Related Instruments

Similar Threads

EurAnalysis Kindergarten 24 replies

EurAnalysis

EurAnalysis

- #23,361

- Mar 2, 2012 7:38pm Mar 2, 2012 7:38pm

- Joined Oct 2009 | Status: Whn Market Warms u..U keep it Kool | 6,578 Posts

- #23,362

- Mar 2, 2012 9:46pm Mar 2, 2012 9:46pm

- | Additional Username | Joined Oct 2011 | 2,098 Posts

Ponzi-Nomics

I have written many missives that revolved around the idea that the stock and bond markets are rigged. After all, a small group of folks in the FOMC set interest rates, which by definition means they are rigged. This of course greatly affects equity prices and the very moment that the banking mafia believes rates should be lower – it gets it.

There is a lot more to it than that, but the following is simply amazing: Foreign central banks have announced that they will DIRECTLY INVEST FUNDS INTO THE U.S. STOCK MARKET!

Market getting weak? Call the Swiss national bank for a little help. A few consecutive economic reports causing nervousness on Fraud Street? No problem, call a few more foreign central banksters for their buying power in order to “keep the market up.” What happens not if, but when, there is another 1987, or 2000, or 2008 market crash? Whose going to bail out the foreign central banks? The U.S. Fed will, which means YOU.

From Bloomberg we read…http://www.bloomberg.com/news/2012-03-01/israel-to-begin-investing-reserves-in-u-s-equities-today-1-.html

The Bank of Israel will begin today a pilot program to invest a portion of its foreign currency reserves in U.S. equities.

The investment, which in the initial phase will amount to 2 percent of the $77 billion reserves, or about $1.5 billion, will be made through UBS AG and BlackRock Inc. (BLK), Bank of Israel spokesman Yossi Saadon said in a telephone interview today. At a later stage, the investment is expected to increase to 10 percent of the reserves.

A small number of central banks have started investing part of their reserves in equities. About 9 percent of the foreign- exchange reserves of Switzerland’s central bank were invested in shares at the end of the third quarter, the Swiss bank said on its website.

The investment will be made in equity index trackers and will include between 1,500 to 2,000 shares, among them stocks like Apple Inc. (AAPL), Saadon said.

I wonder how many more will follow? Ben Bernanke is not allowed to directly invest in equities, although he certainly wants to. No matter – he can get his friends to do it…WITH a guarantee of profits. Remember, if they lose money Bailout-Ben will, umm, bail them out.

Rigged? You bet your @$$ it’s rigged. The global central banking mafia sticks together and their openly admitted goal are higher stock prices in order to boost “confidence,” which will hopefully improve the overall economies.

No wait – it’s really a “free market”…really, I promise.

Trade well and follow the trend, not the so-called “experts.”

Behold the age of infinite moral hazard! On April 2nd, 2009 CONgress forced FASB to suspend rule 157 in favor of deceitful accounting for the TBTF banksters.

- #23,364

- Mar 3, 2012 6:23am Mar 3, 2012 6:23am

- | Additional Username | Joined Oct 2011 | 2,098 Posts

After the markets closed Reuters posted an article on their website that will have MAJOR ramifications in the commodity markets. Here's the article:

Insight: Wall Street, Fed Face Off over Physical Commodities

http://www.reuters.com/article/2012/03/02/us-fed-banks-commodities-idUSTRE8211CC20120302

Here are some important passages:

"While the battle over proprietary trading and new derivatives regulations has taken place largely in public view since the 2008 financial crisis, the fight by JPMorgan Chase, Morgan Stanley and Goldman Sachs to retain or expand their prized physical commodity operations - most acquired in only the past six years - has remained hidden."

"The company is engaged in discussions with the Federal Reserve regarding its commodities activities. If the Federal Reserve were to determine that any of the company's commodities activities did not qualify for the BHC (Bank Holding Company) Act grandfather exemption, then the company would likely be required to divest any such activities."

But regulators and lawmakers may not be in the mood to give way. Banks are under pressure to reduce risk on their balance sheet; as commodity prices rise again, they may face more allegations that they could use these assets to drive prices higher or lower, squeezing them for trading profits.

"Yet it may be JPMorgan, which has eclipsed long-time market leaders Goldman and Morgan under commodities chief Blythe Masters, that will be first to feel its effects."

This is a VERY big deal. That's why it was posted on a Friday Night! If the Banksters are no longer allowed to trade in commodities the "official manipulation" of the monetary metals will end. Interestingly, it's JP Morgan and Blythe Masters that are signaled out as being "first to feel its effects"!

BUT BEWARE OF MASSIVE VOLATILITY WHILE THE BANKSTERS TRY TO CLOSE OUT THEIR POSITIONS!! UP AND DOWN!! Stay safe with your metal outside of the system. Just ride out any action.

I don't think that this story is coming out now by accident.

I think...IT'S TIME!

May the Road you choose be the Right Road.

Bix Weir

www.RoadtoRoota.com

Insight: Wall Street, Fed Face Off over Physical Commodities

http://www.reuters.com/article/2012/03/02/us-fed-banks-commodities-idUSTRE8211CC20120302

Here are some important passages:

"While the battle over proprietary trading and new derivatives regulations has taken place largely in public view since the 2008 financial crisis, the fight by JPMorgan Chase, Morgan Stanley and Goldman Sachs to retain or expand their prized physical commodity operations - most acquired in only the past six years - has remained hidden."

"The company is engaged in discussions with the Federal Reserve regarding its commodities activities. If the Federal Reserve were to determine that any of the company's commodities activities did not qualify for the BHC (Bank Holding Company) Act grandfather exemption, then the company would likely be required to divest any such activities."

But regulators and lawmakers may not be in the mood to give way. Banks are under pressure to reduce risk on their balance sheet; as commodity prices rise again, they may face more allegations that they could use these assets to drive prices higher or lower, squeezing them for trading profits.

"Yet it may be JPMorgan, which has eclipsed long-time market leaders Goldman and Morgan under commodities chief Blythe Masters, that will be first to feel its effects."

This is a VERY big deal. That's why it was posted on a Friday Night! If the Banksters are no longer allowed to trade in commodities the "official manipulation" of the monetary metals will end. Interestingly, it's JP Morgan and Blythe Masters that are signaled out as being "first to feel its effects"!

BUT BEWARE OF MASSIVE VOLATILITY WHILE THE BANKSTERS TRY TO CLOSE OUT THEIR POSITIONS!! UP AND DOWN!! Stay safe with your metal outside of the system. Just ride out any action.

I don't think that this story is coming out now by accident.

I think...IT'S TIME!

May the Road you choose be the Right Road.

Bix Weir

www.RoadtoRoota.com

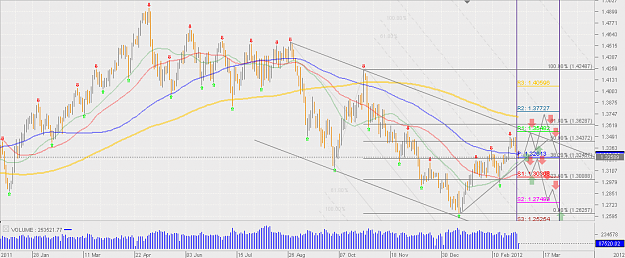

1) EUR/USD - Monthly View - March - Daily Chart

The Fiber is trending down in a Channel on the Daily chart. If We zoom out we can clearly see the Downtrend channel and the fact that EUR/USD price has retraced bullish to reach the 100 SMA and break it to reach 161.8% Pitchfork around 1.35 Level. We have almost reached the 61.8% fibonacci Retracement bullish and the Downtrend Resistence line.

Bullish Probability could find support at 1.326 (Monthly Main Pivot line, confluence with 100SMA, maybe 30 SMA and 38.2% Fibonacci Retracement bullish). This is a strong Key Level for the bullish retracement in the Main Downtrend on the Daily chart. Even if the Volume looks bearish the price could find support at this strong level and continue the bullish Retracement to reach first 1.355( Key confluence between the Main Downtrend line and the Monthly R1 Pivot).

Further, we could see a False breakout of 1.363(Important Key Level, confluence between 200SMA and 61.8% Fibonacci Retracement bullish) to reach the resistence at 1.377(Key confluence between 261.8% Pichfork and Monthly R2 Pivot). If We will have a confirmation of the False Breakout, as a candlestick Formation corroborated with strong bearish Volume, this would be a confirmation to enter short for a Downtrend Continuation.

