The Political Economy of the JPY New York, January 21. Mr. Geithner opened his congressional testimony by saying that economic stimulus should be large and quick because the system is still under considerable stress and the capital markets need support. Needless to say, stocks did not like that very much. The sell off in stokcs came at a time when JPY buying was already in full swing. The good news is that, as if reading from his Paul Krugman (rather, Paul Samuelson) textbook, Mr. Geithner said the flexible exchange rates are best system for the global economy. This put an exclamation point on today"s JPY buying. The willingness of the market to test the BOJ and this 20th century philosophy will be a much more meaningful now that T-bill rates are at 0.00%. Sadly, the theory assumes adequate global capital and on-oing, freely flowing capital markets. Of course, the old saying about when you "assume" may ring true here. The markets may prove Mr Geithner, once again, na ve even before he starts his new job.

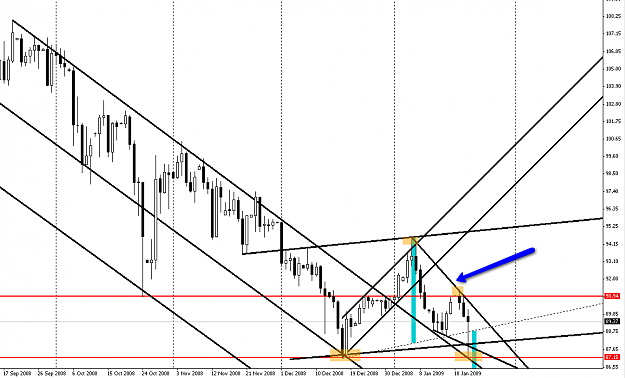

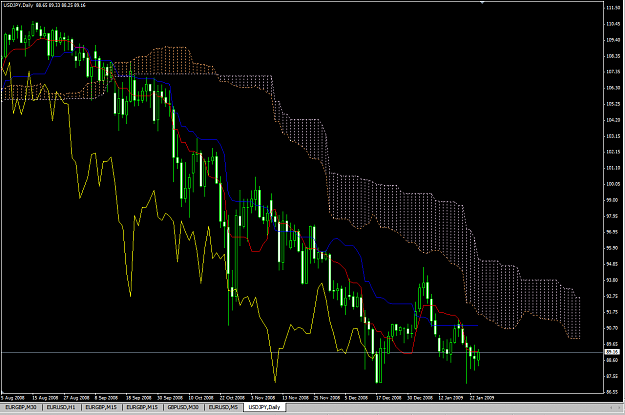

Regarding intervention, the JPY is up about 2% versus most currencies and 3.25% against GBP today. On the week, the JPY is up 1.20% versus the USD, 4% versus the EUR, and 7% versus GBP. Year-to-date, the JPY is up 3%, 11%, and 9%, respectively. At what point does the rise become too volatile for the MOF? The answer may be that volatility does not matter; levels do. With every treasury department and central bank now relying on devalued exchange rates to do its economic dirty work, concepts like PPP and fair value come back into play. The MacPPP for JPY is 78 and for EUR is 1.06. The real exchange rate concept would have USD/JPY trading closer to 96.00. In either case, the markets are looking for cash and they found it in Asia.

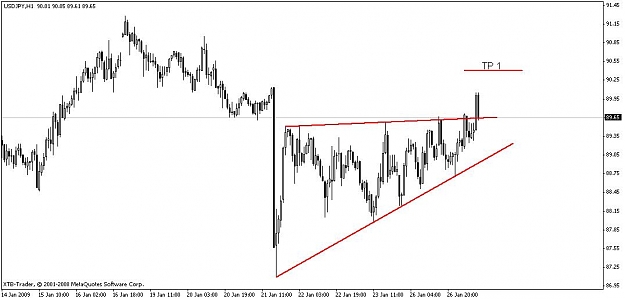

For hints on intervention, look at levels that fail to break rather than guessing about outright intervention. The latter would likely be perceived as politically unacceptable. As an example the former, the December 17 low of 87.11 was a good level for JPY longs to take profit today. If there are solid BOJ bids there, a retest is in order. Is Mr. Geithner, or rather Mr. Trichet since there is no uniform finance minister, listening?

Regarding intervention, the JPY is up about 2% versus most currencies and 3.25% against GBP today. On the week, the JPY is up 1.20% versus the USD, 4% versus the EUR, and 7% versus GBP. Year-to-date, the JPY is up 3%, 11%, and 9%, respectively. At what point does the rise become too volatile for the MOF? The answer may be that volatility does not matter; levels do. With every treasury department and central bank now relying on devalued exchange rates to do its economic dirty work, concepts like PPP and fair value come back into play. The MacPPP for JPY is 78 and for EUR is 1.06. The real exchange rate concept would have USD/JPY trading closer to 96.00. In either case, the markets are looking for cash and they found it in Asia.

For hints on intervention, look at levels that fail to break rather than guessing about outright intervention. The latter would likely be perceived as politically unacceptable. As an example the former, the December 17 low of 87.11 was a good level for JPY longs to take profit today. If there are solid BOJ bids there, a retest is in order. Is Mr. Geithner, or rather Mr. Trichet since there is no uniform finance minister, listening?