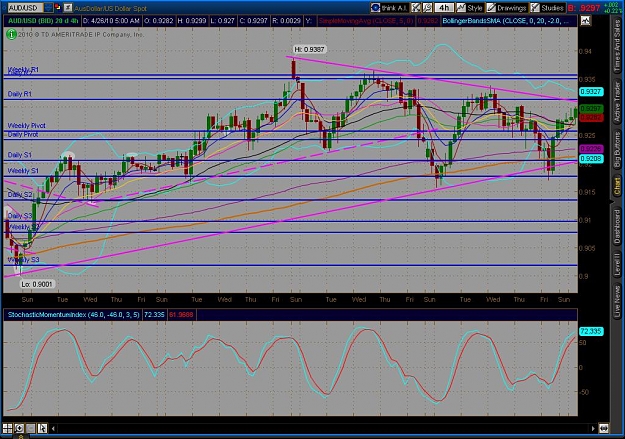

Hey Marc,

Since you are a big follower of AU, I thought I would run my first UIRP (Uncovered Interest Rate Parity) Condition analysis on AU. For UIRP equation E(FXn) = FX0((1+IR AU)/(1+IR US)^n

FX0(not) is equal to spot

E(FXn) is equal to expected rate at time n

N is equal to time period

IR AU is equal to the AU Interest Rate

IR US is equal to the US Interest Rate

Using .0833 as my n or 1 month the E(FX(.0833)) is at .931031

2 month is .934071

3 month is .937121

This is all assuming no IR changes.

I just got bored and though I would test out 1 month AU rate

Since you are a big follower of AU, I thought I would run my first UIRP (Uncovered Interest Rate Parity) Condition analysis on AU. For UIRP equation E(FXn) = FX0((1+IR AU)/(1+IR US)^n

FX0(not) is equal to spot

E(FXn) is equal to expected rate at time n

N is equal to time period

IR AU is equal to the AU Interest Rate

IR US is equal to the US Interest Rate

Using .0833 as my n or 1 month the E(FX(.0833)) is at .931031

2 month is .934071

3 month is .937121

This is all assuming no IR changes.

I just got bored and though I would test out 1 month AU rate