Bearish Probability could break the 1.326 Level (Key confluence between Monthly Pivot, 100 and 30 SMAs and 38.2% Fibonacci Retracement and also 161.8% Pitchfork). Price could reach first 1.304 Level (confluence between 50SMA and Monthly S1 Pivot, and also 23.6% Fibonacci Retracement bullish), retrace back to the Monthly Pivot, and continue downside to 1.275(Monthly S2 Pivot).

Next, we could see a retracement back to 161.8% Pitchfork and then a bearish continuation to reach 1.263 Support. If this setup turns out to be a Double Bottom search for confirmation signals to enter long for a Bullish Retracement and even a Trend Reversal.

To your success,

Doctortyby

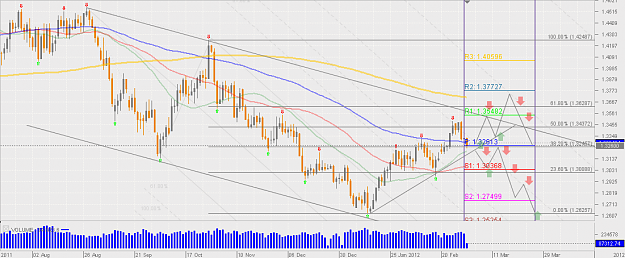

The Fiber is trending down in a Channel on the Daily chart. If We zoom out we can clearly see the Downtrend channel and the fact that EUR/USD price has retraced bullish to reach the 100 SMA and break it to reach 161.8% Pitchfork around 1.35 Level. We have almost reached the 61.8% fibonacci Retracement bullish and the Downtrend Resistence line.

Bullish Probability could find support at 1.326 (Monthly Main Pivot line, confluence with 100SMA, maybe 30 SMA and 38.2% Fibonacci Retracement bullish). This is a strong Key Level for the bullish retracement in the Main Downtrend on the Daily chart. Even if the Volume looks bearish the price could find support at this strong level and continue the bullish Retracement to reach first 1.355( Key confluence between the Main Downtrend line and the Monthly R1 Pivot).

Further, we could see a False breakout of 1.363(Important Key Level, confluence between 200SMA and 61.8% Fibonacci Retracement bullish) to reach the resistence at 1.377(Key confluence between 261.8% Pichfork and Monthly R2 Pivot). If We will have a confirmation of the False Breakout, as a candlestick Formation corroborated with strong bearish Volume, this would be a confirmation to enter short for a Downtrend Continuation.

Bearish Probability could break the 1.326 Level (Key confluence between Monthly Pivot, 100 and 30 SMAs and 38.2% Fibonacci Retracement and also 161.8% Pitchfork). Price could reach first 1.304 Level (confluence between 50SMA and Monthly S1 Pivot, and also 23.6% Fibonacci Retracement bullish), retrace back to the Monthly Pivot, and continue downside to 1.275(Monthly S2 Pivot).

Next, we could see a retracement back to 161.8% Pitchfork and then a bearish continuation to reach 1.263 Support. If this setup turns out to be a Double Bottom search for confirmation signals to enter long for a Bullish Retracement and even a Trend Reversal.

To your success,

Doctortyby

Attached Image(s) (click to enlarge)

- #23,366

- Mar 3, 2012 11:26am Mar 3, 2012 11:26am

DislikedNormally I would agree with you on this but I feel that this time will be an exception. London is not going to be bullish on the Euro. Even if they are, it will not be for very far up the chart... maybe 3250

Of course I may be completely wrong on this one but the odds are in my favor.Ignored

You are right about that. 1.33 is too far.

- #23,367

- Mar 4, 2012 6:16am Mar 4, 2012 6:16am

- | Additional Username | Joined Oct 2011 | 2,098 Posts

http://www.actionforex.com/action-in...0120303160689/

Snippet:

Weekly Review and Outlook

Euro Tumbled after ECB LTRO; Focus Back on Greece and US Data

Price actions in the fx markets last week were quite complicated as several themes had impacts simultaneously. Firstly Euro was sold off steeply after ECB's three year LTRO result as the event provided no fuel to extend recent rebound. Focus was gradually turned back to Greece.

Secondly, Bernanke refrained from giving any hints on QE3 in the semi annual testimony to congress and triggered sharp selloff in gold. However, dollar's strength was limited to against European majors and yen only.

Aussie, Kiwi and Loonie were indeed very resilient. Thirdly, yen's selloff continues as comments from BoJ as well as weak inflation data suggests that we're still far from seeing the end of Japan's QE expansion.

Euro will likely remain weak in near term at least until Greece finally get the EUR 130b bailout fund on hand and settled it's March 20 bond payments. Yen will remain weak as expectation on BoJ expanding quantitative easing continues. The main question is which of dollar and commodity currencies would out-perform. The post Bernanke stock selloff and dollar rebound was a hint that markets are going back to the buy risk on bad US data for QE3 mode. However, that's far from being confirmed as while DOW struggled to stay above 13000 level after multiple attempt, there is no reversal yet. Commodity currencies' resilience could indeed be attributed to resilience in stocks globally. Hence, this week's Non-farm payroll report would be important in determining firstly, how investors now react to US data, and secondly, whether stock markets and commodity currencies would extend rally or reverse.

The ECB has allotted 529.5B euro of 3-year LTRO to 800 banks. Together with the first auction, the central bank has injected 1trillion of 3-year funds into the system. This amount equals to 131% total European bank bond maturities in 2012 and 72% for 2012 and 2013 combined. The average allotment is 0.66B euro, compared with 1B euro in December 2011 and 0.40B euro in June 2009. The total number of bidders is huge, suggesting participation of a lot of small banks. The ECB would probably view the result as positive as it's expected that the funds will be passed to the real economy. More in ECB Allotted over 500B Euro in LTRO.

Dollar index's strong rebound last week indicates that a short term bottom is at least formed at 78.09. It's possible that whole decline from 81.78 is finished too and focus is back on 80.11 resistance. Break there should at least pave the way to retest 81.78 high. However, we'd like to point out that upside momentum is very unconvincing with bearish divergence condition in daily MACD. Hence, even though another rally is possibly, strong resistance would likely be seen at 61.8% retracement of 88.70 to 72.69 at 82.58 to finish off the whole rebound from 72.69. Meanwhile, failure at 80.11, followed by break of 78.09 will revive the case that dollar index has indeed topped out at 81.78 already.

Five central banks will meet this week, including RBA, RBNZ, BoE, ECB and BoC but none of them is expected to change policy. Main focus would indeed be on firstly, reactions to US data. ISM services, ADP and NFP would be closely watched. As speculations on QE3 cooled, investors could indeed respond negatively to positive US data. We'll see if that's the developing pattern. Second, the window of Greek PSI debt swap deal would close on Friday and markets will pay close attention to news regarding this topic.

Snippet:

Weekly Review and Outlook

Euro Tumbled after ECB LTRO; Focus Back on Greece and US Data

Price actions in the fx markets last week were quite complicated as several themes had impacts simultaneously. Firstly Euro was sold off steeply after ECB's three year LTRO result as the event provided no fuel to extend recent rebound. Focus was gradually turned back to Greece.

Secondly, Bernanke refrained from giving any hints on QE3 in the semi annual testimony to congress and triggered sharp selloff in gold. However, dollar's strength was limited to against European majors and yen only.

Aussie, Kiwi and Loonie were indeed very resilient. Thirdly, yen's selloff continues as comments from BoJ as well as weak inflation data suggests that we're still far from seeing the end of Japan's QE expansion.

Euro will likely remain weak in near term at least until Greece finally get the EUR 130b bailout fund on hand and settled it's March 20 bond payments. Yen will remain weak as expectation on BoJ expanding quantitative easing continues. The main question is which of dollar and commodity currencies would out-perform. The post Bernanke stock selloff and dollar rebound was a hint that markets are going back to the buy risk on bad US data for QE3 mode. However, that's far from being confirmed as while DOW struggled to stay above 13000 level after multiple attempt, there is no reversal yet. Commodity currencies' resilience could indeed be attributed to resilience in stocks globally. Hence, this week's Non-farm payroll report would be important in determining firstly, how investors now react to US data, and secondly, whether stock markets and commodity currencies would extend rally or reverse.

The ECB has allotted 529.5B euro of 3-year LTRO to 800 banks. Together with the first auction, the central bank has injected 1trillion of 3-year funds into the system. This amount equals to 131% total European bank bond maturities in 2012 and 72% for 2012 and 2013 combined. The average allotment is 0.66B euro, compared with 1B euro in December 2011 and 0.40B euro in June 2009. The total number of bidders is huge, suggesting participation of a lot of small banks. The ECB would probably view the result as positive as it's expected that the funds will be passed to the real economy. More in ECB Allotted over 500B Euro in LTRO.

