More like this. Red rectangles are the entries. {image}

Ignored

I understand that it enters when the price re-enters the bands, through the marked box.

I have the ATR by multiplying x 10

And in case of 2nd entry, let MA return to the level of the 2nd to make a 3rd entry?, increasing the lotage in each one, for example: input 1: 0.01 input 2. 0.02 input 3: 0.03...

{quote} I understand that it enters when the price re-enters the bands, through the marked box. I have the ATR by multiplying x 10 And in case of 2nd entry, let MA return to the level of the 2nd to make a 3rd entry?, increasing the lotage in each one, for example: input 1: 0.01 input 2. 0.02 input 3: 0.03...

{quote} If you are adding at all those lines I hope you are staying small, otherwise DD could kill you.

Ignored

It just work in progress, it is interesting concept, but definitely needs optimization and backtesting of at least 500 trades before I even consider going live.

I do like expansions(hello FireScape ) and reversions techniques.

{quote} Feel free to show results with a risk based lot setting instead then. abokwaik and PipMeUp even showed the max gap/spread historically. 1200 pips (2008), need to be able to bleed some money if you scale up. How much are you willing to bleed money wise before you hit that stop button?

Ignored

Well, not like i'll be doing $200 at 0.01 lot if i know that the max DD is $145 from statistics.

If I use $1000 for 0.01 lot then i'll be getting an average of about 7% per year (per pair, i have more figured out =P)

I will then set my equity SL to a max of $200 which is 20% risk.

The probability of hitting this SL is extremely low and has not happened for the last 7years.

And duhh...max gap spread are very different depending on MAs, Period and Timeframe.

Heck why am i even bothering my time here.

I'm gonna delete my previous posts. Not really feel like sharing anything anymore. bye bye

{quote} Well, not like i'll be doing $200 at 0.01 lot if i know that the max DD is $145 from statistics. If I use $1000 for 0.01 lot then i'll be getting an average of about 7% per year (per pair, i have more figured out =P) I will then set my equity SL to a max of $200 which is 20% risk. The probability of hitting this SL is extremely low and has not happened for the last 7years. And duhh...max gap spread are very different depending on MAs, Period and Timeframe. Heck why am i even bothering my time here. ...

{quote} You shouldn't have added until theta ate up nearly all of the original opportunity. I will post about rolling soon to try and get out of rough spots.

Ignored

I have another thought about this strategy. Since there will be a theta loss, why don't we trade it on two timeframes with a straddle to make up the theta loss? It's like "gamma scalping". Two opposite positions still could be managed as always. Nothing's changed but we might have less theta loss. Either leg's profits could cover opposite leg's theta. One thing's different from gamma scalping is that we add positions to deviate from delta neutral. We close a leg and build a new leg to become delta neutral. It's just an idea that needs to be proved in practice. But is it theoretically correct?

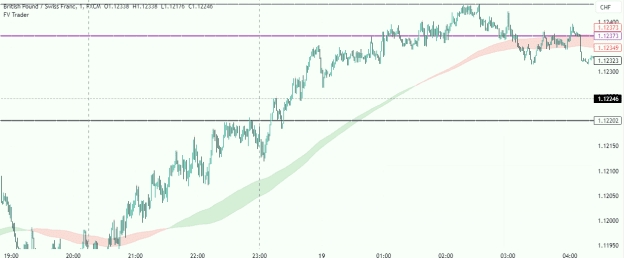

A very hard DD management is when you meet a trend like this. {image}

Ignored

Yep, something that can be misunderstood about this strategy is, it's not supposed to be some 100% win rate martingale type system.

There will be losses. The larger the spread you use to enter, typically results in lower win rates but higher expectancy, which intuitively makes sense because if the spread is larger, there is a higher probability the market is running, or in other words, a higher probability of theta eating your position BUT when it doesn't the payoff is larger.

{quote} Yep, something that can be misunderstood about this strategy is, it's not supposed to be some 100% win rate martingale type system. There will be losses. The larger the spread you use to enter, typically results in lower win rates but higher expectancy, which intuitively makes sense because if the spread is larger, there is a higher probability the market is running, or in other words, a higher probability of theta eating your position BUT when it doesn't the payoff is larger.

Ignored

Easiest way to play this system would be to scan for the maximum average distance from the MA, then trade from there.

{quote} Interesting approach but will result in essentially little to no tradable occurrences so it will be very hard to see the benefits of CLT. Think of the 08 numbers posted earlier by abokwalk. If you are waiting for that distance to be exceeded, you'd have made 0 trades in 15 years...

Ignored

The main issue would be to discover the optimal values of spread and VAR in order to determine the best equity curve - in essence, optimising this strategy. An EA would be best suited for this. I should really get on it lol.

