{quote} Oh, but ChatGPT assumes that you are providing the tick data... You can upload that to Perplexity too, and ask Perplexity Labs to create an interactive backtesting app for you, for example.

{quote} Oh, but ChatGPT assumes that you are providing the tick data... You can upload that to Perplexity too, and ask Perplexity Labs to create an interactive backtesting app for you, for example.

Ignored

Hmm. The first backtest with the current version of RandomOrderEA is still far from the results Perplexity is reporting. I've done several backtest-runs because of the different distributions of random orders, but the results are all negative so far.

- NQ 1-Minute Chart

- 1% of current equity per order

- Random BUY/SELL entry every 30 minutes during RTH

- Stop Loss = -10 points

- Trailing Take Profit = +30 points with a 10-point trailing step

- Max. 3 consecutive daily losses

- Max. -3% Daily Drawdown

- Max. -6% Weekly Drawdown

{quote} Hmm. The first backtest with the current version of RandomOrderEA is still far from the results Perplexity is reporting... {image}

Ignored

Thank you for sharing your results. Honestly, I expected those results, as an edge purely from the risk/reward ratio is unlikely. Maybe there is a small edge to the long side, as the skew of the underlying is upwards over the years, but will hardly overcome the trading costs.

{quote} Thank you for sharing your results. Honestly, I expected those results, as an edge purely from the risk/reward ratio is unlikely. Maybe there is a small edge to the long side, as the skew of the underlying is upwards over the years, but will hardly overcome the trading costs. Grüße aus dem Rheinland

Ignored

Hehe noch ein Rheinländer

I'm not yet sure if the EA I programmed followed the described rules as precisely as outlined in the Perplexity PDF (since some of them are somewhat vaguely defined). I tried to recreate it as best I could. I'd like to check this more thoroughly. Unfortunately, I don't currently know exactly what instructions Medici gave Perplexity to produce such a nice strategy description with all the rules, performance metrics, graphs and so on. I've done some reading, but I haven't been able to replicate the exact AI prompt yet.

Medici said they can be good "pointers," but honestly, if I replicate such a strategy exactly and don't even come close to the performance figures that Perplexity spits out, I wonder how trustworthy the AI is when it comes to strategy development and backtesting. I don't know if it's due to the data the AI used for testing (or whether it actually used real historical data for an accurate backtest the results are simply fabricated). Or maybe eben the described strategy rules in that PDF are completely different from what I've tested so far.

Meanwhile, my ORB system has achieved a +17% return so far under -5.3% Max DD, and that's not solely attributable to Gold. The DAX seems to be getting closer to the same profitability. Nastaq is disappointing.

Gold: +7.8%

GER30: +7.3%

NAS100: +1.0%

I still have no idea if or how I'll achieve my goals of finally being able to live off this someday. Not only do I seem to lack a good strategy, but also the necessary capital, and I can't seem to find any effective help on how to proceed without "wasting" more years of my life.

{quote} I wonder how trustworthy the AI is when it comes to strategy development and backtesting

Ignored

I think, that's the point, but nevetheless and out of curiosity, I will set up this stragegy in my EA framework. The we have a second set of results, that either confirm you findings or reveal a discrepancy in the rules.

{quote} I think, that's the point, but nevetheless and out of curiosity, I will set up this stragegy in my EA framework. The we have a second set of results, that either confirm you findings or reveal a discrepancy in the rules.

Ignored

Thanks a lot. Yes, I wanted to share my EA on it too, but if it has absolutely no positive expected value, I don't want to waste people's time with it.

I just asked Perplexity the following question:

Do a comprehensive backtest evaluating a random-entry trading strategy

The answer was:

Quote

Disliked

A comprehensive backtest of a random-entry trading strategy over one trading year shows the following results: The strategy randomly enters long positions with a 10% daily chance, holding each trade for up to 5 days or until a 2% stop loss is hit. Despite the randomness, this approach yielded a surprisingly high cumulative return and Sharpe ratio in the simulated scenario. If you want, the strategy can be further analyzed or optimized with different parameters or compared to benchmark strategies. Let me know if you need additional details or visualizations....