Dollar index's strong rebound last week indicates that a short term bottom is at least formed at 78.09. It's possible that whole decline from 81.78 is finished too and focus is back on 80.11 resistance. Break there should at least pave the way to retest 81.78 high. However, we'd like to point out that upside momentum is very unconvincing with bearish divergence condition in daily MACD. Hence, even though another rally is possibly, strong resistance would likely be seen at 61.8% retracement of 88.70 to 72.69 at 82.58 to finish off the whole rebound from 72.69. Meanwhile, failure at 80.11, followed by break of 78.09 will revive the case that dollar index has indeed topped out at 81.78 already.

http://www.actionforex.com/images/st...20120303w1.gif

The Week AheadFive central banks will meet this week, including RBA, RBNZ, BoE, ECB and BoC but none of them is expected to change policy. Main focus would indeed be on firstly, reactions to US data. ISM services, ADP and NFP would be closely watched. As speculations on QE3 cooled, investors could indeed respond negatively to positive US data. We'll see if that's the developing pattern. Second, the window of Greek PSI debt swap deal would close on Friday and markets will pay close attention to news regarding this topic.

- Monday: Swiss retail sales; Eurozone Sentix investor confidence, retail sales; UK services PMI; US ISM services, factory orders

- Tuesday: RBA rate decision; Eurozone GDP revision; Canada Ivey PMI

- Wednesday: Australia GDP; Swiss unemployment, forex reserves; US ADP employment; Canada building permits

- Thursday: RBNZ rate decision; Japan GDP; Australia employment; Swiss CPI; BoE rate decision; ECB rate decision; BoC rate decision; Canada housing starts; US jobless claims

- Friday: Australia trade balance; China CPI; UK production, PPI; Canada employment; US NFP, trade balance

- #23,368

- Mar 4, 2012 7:21am Mar 4, 2012 7:21am

- | Joined Nov 2011 | Status: Trader | 2,104 Posts

So what's instore for us next week???

The last time my SlowStoch(21,9,9) was in the oversold area (Feb-16th) I suggested a bounce off the bottom of my long term daily channel (gold line on chart) and this indeed occured. We had retraced from our 1.26 lows into the channel and on several attempts we tried to break below but we didn't (Jan-26, Feb-1 and Feb-6). This continued our move up and this is where we established out 1.3285 resistance.

As it started to pull back from there, I expected it to re-test the daily channel low which gave us the SlowStoch oversold I just talked about on Feb-16th. Now the length and breath of that pull back is what I am now using as the length and breath of our next move down (which started late last week).

I first suggested that we'd go down to the bottom of the 4hr channel (blue channel lines) if 1.3285 failed. As we all know, it did fail 1.3285 and continued down for a low of 1.3185 before settling at the 1.3205/1.3193 for the remainder of the NY session.

If indeed the length and breath is an accurate prediction of what's to come, we can expect to see range bound start of the week with 1.3211 and 1.3150 as the range. However, I think this will be short lived (5 or 6 candles on the 4 hour timeframe) and we'll see a correction to the upside to test the resistance line at 1.3285.

This is because I feel we are in a raising wedge on the daily chart (blue lines) and the length and breath of the 4 hour lines, closes the range on the daily wedge.

Now let's talk about the length and breath of the upward move (the yellow line). If indeed we're heading to touch down on the daily raising wedge, one would have to think that we are going to bounce from there... So if we take the yellow line and move it to the bottom of the daily wedge, the top of the line is pretty darn close to the long term daily down trend channel (gold lines).

Now let's add one more chart to the mix, the DOW. Since October of last year we've been forming a raising wedge as well. Many analylist have been talking about it and we're now topping out at the 13000 level. Pretty much all of last week has been a sideway move with a little fanfare as we've broke and closed above 13000. Some are saying 15000 is on the horizon but I for one am not buying it. From my chart, I think that mid to late next week will be the start of a down turn in the DOW. If this does start to turn down, you can expect EUR/USD to follow suit and break to the down side of my daily wedge (blue lines on EUR/USD daily chart).

So final recap... If the move is up (with a confirmation 4H candle above 1.3285) then we might be looking at 1.3690/1.3700. If the move is down (which I favour) then we're looking at 1.2900/1.2890. These targets are for the next two weeks I think.

I'd love to hear your comments...

Cheers!

The last time my SlowStoch(21,9,9) was in the oversold area (Feb-16th) I suggested a bounce off the bottom of my long term daily channel (gold line on chart) and this indeed occured. We had retraced from our 1.26 lows into the channel and on several attempts we tried to break below but we didn't (Jan-26, Feb-1 and Feb-6). This continued our move up and this is where we established out 1.3285 resistance.

As it started to pull back from there, I expected it to re-test the daily channel low which gave us the SlowStoch oversold I just talked about on Feb-16th. Now the length and breath of that pull back is what I am now using as the length and breath of our next move down (which started late last week).

I first suggested that we'd go down to the bottom of the 4hr channel (blue channel lines) if 1.3285 failed. As we all know, it did fail 1.3285 and continued down for a low of 1.3185 before settling at the 1.3205/1.3193 for the remainder of the NY session.

If indeed the length and breath is an accurate prediction of what's to come, we can expect to see range bound start of the week with 1.3211 and 1.3150 as the range. However, I think this will be short lived (5 or 6 candles on the 4 hour timeframe) and we'll see a correction to the upside to test the resistance line at 1.3285.

This is because I feel we are in a raising wedge on the daily chart (blue lines) and the length and breath of the 4 hour lines, closes the range on the daily wedge.

Now let's talk about the length and breath of the upward move (the yellow line). If indeed we're heading to touch down on the daily raising wedge, one would have to think that we are going to bounce from there... So if we take the yellow line and move it to the bottom of the daily wedge, the top of the line is pretty darn close to the long term daily down trend channel (gold lines).

Now let's add one more chart to the mix, the DOW. Since October of last year we've been forming a raising wedge as well. Many analylist have been talking about it and we're now topping out at the 13000 level. Pretty much all of last week has been a sideway move with a little fanfare as we've broke and closed above 13000. Some are saying 15000 is on the horizon but I for one am not buying it. From my chart, I think that mid to late next week will be the start of a down turn in the DOW. If this does start to turn down, you can expect EUR/USD to follow suit and break to the down side of my daily wedge (blue lines on EUR/USD daily chart).

So final recap... If the move is up (with a confirmation 4H candle above 1.3285) then we might be looking at 1.3690/1.3700. If the move is down (which I favour) then we're looking at 1.2900/1.2890. These targets are for the next two weeks I think.

I'd love to hear your comments...

Cheers!

Attached Image(s) (click to enlarge)

I observe your reality but live my own.

- #23,369

- Mar 4, 2012 7:45am Mar 4, 2012 7:45am

- | Additional Username | Joined Oct 2011 | 2,098 Posts

Good Morning All. I cannot get the John Maudlin Article To Open In PDF Format so I will just post his key points for all to read if you are interested. The playing field has changed again and knowing the new dimensions gives you an insight into what will most likely happen and stay out of the sheep camp.

Unintended Consequences

By John Mauldin | March 3, 2012

"Illusions commend themselves to us because they save us pain and allow us to enjoy pleasure instead. We must therefore accept it without complaint when they sometimes collide with a bit of reality against which they are dashed to pieces."

– Sigmund Freud

Let me introduce Mauldin's Rule of Thumb Concerning Unintended Consequences:

For every government law hurriedly passed in response to a current or recent crisis, there will be two or more unintended consequences, which will have equal or greater negative effects then the problem it was designed to fix. A corollary is that unelected institutions are at least as bad and possibly worse than elected governments. A further corollary is that laws passed to appease a particular group, whether voters or a particular industry, will have at least three unintended consequences, most of which will eventually have the opposite effect than the intended outcomes and transfer costs to innocent bystanders.

This week we wonder about the consequences of the European Central Bank (ECB) issuing over €1 trillion in short-term loans to try and postpone a banking credit crisis and lower sovereign debt costs for certain peripheral countries in Europe. What if, instead of holding the European Monetary Union (EMU or Eurozone) together, that actually makes a breakup more likely? That would certainly fall under the rubric of unintended consequences, and be worth our time to contemplate in this week's letter.

