with foreign policy jitters, protectionism, warmongering and less free flows and trade opportunities will charge a very big toll sooner rather than later in Dollar. Depending on how the honeymoon ends, momentum will completely fade out by Q3/Q4 after the next round of hikes as Europe (BOE first and ECB) rates expectations will enter in play.

On the TA side. 101.8x is the level to track for the yearly close. Dollar holding the break unlock 105.5x in a rather quick leg early in on the year and then a zigzag play to 100.xx and a bit below to close the year in wide chop zone until ECB, BOE and emerging currencies start pushing back.

---> Europe Economy and European Equities...."Europe is back...in play ...and one more time also with risk"

Most of EZ Equities looks solid. We found a bottom from Spain to Finland and everybody else in between. Europe macro environment looks very similar to the US 2 years ago. Two big hurdles ahead will keep Equities on check.

First we need to clear a series of elections including France and the climax with Germany. If they stay on track and don't fall for the populist trap we will see a very sharp, consistent rally across the board.

Second, the Brexit fiasco. As per today UK looks set to be the only loser in economic terms. However things can change fast (and the above mentioned elections) and UK and Europe entering in a backward spiral that can destroy the common market will be devastating for the continent leading for a sharp recession that will spread across the world.

Expecting (DAX and CAC as references) to break ATH early in the year. All macro pointing up, US on steroids, free money from ECB guarantee and political risk still a few months down the road. We are set to mark the high of 2017 rather early (Q1/Q2) and then will enter in extended narrow chop zone till risk and brexit are cleared. Only a major fck up from Brexit (e.g end of common market) or war nearby (eyes on Russia this year) will derail the recovery.

On FTSE, it will benefit from the collateral impact until Brexit details get confirmed but the 'minutes' are counted. Only a major shift on the Brexit front will align FTSE with the rest of the world. The high in this current leg will mark a long and mid term high that will hold for a few years.

---> OIL & commodities...."Trump? ... it's my best friend"

Oil and commodities found a clear bottom. Both political factors, supply and demand factors are all aligned one more time. On top Trump initial plans (both in foreign policy and economics) are a huge gift for commodities across the world.

Expecting OIL to carry the rally fuelled by equities hand in hand. We couldn't complete the test $56.xx this year but we already unlocked the $65 handle. Exact same scenario for NG with $4.0x but also already unlocked $4.3x.

Things get a lot trickier later in the year. Geopolitical risk on the rise (Trump and Russia and all that), China is still far from picking pace, Brexit put Europe out of business for a while, emerging economies wont raise their head above ground, OPEC agreement is myopic and very feeble especially with the huge divergences between the Saudis and Russia, Iran and the rest.

Gold is very tricky this year and it will be a very hard one to trade. Between hikes early in the year and ECB/BOE and BOJ at the end and with a plethora of potential hiccups via risk in between it's set for a rather unclean but volatile legs.

On the short term, 'all roses' is the name of the game Q1/Q2. Gold losing 1135.x unlock that pending (from last year) 940.xx. However, anything beyond that is pretty much locked in a steel support that wont be cracked without a major game changer. Sidelined until 1135. is solved. Expecting a zigzag and then Q3 narrow chop zone for a flattish year.

---> US equites ...."if Trump walks the talk ....the end of happy years"

If Trumps walk the talk, US will experience for the fist time the terrible effects of protectionism and wont be nice neither for the average voter, neither...

....TBC

sisse

Pending conversations? PM for a chat...I am mainly in OTM now

3