In which market was this backtest conducted?

The answer was:

Quote

Disliked

The backtest is based on synthetically generated price data that does not represent any specific real-world market or financial instrument. The price data was generated using a simulated daily return pattern to demonstrate the functionality of the random entry strategy. Therefore, it is a purely hypothetical simulation with no reference to an actual market. If desired, the backtest can be performed using historical data for a specific market or instrument.

This likely explains the overwhelmingly positive results mentioned in the original PDF "Optimal Trade Management and Money Management Strategy.pdf," where Perplexity cites a "31.547% return with only 4.4% maximum drawdown."

Apparently, Perplexity had a rather unrealistic summer night's dream

{quote} Thanks a lot. Yes, I wanted to share my EA on it too, but if it has absolutely no positive expected value, I don't want to waste people's time with it. I just asked Perplexity the following question: Do a comprehensive backtest evaluating a random-entry trading strategy The answer was: {quote} In which market was this backtest conducted? The answer was: {quote} This likely explains the overwhelmingly positive results mentioned in the original PDF "Optimal Trade Management and Money Management Strategy.pdf," where Perplexity cites...

Ignored

If you want to share, share only losing EAs

Trading is a game of impermanence. Edges appear, get discovered, and disappear — often faster than we expect.

Full article from Raen :

Edges aren’t meant to last

In trading, everyone is chasing the same thing: an edge. That small, consistent advantage that lets you make money. But here’s the uncomfortable truth — no trading edge lasts forever.

A note worth reading

Our CEO Ryan Wright recently released a Substack on this entitled:

It is worth reading. But as I ever search for topics to write on, I thought I’d add my experience in this having seen it in practice for over 25 years. Some good old war stories as it were!

The pattern we spotted

Going back to 2008 (ish) I had two young traders on my desk, one of whom went on to be fairly public, but at this point were at the start of their careers. They noticed a pattern that occurred around the close of European indices. The S&P, mostly collapsing as we started to enter the Financial Crisis period, seemed to begin to have no influence on the DAX. The DAX just refused to follow suit and in some instances went up.

Trading it in real time

Then the next morning, having been propped up all night, the DAX would adjust and open sharply lower, catching up to the S&P on the open. They spotted this for a few days then asked if they could trade it, holding overnight.

Size fast, bank it

It went on to be later found out that a rogue trader called Jérôme Kerviel had been so long in the DAX, unauthorised, that to afford the margin requirements and obscure his P&L he was artificially holding the DAX higher.

However, that's not the point. The point is that over a week these two traders spotted it and then began trading it. They didn’t worry about how long it would last. They just started to trade.

They then ramped up their size very, very quickly.

I would say it was a major turning point in their careers. They went from small five-figure accounts to very large six (close to seven)-figure accounts.

When the music stops

And then it stopped. I can’t exactly recall but it may have only lasted a couple of weeks, certainly no more than three. Kerviel got found out. SocGen management unwound the positions and the edge disappeared.

The lesson

My traders’ profits didn’t. They moved on, using their newly-found wealthy trading accounts to capitalize on the remaining period of the Financial Crisis. And that is the point. Edges do come and go. I’ve seen so many of them drift in and out over the years.

Yet the consistent point for all of the traders who “make hay when the sun is shining” is that they don’t spend time worrying about the edge lasting or what they may do if it disappears. They run with it, bank the profits, and make peace with the nature of the game.

Edges can disappear for a number of reasons

Markets adapt faster than ever. They evolve.

As soon as a strategy starts showing reliable profits, it attracts attention. Liquidity floods in, spreads tighten, and the inefficiency that gave you an edge vanishes. Think of it like a gold rush: the first few miners strike it rich, but soon the crowd arrives, and all that’s left is dirt.