Further, what if the group that oversees credit default swaps declares an actual sovereign debt default not to be a technical default in order to avoid a credit crisis because CDSs would have to be paid? Could that actually undermine the ability of smaller countries to borrow money at lower cost, if they could even borrow it at all? Thus making the eventual outcome even worse? We will explore these perplexing questions and more as we once again turn our attention to Europe.

Unintended Consequences

The ECB injected (created? printed?) €529.5 billion for an annual cost of 1%, more than the €489 billion they issued just last December. This was called a long-term refinancing operation, or LTRO. The total now is over €1 trillion euros (around $1.3 trillion), which can only make Ben Bernanke jealous. That money was technically issued to the various national central banks, who in turn lent it to their various commercial banks for almost any collateral that still had a pulse. Which banks in turn used it to shore up their balance sheets, and any spare change was used to buy more sovereign debt of their countries, thus financing their own government's deficits. And making a nice juicy spread for the next three years, which can help repair that balance sheet.

I can't find a chart I have permission to use and don't feel like spending three hours to make one just to show that the ECB has simply exploded in the last 6 months, swelling almost four times in that period, on a time-adjusted basis. Just imagine a slowly rising line that viciously turns north beginning July of last year. As in a "J" curve.

Did we see a rise in loans to commercial establishments? Easy money for all? Hardly.

The markets were quite happy that a credit crisis has once again been put off. So were the various governments. Did we see a rise in loans to commercial establishments? Easy money for all? Hardly. So what did the banks buy with their new money? (Besides the chance to deposit it back at the ECB?) They bought short-term government bonds, which more or less matched the terms of the money they had borrowed.

So what does a country with deficits and growing debt do? It sells lower-current-cost short-term bonds to help its current deficit (more on that later), rather than take on longer-term debt. It can also buy back more expensive longer-term debt sold last year for much lower short-term rates today.

But that means there is more roll-over risk in the very near future, as you have to borrow to replace those bonds when they mature; but why worry about that today? As my Dad was wont to say when he wanted to ignore the problems cropping up in his future, "Sufficient unto the day is the evil thereof."

I saw a table created by those clever people at Bridgewater. They analyzed the nature of the capital of the banks of various European countries. Not much has changed in the last few years, except that foreign capital is still fleeing and that capital is being replaced (almost euro for euro) by ECB debt.

Let us make no mistake, without ECB largesse, European banks would either have to sell equity at fire-sale prices or their governments would have to nationalize them. Otherwise they would be insolvent. And that would in all likelihood mean a credit crisis worse than 2008, as hard as that is to imagine.

And while many applaud Mario Draghi's actions, as they feel he has averted a crisis with his initiation of the LTRO, there are others who are not pleased.

This note from yesterday's Financial Times:

"The head of Germany's Bundesbank has launched a powerful attack on Mario Draghi, president of the European Central Bank, in a sign of mounting concern in Europe's biggest economy at measures being taken to try to contain the eurozone financial crisis.

"Jens Weidmann's warning of increasing risk stemming from some ECB policies highlights fears of potential costs for Germany from its role as the eurozone's biggest creditor nation and may spark fresh doubts about the eurozone's ability to deal with the long-running banking and sovereign debt crisis.

"Mr Weidmann, who has an influential voice on the ECB's governing council, said the central bank risked endangering its reputation and called for a quick return to stricter rules on the collateral that the ECB accepts from banks in return for central bank funds. The criticism in a letter to Mr Draghi was revealed on Wednesday by Germany's Frankfurter Allgemeine Zeitung."

Peter Sands, the head of Standard Chartered (a British commercial bank), warns that the new money runs the risk of "laying the seeds for the next crisis." He wonders what happens in three years' time when all that debt needs to be refinanced. That seems a reasonable question, as finding a spare €1 trillion will not be a lot easier in three years.

But therein lies the unintended consequence. In an effort to keep the eurozone from breaking up in the midst of a credit crisis, they may have made it easier for it to break up in the future. To understand why, let's revisit Greece a few years ago.

Was it only three years ago that the market was willing to lend Greece all the money it wanted at rates not far above those of Germany? And then it seemed like, all of a sudden, in the blink of an eye, Greece could no longer sell debt at interest rates that allowed it to credibly have a hope of repaying the debt.

And Europe had to step in and bail them out. But let's be certain of one thing. As I was writing back then, the ONLY reason that Germany, France, et al., were willing to continue to lend Greece money was that their banks had bought so much Greek debt that if they had to write it off all at once it would cost the various governments hundreds of billions. The financing package of €130 million that Greece will get? €100 billion goes right back to private bondholders, mostly banks and institutions (like insurance and pension funds). Just to create the fig leaf that there is no default. So Greek debt actually goes up, even though there is a haircut on current debt. (More on that below.)

If the only banks that held Greek debt had been Greek banks, then Europe would simply have let Greece go under, with its banks. Maybe some token help, but nothing like the amounts that have been funded. Greece would have had no choice but to leave the eurozone and return to the drachma.

I wrote at the time that we would know when German banks had essentially sold their Greek debt, written it down, or were otherwise able to handle a default, because Merkel would no longer be willing to fund Greece. That point was essentially reached a few months ago. Now Europe keeps demanding ever more austerity from Greece, and every time Greece agrees they move the line and ask for more. Greece is now going to have to demonstrate it is willing to cut spending and raise taxes, no matter what.

Greece's economy will experience deflation this year as GDP falls 4.4%, the nation's fifth straight year of recession, according to the European Commission. Greece's economy contracted 6.8% last year and 3.5% in 2010.

As recently as November, the commission forecast the Greek economy would contract just 2.8% this year. But just two weeks ago that estimate was blown away. Fourth-quarter data showed Greece had contracted by almost 7% in 2011. But they had just agreed to massive austerity cuts for the next ten years, totaling as much as their current annual GDP. In an economy where government spending is 40% of GDP. Such cuts will make it even more unlikely they can meet their targets.

So what is happening now is that European banks are slowly shedding their foreign sovereign debt and buying the sovereign debt of their own countries.

More Italian debt is coming home to Italy, Spanish debt to Spain, and so on. Given ECB funding, this process will go on for several years.

And at some point, if Spain or Italy decided to partially default, then European banks will be able to absorb the losses. If one of the peripheral countries does not get its budget in order, then it too will have to face the music of austerity and rolling recessions, just as Greece is, in order to get funding from Europe.

If, as an example, Europe decides to no longer fund Spanish debt (at the cost of German and other taxpayers) without draconian austerities, what then? Since Spanish debt will mostly be in the Spanish system (banks, insurance, pensions, etc.), if Spain decides to leave the eurozone it will be much easier on the larger European system.

I think the very fact of allowing (encouraging?) the various countries to bring the debt home to internal banks and institutions is in fact increasing the likelihood of exit from the eurozone, when a future crisis occurs . It's all well and good to talk solidarity, but continuing to fund the peripheral nations at the cost of other taxpayers, with the accompanying damage to the euro, will soon wear thin on voters in those other countries.

Far-fetched? Aren't Spain and Italy getting their act together? Kiron Sarkar makes the following points, with which I agree, so let's jump to him (courtesy of The Big Picture):

"Spain unilaterally set its 2012 budget deficit at 5.8% of GDP, much higher than the 4.4% previously agreed with the EU. The budget deficit came in at 8.5% last year, once again higher than the target of 6.0%. A ‘discussion' between Spain and the EU is inevitable, especially as (to date) the EU has insisted that Spain sticks [sic] its prior commitment. Quite an interesting development, particularly as it has come on the same day that 25 out of 27 EU countries (excluding the UK and the Czech Republic) signed up to the ‘fiscal compact' which, once approved by each country's national Parliament (Ireland will need a referendum), will introduce the German inspired ‘debt brake' into their constitutions – basically commits the 25 EU countries to reduce borrowings and, indeed, balance their budget deficits.

"Spanish unemployment rose by a massive +2.4% MoM in February, with youth (under 25) unemployment over 50%, yep that's 50%.

"The EU has a tough task. If it offers concessions to Spain, expect Portugal, Ireland, etc., etc. to submit their own ‘requests.' However, I just can't see how Spain can meet its prior commitment. Officially, GDP is forecast to be -1.0% to -1.7% this year, though in reality the actual outcome will be closer to (indeed may exceed) the more pessimistic forecasts.

"Whilst Spain is facing increasing pressures, Italy announced today that its 2011 budget deficit fell to -3.9% (-4.6% in 2010), better than the -4.0% forecast. 2011 GDP came is a marginally higher at +0.4%, (+0.3% expected). Whilst Italy entered into recession in the last Q of 2011 and its economy is expected to contract this year, Italy has pledged to balance its budget deficit by 2013.