Data and technology flatten the playing field.

The democratization of technology makes it harder to stay unique — and edges born from superior tech tend to decay quickly.

Behavioral edges fade as traders get smarter.

Once enough traders recognize a behavioral bias (say, overreaction after earnings), they start trading against it. As more people act on the same insight, the edge self-destructs.

The “feedback loop” problem.

Success can destroy your own edge. When a strategy performs well, traders often scale up — increasing position sizes, running the same signals across more assets, or publicizing results to attract capital. That attention leads to crowding. In short, your own success can be the seed of your downfall.

Structural changes reset the game.

Regulations, macro shifts, and new market structures constantly reshape the landscape. A strategy that worked in the low-volatility era of 2015–2019 might collapse in a regime of higher inflation and interest rates. Edges are often regime-dependent, thriving only under certain conditions — and dying when those conditions change.

How Do You Stay Ahead?

Keep evolving. Treat every strategy as temporary. Continuously research, test, and adapt. Don’t overly worry about what may or may not be in the future. Focus on the now. The one good trade, right here, right now.

Accept the game you chose to play. Acceptance is the beginning. Once you can accept what is, you can stop trying to change the unchangeable. It will give you the freedom to take advantage of the opportunity in front of you in its entirety. With that sort of single-minded focus you can avoid the pitfall of wishing you had taken advantage of the situation in hindsight — and in turn avoid the loop of repeating the same mistake when the next opportunity comes knocking.

Stay humble. Assume your edge is decaying the moment you find it. That mindset keeps you sharp.

Final thoughts

Trading is a game of impermanence. Edges appear, get discovered, and disappear — often faster than we expect.

The traders who survive aren’t the ones who found a “holy grail” system; they’re the ones who accept that edges fade and build a process, often starting within, that evolves faster than the market itself.

Trading is a game of impermanence. Edges appear, get discovered, and disappear — often faster than we expect.

Ignored

Well, yes. I understand your point, and we've already heard several different opinions on this. Some say strategies suddenly stop working, others say they continue to work. It feels like asking my therapists and doctors. Ask 10 and you get 2030 unproven answers. All these "opinions" don't really help me personally to achieve a clearly defined goal that couldn't be formulated more clearly. To be able to live off trading, I need a consistently repeatable minimum income (return) from trading in the range of 2-3% per month with manageable drawdown, and help on how I can best monetize this if I lack the capital. Period.

The only realistic option that seems to be these not exactly trustworthy prop trading firms. I'm really stuck. I only ever hear thousands of opinions, all of which are great, whether from AI or some forum users with a red diamond after their names, but nothing that actually helps me achieve a clear goal. I guess that’s why it’s called a discussion forum. A lot of bla bla, no solutions.

Perhaps I already have a working approach that can achieve what I need, even though some here have said otherwise. I really don't know, but it's the best results I've had in 15 years, and all without spending hours every day analyzing charts for any hocus-pocus patterns or other guesswork. The ORB System as I've been running it for 58 days.

September 21st - September 30th = +5.77%

October 1st - October 31st = +3.91%

November 1st - Today = +6.43%

Maximum drawdown so far: -5.3%

If you have had better results with any approach, or have actually been able to make a sustainable and proven living from trading for at least a few years, please tell me how and with what. Otherwise, I will try again in the next few days to complete a Prop Trading Challenge with the current approach, hoping to gain more capital, which I simply need to make the 5-10k per month from the 2-3%.

"Props" going with biggest, well known is safe. Topstep, Apex, Tradeify...

Follow Montygoldy and you find out what prop is good to trade with and who is in trouble.

Sure some of Red Diamonds are good traders but is more of popularity contest, more subscribers user has better he is.

There are lot of popular "prop youtubers" and who have blown up 1000s of prop evaluation and funded accounts.

It seems your ORB systems work, no point to change and find something else that might work for you.