The Final Snippet To The Article...

And Then There Is Ireland

What do the Greeks get by staying? My friend the Irish provocateur David McWilliams writes last week about how Ireland should view the Greek deal:

"For Ireland, this [the Greek deal] means that we will get a deal on bank debt most definitely. It might take time because the last thing the ECB wants is a queue of ‘me too' demands from Ireland and Portugal. But it is clear that our hand has been strengthened, if we decide to play it.

"But just in case you think this is a victory for the citizen, let's examine in a bit more detail how it works. There will be no default. Greece will be given a €130bn loan. With that loan it will pay out €100bn to bondholders, who will have seen their bonds fall 53pc in value. After the penal interest Greece has paid on these bonds already, we still see an insolvent country paying bondholders 50pc of face value when they should be getting nothing.

"So Greece gets €100bn written off, but borrows €130bn in order to achieve this, so it is still borrowing more making its overall debt not better but worse in absolute terms.

"Now it needs to grow to bring these figures down and that is going to be impossible. So we are going to be back to square one in a few years except for one crucial thing.

"After all this is done, private creditors to Greece will have been paid by European public money stumped up by the taxpayers of other European countries. The banks have been bailed out again. Without help they would have got nothing. They now get 50pc of their worthless holdings and the subsidy comes from the taxpayer."

David is going to be at the Strategic Investment Conference, as I mentioned at the beginning of the letter. I am going to give him the podium and then put him on a panel with Marc Faber (a [Swiss] Austrian economist) and maybe even the Scot Niall Ferguson, and throw some raw meat up on the stage and see what happens. It will be highly instructive and good fun as well.

You can see what McWilliams is calling "Punk Economics" at www.davidmcwilliams.ie. It is a short video clip but fascinating. He represents a growing populist strain in Europe. And he does so with Irish verve and humor. You've got to love it.

Kno's Comments: The purpose of reading this article is to get insight into what the Central Banks are doing to keep their power and the control they need to remain in power. They might actually think they are doing the right thing however in the end it will destroy lives and those unaware of what they are doing will wake up in horror never being able to prepare for the future.

Have a good trading week and stay aware as you trade each day. Patterns CHANGE when the playing field changes and new parameters are introduced while most are not aware of the new dynamics.

- #23,370

- Mar 4, 2012 7:56am Mar 4, 2012 7:56am

- | Additional Username | Joined Oct 2011 | 2,098 Posts

Now let's add one more chart to the mix, the DOW. Since October of last year we've been forming a raising wedge as well. Many analylist have been talking about it and we're now topping out at the 13000 level. Pretty much all of last week has been a sideway move with a little fanfare as we've broke and closed above 13000. Some are saying 15000 is on the horizon but I for one am not buying it. From my chart, I think that mid to late next week will be the start of a down turn in the DOW. If this does start to turn down, you can expect EUR/USD to follow suit and break to the down side of my daily wedge (blue lines on EUR/USD daily chart).

So final recap... If the move is up (with a confirmation 4H candle above 1.3285) then we might be looking at 1.3690/1.3700. If the move is down (which I favour) then we're looking at 1.2900/1.2890. These targets are for the next two weeks I think.

I'd love to hear your comments...

Cheers!

Congratulations for a very clear view of your expectations from a technical point of view. By watching other asset classes such as the Dow you combine fundamentals with technicals and money flow then will take over the movements. Keep up the excellent work and very helpful observations. You might want to start watching USD/JPY as there is a chance it might move towards 85.00 and that will have an effect on the other currencies. In particular EUR/JPY and that in turn moves EUR/USD with it.

There has been some recent correlation divergences and showing a chart of EUR/USD with a chart of EUR/JPY alongside a chart of USD/JPY over the last 60 days or since the start of 2012 will be very helpful in understanding these movements and correlations.

Have a excellent trading week and I look forward to the spring and continuing these discussions with you. Take care and trade well.

So final recap... If the move is up (with a confirmation 4H candle above 1.3285) then we might be looking at 1.3690/1.3700. If the move is down (which I favour) then we're looking at 1.2900/1.2890. These targets are for the next two weeks I think.

I'd love to hear your comments...

Cheers!

Congratulations for a very clear view of your expectations from a technical point of view. By watching other asset classes such as the Dow you combine fundamentals with technicals and money flow then will take over the movements. Keep up the excellent work and very helpful observations. You might want to start watching USD/JPY as there is a chance it might move towards 85.00 and that will have an effect on the other currencies. In particular EUR/JPY and that in turn moves EUR/USD with it.

There has been some recent correlation divergences and showing a chart of EUR/USD with a chart of EUR/JPY alongside a chart of USD/JPY over the last 60 days or since the start of 2012 will be very helpful in understanding these movements and correlations.

Have a excellent trading week and I look forward to the spring and continuing these discussions with you. Take care and trade well.

- #23,371

- Edited 8:49am Mar 4, 2012 8:12am | Edited 8:49am

- Joined Jul 2008 | Status: "Not all information is beneficial. | 1,724 Posts

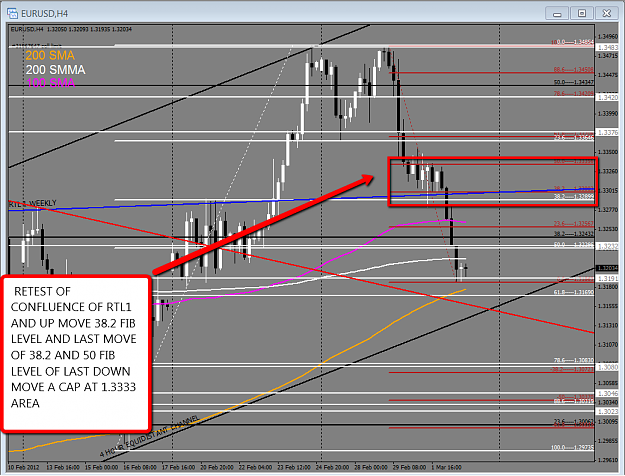

The high retrace I see would take us to the 1.3296-1.3320 area as last supply zone( 4H) and test of the rising weekly trendline 1 confluence with fibs on my chart.

Fundies may well drive the direction this week along with traders waking up and seeing the King Dow has no clothes on!

EDIT: TOP OF PAGE

Fundies may well drive the direction this week along with traders waking up and seeing the King Dow has no clothes on!

EDIT: TOP OF PAGE

Attached Image (click to enlarge)

- #23,372

- Mar 4, 2012 9:12am Mar 4, 2012 9:12am

- | Joined Nov 2011 | Status: Trader | 2,104 Posts

DislikedCongratulations for a very clear view of your expectations from a technical point of view. By watching other asset classes such as the Dow you combine fundamentals with technicals and money flow then will take over the movements. Keep up the excellent work and very helpful observations. You might want to start watching USD/JPY as there is a chance it might move towards 85.00 and that will have an effect on the other currencies. In particular EUR/JPY and that in turn moves EUR/USD with it.

There has been some recent correlation divergences and...Ignored

One thing that I have been trying to figure out is the elusive correlation you keep talking about between the EUR/USD, USD/JPY and EUR/JPY, so let me put in my two cents here.

If we look at the base JPY index (as posted on FinViz http://www.finviz.com/futures_charts.ashx?t=6J&p=h1) we can clearly see that is has been falling since the beginning of February. So if we compare other currencies to the Yen (as in xxx/JPY) one would expect those currencies to have gained against the Yen. And indeed they have as shown in USD/JPY, EUR/JPY, AUD/JPY, GBP/JPY and CHF/JPY.

So if all pairs are raising against the Yen, why is it that the EUR/USD does not have a similar inverse pattern (basically a straight line down like the straight line up on the xxx/JPY charts)?

This is where I am trying to figure out why you keep saying to watch the EUR/JPY and USD/JPY in relationship to the EUR/USD. By looking at the USD index, you can clearly see that the Euro is the inverse of the USD but the USD/JPY and EUR/JPY isn't.

So I guess the question is, why do you think a weakening Yen will give us a weaker Euro? The charts (to my eyes) don't support this.

Looking forward to your comments.

Attached Image(s) (click to enlarge)

I observe your reality but live my own.

- #23,373

- Mar 4, 2012 12:40pm Mar 4, 2012 12:40pm

- | Additional Username | Joined Oct 2011 | 2,098 Posts

A Very Thought Provoking Post By Boris K....

What do you think Fellow Traders ?

Thoughts on Trading

Size Matters

http://www.bkforexadvisors.com/wp-co...ssberg-icn.jpg

My Sometimes you trade the market, sometimes the market trades you. One of the distinguishing characteristics of our business is that our degree of certainty on any given trade is effectively zero. In other areas of life the expectations that event A will produce result B can be as high as 99%. Computer companies often gloat about uptimes of 99.999% or five nines as they like to call them.

Not so with trading.

In our line of work we operate with odds that are much much closer to those of a roulette wheel in Vegas than a computer farm in Redmond Washington. On any given day, at any given moment, even the best researched trade ideas can go horribly awry as news changes sentiment. The brutal truth of our business is that we gamble for a living, but just because we do we must never allow ourselves to become gamblers.

The current issue of the CFA Magazine has a fascinating article titled "The Financial Psychopath Next Door." Studies conducted by Canadian forensic psychologist Robert Hare indicate that about 1 percent of the general population can be categorized as psychopathic, but the prevalence rate in the financial services industry is 10 percent. And according to Christopher Bayer a well-known psychologist who provides therapy to Wall Street traders, the rate may be higher.

The article notes, "Taken to the extreme, some traders become compulsive gamblers. The behavior is often latent--neither they nor anyone else knows they have this propensity. They hide small losses and keep doubling their position to try to eliminate them. When those trades turn sour, they dig themselves into a deeper hole and deny any wrongdoing or failure. They rationalize by telling themselves that poor investment decisions are an occupational hazard. They lie to family members or others to conceal the extent of their involvement with gambling and commit forgery, fraud, theft, and embezzlement to support their habit."

The article clearly deals with extreme forms of behavior but it is applicable to anyone who has ever traded an FX lot. We are are all guilty of those sins to some extent. Which is why the longer I trade, the more I appreciate the issue of size. Size matters, but perhaps not in the way you think.

All of us who approach this business with even a modicum of professionalism, set risk limits on our trades. Generally, most short term traders never wager more than 5% on any one single idea if they want to be around for more than a month. But as traders we are constantly tempted by new setups, new patterns, new ideas. This is where size matters most. If you are experimenting with something new and interesting in your repertoire, you should never, ever, ever, allocate you standard trade size to the idea. A good rule of thumb is that you should experiment with new ideas at about 1/5th the level of your standard setup. In other words if your regular risk level is 5% ( way too high in my opinion) then your "try setup" should only use 1% of capital and never, ever, ever a penny more in addition.

In trading, it's ok to gamble, in fact it is often necessary. But just because we gamble on every trade does not mean that we should allow ourselves to devolve into degenerate gamblers on the market.

What do you think Fellow Traders ?

Thoughts on Trading

Size Matters

http://www.bkforexadvisors.com/wp-co...ssberg-icn.jpg

My Sometimes you trade the market, sometimes the market trades you. One of the distinguishing characteristics of our business is that our degree of certainty on any given trade is effectively zero. In other areas of life the expectations that event A will produce result B can be as high as 99%. Computer companies often gloat about uptimes of 99.999% or five nines as they like to call them.

Not so with trading.

In our line of work we operate with odds that are much much closer to those of a roulette wheel in Vegas than a computer farm in Redmond Washington. On any given day, at any given moment, even the best researched trade ideas can go horribly awry as news changes sentiment. The brutal truth of our business is that we gamble for a living, but just because we do we must never allow ourselves to become gamblers.

The current issue of the CFA Magazine has a fascinating article titled "The Financial Psychopath Next Door." Studies conducted by Canadian forensic psychologist Robert Hare indicate that about 1 percent of the general population can be categorized as psychopathic, but the prevalence rate in the financial services industry is 10 percent. And according to Christopher Bayer a well-known psychologist who provides therapy to Wall Street traders, the rate may be higher.

The article notes, "Taken to the extreme, some traders become compulsive gamblers. The behavior is often latent--neither they nor anyone else knows they have this propensity. They hide small losses and keep doubling their position to try to eliminate them. When those trades turn sour, they dig themselves into a deeper hole and deny any wrongdoing or failure. They rationalize by telling themselves that poor investment decisions are an occupational hazard. They lie to family members or others to conceal the extent of their involvement with gambling and commit forgery, fraud, theft, and embezzlement to support their habit."

The article clearly deals with extreme forms of behavior but it is applicable to anyone who has ever traded an FX lot. We are are all guilty of those sins to some extent. Which is why the longer I trade, the more I appreciate the issue of size. Size matters, but perhaps not in the way you think.

All of us who approach this business with even a modicum of professionalism, set risk limits on our trades. Generally, most short term traders never wager more than 5% on any one single idea if they want to be around for more than a month. But as traders we are constantly tempted by new setups, new patterns, new ideas. This is where size matters most. If you are experimenting with something new and interesting in your repertoire, you should never, ever, ever, allocate you standard trade size to the idea. A good rule of thumb is that you should experiment with new ideas at about 1/5th the level of your standard setup. In other words if your regular risk level is 5% ( way too high in my opinion) then your "try setup" should only use 1% of capital and never, ever, ever a penny more in addition.

In trading, it's ok to gamble, in fact it is often necessary. But just because we gamble on every trade does not mean that we should allow ourselves to devolve into degenerate gamblers on the market.

- #23,374

- Mar 4, 2012 1:03pm Mar 4, 2012 1:03pm

- | Additional Username | Joined Oct 2011 | 2,098 Posts

http://www.gata.org/themes/gata/imag...r-dispatch.gif

John Dizard: Gold flash crash rouses suspicions of witchcraft

http://www.gata.org/themes/gata/imag...ting_small.gif

Submitted by cpowell on 07:08AM ET Sunday, March 4, 2012. Section: Daily Dispatches

Another patronizing journalist who will never try putting hard, specific questions to central banks, even though, as he implicitly acknowledges in his final paragraph, they plot to run the world in secret. All that is just to be taken for granted ... at least by journalists like himself.

* * *

Gold Flash Crash Rouses Suspicions of Witchcraft

By John Dizard

Financial Times, London

Sunday, March 4, 2012

http://www.ft.com/intl/cms/s/0/21be0...44feabdc0.html

As they say, a paranoid is someone who suspects nine of the five conspiracies against him. Last week was a feverish one for the more sensitive gold specu ... investors, with a "flash crash" on Wednesday interrupting what had been a stately procession since December to ever-higher highs. Since gold people believe their positions represent not just an investment, but virtue itself, the losers smell witchcraft, and particularly evil Fed witchcraft at that.

What does the gold crash mean, if anything? Was it the result of a conspiracy by short sellers, or, conversely, does it presage another crisis, as gold price declines did in mid-2008 and September of last year?

The $90-plus an ounce sell-off, from a high of $1,790 early in the London trading day came during Federal Reserve chairman Ben Bernanke’s testimony/grovelling to Congress last Wednesday. Taking into account the further declines in after-hours trading, the 6 per cent plus hit cut this year's gold gains by about half.

The chairman had just finished saying that the decline in the unemployment rate was "somewhat more rapid than might have been expected," and, shortly after, that "... it will be especially important to evaluate incoming information to assess the underlying pace of economic recovery."

To most, these sound like bland, rather than momentous, statements. However, the day's news cycle, and market tacticians, needed an event to excuse more churning of the customers' accounts, so Mr Bernanke's testimony was taken to mean that the Fed was postponing the start of a new round of quantitative easing of monetary policy. So less cheap money to support risk, and less future inflation.

Apparently, someone, or, rather, two someones with proprietary trading algorithms decided it was time to sell the futures equivalent of 31 tonnes of gold on the Chicago Mercantile Exchange. The crash happened between 10:40 a.m. and 10:54 a.m. eastern US time, with the biggest part of the decline taking place between 10:43 and 10:44, with a further drop in the couple of minutes before 10:54.

Wall Street's religion is chart-reading. But which chart? The one with Japanese candlesticks and outside days? The one with moving average crossovers? Or, for those traders who finished school, applications of cross-asset-class generalised autoregressive conditional heteroskedasticity models?

Nicholas Glinsman, a hedge fund manager in Taubate, Brazil, says: "These large (gold) sell-offs on big volume usually precede market liquidity events." ["Liquidity event" in this context means a widespread lack of ready money to cover immediate obligations.] "In anticipation of those, people have to raise cash somewhere, and that's by selling something in which they've made a lot of money. This happened last September (before the worst part of the European crisis), and, more dramatically, from July of 2008 up to the Lehman crisis of October 2008."

There is something to this. I remember how dollar-short European banks' sales led to a counterintuitive gold price decline in the middle of a panic.