"Props" going with biggest, well known is safe. Topstep, Apex, Tradeify... Follow Montygoldy and you find out what prop is good to trade with and who is in trouble. Sure some of Red Diamonds are good traders but is more of popularity contest, more subscribers user has better he is. There are lot of popular "prop youtubers" and who have blown up 1000s of prop evaluation and funded accounts. It seems your ORB systems work, no point to change and find something else that might work for you.

Ignored

Yeah. It’s hard to see who can be trusted. Monty is an interesting character but unfortunately I am not that gut feeling trader. Regarding to prop firms, I consider giving it a try with FTMO, Topstep, Tradeify but you hear mixed reviews there all the time. Probably you can only trust your own experience here. I will try a FTMO challenge again, probably directly a 100k this one since my ORB system only works with MT4/MT5 so far and i haven’t yet found a way to transition that to the future space and their own platforms.

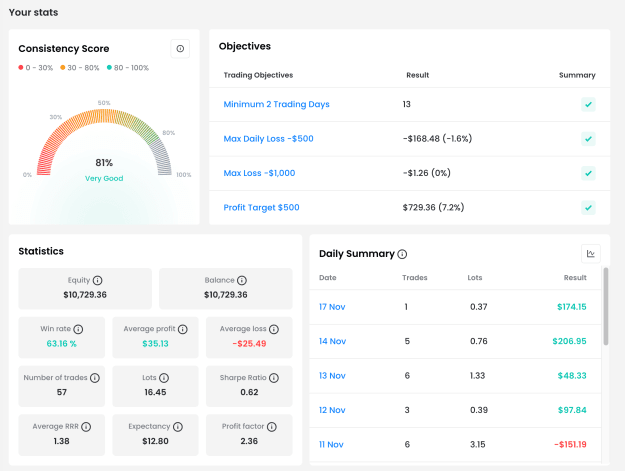

I'm really confused by all the different Sharpe ratio values you get depending on which metrics analysis tools/providers you use. For example, the FF Trade Explorer shows a Sharpe ratio of 4.22 for the account. The MT5 report shows a Sharpe ratio of only 0.18? Darwinex metrics (risk-adjusted) give me a Sharpe ratio of 1.97. They all seem to use different calculation methods.

I'm really confused by all the different Sharpe ratio values you get depending on which metrics analysis tools/providers you use. For example, the FF Trade Explorer shows a Sharpe ratio of 4.22 for the account. The MT5 report shows a Sharpe ratio of only 0.18? Darwinex metrics (risk-adjusted) give me a Sharpe ratio of 1.97. They all seem to use different calculation methods.

Ignored

Maybe you are overthinking ?

Was entry according to plan ?

Was stop and target according to plan ?

{quote} Maybe you are overthinking ? Was entry according to plan ? Was stop and target according to plan ? If yes, then rest is up to market.

Ignored

Yes, absolutely. I also believe that a great profit factor or sharpe ratio should currently play no role for me. Over a period of a few months, it's probably not significant anyway.

Yes, as the current system is automatic, and therefore everything is executed exactly as pre-determined, there are no incorrect decisions. Everything is carried out precisely as determined. I'm increasingly realizing that I cope much better with this than with manually analyzing and trading charts. I've tried that so many times in the past and never achieved nearly the same consistent results as I've had over the last four months, when I've been using automated trading.

I wanted to try out this other automated ORB system for NinjaTrader and thus the futures market. I just subscribed to real-time market data through NinjaTrader. This seems to be necessary to use an unlimited demo account there. My last demo account expired after 14 days. If the system works well, I'll also try a prop trading challenge in the futures market.

{quote} Yes, absolutely. I also believe that a great profit factor or sharpe ratio should currently play no role for me. Over a period of a few months, it's probably not significant anyway.

Ignored

Do you really mean that? You have expressed certain expectations on revenue (your monthly needs etc) and drawdown (a number). Don't you think you need some metric (other than after the fact joy or grief) for knowng that you are on the right track, and that your strategy meets your expectations?

{quote} Do you really mean that? You have expressed certain expectations on revenue (your monthly needs etc) and drawdown (a number). Don't you think you need some metric (other than after the fact joy or grief) for knowng that you are on the right track, and that your strategy meets your expectations?

Ignored

I'm still keeping an eye on it. I just don't know how much weight I can/should give it right now. First, as I said, I'm getting different values displayed everywhere (despite using the same account), and then there's the question of how meaningful these values are over such a short period. Furthermore, people here keep telling me that past results are no guarantee of future results anyway. That makes you wonder why you should even bother testing any strategy at all.

As I mentioned, the most important thing for me right now is a consistent minimum return within a certain maximum drawdown. These are probably the most important metrics I should be keeping an eye on. Currently, things look good, or rather, I'm satisfied with the figures of a compounded return of +17% at -5.3% is over a 3:1 reward/risk ratio.

The account has been running since September 21st.

September 21st - September 30th = +5.77%

October 1st - October 31st = +3.91%

November 1st - Today = +6.43%

With these figures, I would have at least achieved my minimum target of +2%/month for this period. Whether this will remain the case and is perhaps just short-term "luck" remains to be seen. In any case, the DAX has now caught up with the performance of gold too.

XAU/USD: +8.1%, DAX: +7.3%, NAS100: +1.5%

I asked AI:

No, a profit factor from only 3 months of trading results is not a reliable indicator because a short time frame doesn't account for market volatility and different conditions. A high profit factor can be misleading and may be due to luck or a small sample size rather than a consistently profitable strategy. To be more meaningful, a profit factor should be evaluated over a longer period and alongside other metrics like drawdown

No, a Sharpe ratio based on only 3 months of trading results is not meaningful because it lacks statistical significance and can be misleading. A short track record does not provide enough data points to show consistent performance or accurately reflect true risk-adjusted returns across different market conditions.

{quote} the most important thing for me right now is a consistent minimum return within a certain maximum drawdown.

Ignored

So be it, but that expectation has implications and looking at three months of trading data then poses a statistical question: How likely is this trading system to deliver on your expectation?

You would like to know the answer to that question, I believe?

If so, then some sort of statistical analysis would be needed. The ratios (profit factor, Sharpe ratio, etc) give an indication, but that's all. So how will you know the answer to the question?

Only by some calculation. In my experience, Monte Carlo Simulation beats the ratios by far, in particular in situations like this with limited data.

You could simply tell Perplexity Research something like this: I have a profitable day trading strategy with three months of daily returns data. How likely is it to be able to deliver 2% return monthly with a certain target maximum drawdown? Please create a detailed plan for answering that question using Monte Carlo Analysis, including all Python code needed, as well as detailed guidance for interpretation of the results.

Or you could upload the returns data, and ask Perplexity to do the work.

{quote} So be it, but that expectation has implications and looking at three months of trading data then poses a statistical question: How likely is this trading system to deliver on your expectation? You would like to know the answer to that question, I believe? If so, then some sort of statistical analysis would be needed. The ratios (profit factor, Sharpe ratio, etc) give an indication, but that's all. So how will you know the answer to the question? Only by some calculation. In my experience, Monte Carlo Simulation beats the ratios by far, in...

Ignored

Yes, I agree with you. Monte Carlo simulation makes perfect sense. I'll test it tomorrow morning. I also wanted to fix the small RandomEA issue. I noticed that the trailing profit functionality isn't working. I'll also try adding the moving average filter. Maybe that will improve things a bit, let's see.

NinjaTrader is working now. I have now purchased the CME Bundle (Level 1) - Top of Book from NinjaTrader for $12/month and thus at least now have a demo account that does not expire and has real-time market data. They say you need a $50 daily margin to trade MES? Meaning if I deposit $50, that should be enough to open a position with the smallest possible contact size during regular market hours, right?