David Goldman, a highly innovative New York fixed-income strategist, has tested a wide range of gold price time series correlations. He makes a strong case that the metal's closest relative (for now) is the yield on US Treasury Tips, the inflation indexed bonds.

"Tips and gold are high-correlated," he says. "They are both deep out of the money options on catastrophic changes in the price level." However, because Tips pay par at maturity (unlike some of their European counterpart inflation linkers), they also protect against deflation. This payoff on either inflation or deflation is so valuable that at the moment the 10-year Tips trades at a negative yield.

As Mr Goldman points out, the two asset classes are so close that they trade very tightly on a minute-by-minute or tick-by-tick basis, as well as over longer time periods. I don't think there are people trading the Tips/gold basis with offsetting long and short positions. However, there are probably long-only portfolio allocators who are rapidly changing their relative positions in Tips and gold.

Geeky enough for you yet?

This persistent pattern of high correlation makes Mr Goldman sceptical that last week's gold flash crash is anything more than a couple of clumsy hedge funds unloading excessively large positions. As he points out, it took an eternity, from 10:54 a.m. Eastern Time all the way to 11.20 a.m., for the Tips market to follow the gold price down. And when Tips did sell off, they did so far more gently. "The Tips market tells us this wasn't all that significant. If it were a general change in perception, then you have seen more happen (faster) in Tips."

My own view is that the Fed, like any bureaucracy, has tons of plans but doesn't really know what it will do next. When QE3 happens, it will be in reaction to immediately preceding outside-the-model events, justified with tortuous rationalisations.

John Dizard: Gold flash crash rouses suspicions of witchcraft

http://www.gata.org/themes/gata/imag...ting_small.gif

Submitted by cpowell on 07:08AM ET Sunday, March 4, 2012. Section: Daily Dispatches

Another patronizing journalist who will never try putting hard, specific questions to central banks, even though, as he implicitly acknowledges in his final paragraph, they plot to run the world in secret. All that is just to be taken for granted ... at least by journalists like himself.

* * *

Gold Flash Crash Rouses Suspicions of Witchcraft

By John Dizard

Financial Times, London

Sunday, March 4, 2012

http://www.ft.com/intl/cms/s/0/21be0...44feabdc0.html

As they say, a paranoid is someone who suspects nine of the five conspiracies against him. Last week was a feverish one for the more sensitive gold specu ... investors, with a "flash crash" on Wednesday interrupting what had been a stately procession since December to ever-higher highs. Since gold people believe their positions represent not just an investment, but virtue itself, the losers smell witchcraft, and particularly evil Fed witchcraft at that.

What does the gold crash mean, if anything? Was it the result of a conspiracy by short sellers, or, conversely, does it presage another crisis, as gold price declines did in mid-2008 and September of last year?

The $90-plus an ounce sell-off, from a high of $1,790 early in the London trading day came during Federal Reserve chairman Ben Bernanke’s testimony/grovelling to Congress last Wednesday. Taking into account the further declines in after-hours trading, the 6 per cent plus hit cut this year's gold gains by about half.

The chairman had just finished saying that the decline in the unemployment rate was "somewhat more rapid than might have been expected," and, shortly after, that "... it will be especially important to evaluate incoming information to assess the underlying pace of economic recovery."

To most, these sound like bland, rather than momentous, statements. However, the day's news cycle, and market tacticians, needed an event to excuse more churning of the customers' accounts, so Mr Bernanke's testimony was taken to mean that the Fed was postponing the start of a new round of quantitative easing of monetary policy. So less cheap money to support risk, and less future inflation.

Apparently, someone, or, rather, two someones with proprietary trading algorithms decided it was time to sell the futures equivalent of 31 tonnes of gold on the Chicago Mercantile Exchange. The crash happened between 10:40 a.m. and 10:54 a.m. eastern US time, with the biggest part of the decline taking place between 10:43 and 10:44, with a further drop in the couple of minutes before 10:54.

Wall Street's religion is chart-reading. But which chart? The one with Japanese candlesticks and outside days? The one with moving average crossovers? Or, for those traders who finished school, applications of cross-asset-class generalised autoregressive conditional heteroskedasticity models?

Nicholas Glinsman, a hedge fund manager in Taubate, Brazil, says: "These large (gold) sell-offs on big volume usually precede market liquidity events." ["Liquidity event" in this context means a widespread lack of ready money to cover immediate obligations.] "In anticipation of those, people have to raise cash somewhere, and that's by selling something in which they've made a lot of money. This happened last September (before the worst part of the European crisis), and, more dramatically, from July of 2008 up to the Lehman crisis of October 2008."

There is something to this. I remember how dollar-short European banks' sales led to a counterintuitive gold price decline in the middle of a panic.

David Goldman, a highly innovative New York fixed-income strategist, has tested a wide range of gold price time series correlations. He makes a strong case that the metal's closest relative (for now) is the yield on US Treasury Tips, the inflation indexed bonds.

"Tips and gold are high-correlated," he says. "They are both deep out of the money options on catastrophic changes in the price level." However, because Tips pay par at maturity (unlike some of their European counterpart inflation linkers), they also protect against deflation. This payoff on either inflation or deflation is so valuable that at the moment the 10-year Tips trades at a negative yield.

As Mr Goldman points out, the two asset classes are so close that they trade very tightly on a minute-by-minute or tick-by-tick basis, as well as over longer time periods. I don't think there are people trading the Tips/gold basis with offsetting long and short positions. However, there are probably long-only portfolio allocators who are rapidly changing their relative positions in Tips and gold.

Geeky enough for you yet?

This persistent pattern of high correlation makes Mr Goldman sceptical that last week's gold flash crash is anything more than a couple of clumsy hedge funds unloading excessively large positions. As he points out, it took an eternity, from 10:54 a.m. Eastern Time all the way to 11.20 a.m., for the Tips market to follow the gold price down. And when Tips did sell off, they did so far more gently. "The Tips market tells us this wasn't all that significant. If it were a general change in perception, then you have seen more happen (faster) in Tips."

My own view is that the Fed, like any bureaucracy, has tons of plans but doesn't really know what it will do next. When QE3 happens, it will be in reaction to immediately preceding outside-the-model events, justified with tortuous rationalisations.

- #23,375

- Mar 4, 2012 1:10pm Mar 4, 2012 1:10pm

- | Additional Username | Joined Oct 2011 | 2,098 Posts

In The News Today

March 3, 2012, at 10:06 am

by Jim Sinclair in the category In The News |

Jim Sinclair’s Commentary

The important unanswered question is "Where is the money coming from?"

The answer is from the global Western world lender of last resort, the US Federal Reserve. This was just proven.

As far as the dollar is concerned, no one is focused on the "utilization" that is fading fast and will negatively impact the value of the US dollar in 2012.

http://www.jsmineset.com/

March 3, 2012, at 10:06 am

by Jim Sinclair in the category In The News |

Jim Sinclair’s Commentary

The important unanswered question is "Where is the money coming from?"

The answer is from the global Western world lender of last resort, the US Federal Reserve. This was just proven.

As far as the dollar is concerned, no one is focused on the "utilization" that is fading fast and will negatively impact the value of the US dollar in 2012.

Inserted Video

http://www.jsmineset.com/

- #23,376

- Edited 1:22pm Mar 4, 2012 1:18pm | Edited 1:22pm

- | Additional Username | Joined Oct 2011 | 2,098 Posts

Mises Canada Daily

The Death of the Credit Default Swap

Mar 04, 2012 12:17 am by James E. Miller posted in Banking, Capitalism, credit default swaps, Eurozone Crisis, Greece

Warren Buffet must be crying tears of joy after last week’s announcement where The International Swaps and Derivatives basically destroyed the function of a credit default swap. Via the New York Times:

I concur wholeheartedly with Big Picture blogger Barry Ritholtz:

This may not constitute default by CDS standards (nothing does anymore apparently) but the promises of utopia made by politicians will inevitably bring government balance sheets to their knees the world over. Greece and the rest of the PIIGS are just the beginning.

Since credit default swaps are a weapon against the bad habits of the political class and the special privileges granted to the banking industry, they continue to be regarded as a great evil by those who benefit from the state. If banks refrained from engaging in the practice of extending unbacked credit or governments didn’t spend more than they take in, credit default swaps would not have been widely used to speculate on their solvency.

Now, the CDS market may have just met an early death despite the Greece government clearly defaulting on its debt. One more tool to fight Leviathan’s growth might have been removed but no doubt others will develop as to ensure a market for betting on the solvency of over extended states and banks. Capitalism, when not regulated into the ground, works in spontaneous and mysterious ways. Silver linings exist in almost any situation if you look hard enough. With the CDS market effectively rendered useless, perhaps government bonds will lose their appeal to the investor class. This can only be a good thing as it means less money flowing into the coffers of unproductivity.

James E. Miller holds a BS in public administration with a minor in business from Shippensburg University, PA. He is a former staff columnist to the Shippensburg Slate and current contributor to his hometown newspaper, the Middletown Press and Journal. Read his blog.

News Flash...

Sunday, March 4, 2012 9:07:14 AM

9:07 AM Greece is on course to default, as it looks set to fall short of the 95% agreement it needs from private creditors to secure its bond swap and thus its 2nd bailout, The Daily Telegraph reports. Athens is ready to use collective action clauses (CAC) to impose the deal if it receives 66% approval, which is likely to prompt ratings agencies to declare default. [See more on Global & FX, Top Stories or comment on this.]

The Death of the Credit Default Swap

Mar 04, 2012 12:17 am by James E. Miller posted in Banking, Capitalism, credit default swaps, Eurozone Crisis, Greece

Warren Buffet must be crying tears of joy after last week’s announcement where The International Swaps and Derivatives basically destroyed the function of a credit default swap. Via the New York Times:

The International Swaps and Derivatives Association said on Thursday that based on current evidence the Greek bailout would not prompt payments on the credit-default swaps linked to the country’s bonds.

I concur wholeheartedly with Big Picture blogger Barry Ritholtz:

The claim that Greece has not defaulted — despite refusing to make good on their obligations in full or on time — is utterly laughable.

In order to get paid on a default, you need a committee to evaluate whether or not failing to make payments is a — WTF?!? — default? Even more ridiculous, the committee is composed of biased, interested parties with positions in the aforementioned securities? However, sound economic analysis reveals that CDS are fully compatible with the principles of the free market, and that CDS are not to blame for the disintegration of credit markets—with their tumbling banks, struggling private borrowers and increasingly overstretched government finances. The truth is that CDS provide investors with an efficient and effective instrument for exposing economically unsound and unsustainable fiat money regimes and the economic production structure it creates—which, in turn, provokes a (n intellectual) counterattack from government officials (and their “court intellectuals”), who argue for regulating or even banning CDS.

ISDA: After this ****show, why on earth would anyone EVER want to own an asset class that requires you to determine payout? Indeed, why should ANYONE ever buy a derivative again?

Indeed, who in their right mind would buy a CDS ever again after its sole purpose has now been relegated to the irrelevance due to the decision of one group? It’s the equivalent of purchasing car insurance, being side swiped by another driver, and then having the insurance company renege on paying out. Depending on the contract, such could be fraud punishable by legal arbitration; not to mention a good way to run a company into the ground. This latest decision by the ISDA has most likely put a death nail in the CDS market as we know it. Those who see the financial industry as the embodiment of all that is unholy and in dire need of divine regulation from those elected angels in the halls of Congress, such as George Soros, are ecstatic at this probability.

Yet credit default swaps are in no way shape or form an instrument to be demonized. As Thorsten Polleit and Jonathan Mariano explain:

Credit default swaps, at their core, are a bet against the solvency of an institution. If they are to be criticized and heavily regulated, than any game of chance involving monetary payments is to be as well. The same goes for speculators who risk their own capital in trying to forecast future market signals in an efficient manner.

Basically, those who see credit default swaps and speculators as the enemies of mankind have their verbal knives pointed at entrepreneurs attempting to smooth out market fluctuations at a profit.

Since market information is widely dispersed between individuals, preventing the free flow of interaction between market participants cuts down on the efficient allocation of goods and resources. From Freidrich Hayek’s invaluable The Use of Knowledge in Society:

It is with respect to this that practically every individual has some advantage over all others because he possesses unique information of which beneficial use might be made, but of which use can be made only if the decisions depending on it are left to him or are made with his active coöperation.

This may not constitute default by CDS standards (nothing does anymore apparently) but the promises of utopia made by politicians will inevitably bring government balance sheets to their knees the world over. Greece and the rest of the PIIGS are just the beginning.

Since credit default swaps are a weapon against the bad habits of the political class and the special privileges granted to the banking industry, they continue to be regarded as a great evil by those who benefit from the state. If banks refrained from engaging in the practice of extending unbacked credit or governments didn’t spend more than they take in, credit default swaps would not have been widely used to speculate on their solvency.

Now, the CDS market may have just met an early death despite the Greece government clearly defaulting on its debt. One more tool to fight Leviathan’s growth might have been removed but no doubt others will develop as to ensure a market for betting on the solvency of over extended states and banks. Capitalism, when not regulated into the ground, works in spontaneous and mysterious ways. Silver linings exist in almost any situation if you look hard enough. With the CDS market effectively rendered useless, perhaps government bonds will lose their appeal to the investor class. This can only be a good thing as it means less money flowing into the coffers of unproductivity.

James E. Miller holds a BS in public administration with a minor in business from Shippensburg University, PA. He is a former staff columnist to the Shippensburg Slate and current contributor to his hometown newspaper, the Middletown Press and Journal. Read his blog.

News Flash...

Sunday, March 4, 2012 9:07:14 AM

9:07 AM Greece is on course to default, as it looks set to fall short of the 95% agreement it needs from private creditors to secure its bond swap and thus its 2nd bailout, The Daily Telegraph reports. Athens is ready to use collective action clauses (CAC) to impose the deal if it receives 66% approval, which is likely to prompt ratings agencies to declare default. [See more on Global & FX, Top Stories or comment on this.]

- #23,377

- Edited 1:28pm Mar 4, 2012 1:25pm | Edited 1:28pm

- | Additional Username | Joined Oct 2011 | 2,098 Posts

Today - Sunday, March 4, 2012

10:47 AM China's February services PMI slides to 48.4 from 52.9 previously, reports the CFLP, attributing the fall to the business lull following January's Spring Festival holidays. The sub-index of new orders fell to 46.1 from 48.5. 11 Comments

10:38 AM CIC - China's sovereign wealth fund - receives a $30B capital boost from the government. Eurocrats may be licking their chops hoping to get a piece of that to bankroll their bailouts, but thus far fund chairman Lou Jiwei has shown more interest in profitable investments than funding troubled EU states. 1 Comment

10:25 AM Beijing announces an 11.2% increase in its military budget, pushing defense spending above $100B for the first time (U.S. = $740B). "China has 1.3B people, a large territory and long coastline, but our defense spending is relatively low compared with other major countries," says lawmaker Li Zhaoxing. 5 Comments

10:23 AM Greece may need a 3rd bailout of €50B as soon as 2015 according to a draft of the recent Troika report on the country, reports Der Spiegel. This unpleasantry was left out of the final report under pressure from the German government. 7 Comments

10:21 AM Thirty-seven percent of Irish voters say they will vote in favor of the new EU fiscal compact, with a near equal amount either undecided or saying their support is conditional on better bailout terms. A full 61% believe the economy will only recover if the country is allowed a debt restructuring. Comment!

9:07 AM Greece is on course to default, as it looks set to fall short of the 95% agreement it needs from private creditors to secure its bond swap, The Daily Telegraph reports. Athens is ready to use collective action clauses (CAC) to impose the deal if it receives 66% approval, which is likely to prompt ratings agencies and the ISDA to declare default. 17 Comments

6:50 AM As the West ratchets up sanctions against Iran, which have already hurt the country's economy, loyalists of Ayatollah Ali Khamenei win 75% of the seats in parliamentary elections, turning Mahmoud Ahmadinejad into a lame-duck president. With reformists sitting out, the results are unlikely to bring much of a change to Iran's foreign policy. 1 Comment

5:42 AM Vladimir Putin is expected to regain Russia's Presidency in today's election despite major protests against his rule over the past few months. While critics have questioned the legitimacy of the vote, Russian markets have risen in anticipation of an end to any small uncertainty that may have deterred investors. 2 Comments

http://seekingalpha.com/currents/glo...il_rt_mc&ifp=0

10:47 AM China's February services PMI slides to 48.4 from 52.9 previously, reports the CFLP, attributing the fall to the business lull following January's Spring Festival holidays. The sub-index of new orders fell to 46.1 from 48.5. 11 Comments

10:38 AM CIC - China's sovereign wealth fund - receives a $30B capital boost from the government. Eurocrats may be licking their chops hoping to get a piece of that to bankroll their bailouts, but thus far fund chairman Lou Jiwei has shown more interest in profitable investments than funding troubled EU states. 1 Comment