{quote} Easiest way to play this system would be to scan for the maximum average distance from the MA, then trade from there. asw

Ignored

Not exactly

Like in the picture above, the spread is not so high but DD is killing you because price and MA are raising in a parallel way.

This kind of price action will not give you any chance to come up in profit.

So, your money management needs to survive scenarios like that.

Joined May 2021

|

Status: Calculating Probabilities...

|133 Posts

This a long Saturday post to hopefully nudge you so you start changing how you think about trading. How to use a model and profit from errors...

I have written about it many times in the past but never as clearly as I want to lay it out here and it's how to use a model in order to trade.

Many people on Twitter will often post about "entry models" or "smart money" models but can't actually articulate what the model is.

I am not saying they don't work, they might. But what I am saying is, they aren't clearly articulating what they are actually doing with the vague representation of the "model" they are trading. That also goes for nearly every thread of FF.

To keep this post simple, we are going to look at the Black-Scholes model, specifically for pricing European Options.

For those that don't know, a European option is simply a contract saying, after some amount of time, the holder of the contract has the right to purchase some number of shares or units of an asset for an agreed-upon price.

A simple example of this would be a 60-day EUR/USD call option with a strike price of 1.11. Whoever owns this contract has the right to buy EUR/USD at 1.11 after 60 days.

If 60 days pass and EUR/USD is above 1.11, the owner of the contract would be able to buy the shares at 1.11 and instantly show a profit from the difference between the current price of EUR/USD and their execution price of 1.11.

Now that we understand what the option is, and how it works, the most important question to ask is, what is an option like this actually worth?

This is where models come in, particularly the Black-Scholes model.

The purpose of the model is very simple. Given a set of inputs, what would be considered a "fair value" for an option with those parameters.

In this example, the parameters are:

Probability Distribution for EUR/USD: Most economists typically start with a normal distribution.

Risk-Free Rate: This is typically the interest rate difference between the 2 currencies.

Current Price: We will use 1.09 in this post.

Strike Price: As stated above, we will be using 1.11

Duration: In this case, 60 days.

Volatility: This is typically the annual volatility for the pair, but you can really use any period.

Now what the model does is, it takes probability distribution, and modifies it so that it accounts for the risk-free rate. It then calculates all of the possible results of the price of the EUR/USD using this assumed distribution over a 60-day period, using the given volatility.

For all of the possible outcomes where the price of EUR/USD ends higher than 1.11 after sixty days, you take the difference between the final price and the strike price as your payoff.

For all of the outcomes where EUR/USD ends below 1.11, you take 0 as your payoff.

You then average all of these possible payoffs together, discount it by the risk-free rate multiplied by the duration of the option, and just like that, you have a theoretical "fair value" for how much you should sell or buy this option for.

This is also the expected value of the trading activity that would manufacture this option (dynamic hedging).

In other words, if you bought or sold this option a thousand times for this fair price, and all of the model's assumptions remained true, neither the buyer nor the seller would make any money because the price was "fair".

I want you to re-read that last paragraph so it really sinks in. The main idea is, if your model's assumptions (or inputs) are correct, neither you or your counterparty will make or lose any money transacting.

This is where risk and opportunity lie, in the assumption that your model's inputs are correct...

Now in our model above, there is really only 1 main input that is a risk for someone using this model, and it's volatility. We know the current price with a very high degree of certainty, the same goes for the strike price and the duration of the option. We also have a relatively high degree of certainty when it comes to how prices are distributed.

But one thing we do not have a high degree of certainty around is what kind of volatility EUR/USD will realize over the next 60 days. That is anyone's guess...

Knowing this, think again about how we calculate the payoffs using the provided distribution and its assumed volatility.

If volatility is actually higher than what we used in this model, the model's price for the option will be lower than what it is actually worth. This is because the probability of EUR/USD ending above the strike will be increased.

If the volatility is actually lower than what we used in the model, the mode's price for the option will be higher than it's actually worth. This is because the probability of EUR/USD ending above the strike will be decreased.

So even though a call option is inherently a long trade directionally, at the end of the day, it's actually just a volatility bet.

If you are buying the call, you think the price you bought it for was essentially calculated using a volatility input that is lower than what you think the market will realize over the next 60 days. If you didn't think this, you'd be explicitly buying the option for more than it's worth.

If you are selling the call, you think the price you are selling it assumes more volatility in the market than what you think will actually take place. If you didn't think this, you'd be explicitly selling the option for less than it's worth.

In both cases, you are betting on the model being wrong, or the model having an error in regards to the volatility input. If you didn't think the model had an error, there would be no reason to engage in the market at all because every price you transacted would be fair.

This is extremely important to understand. When you trade a model, you are betting on model errors as it relates to the inputs that are most likely to error...

The point of any model is to calculate what some kind of trading activity is worth (its expectancy), in order to price it.

You then need to understand which inputs into the model are most likely to be wrong, and in which direction they will be wrong. You then need to understand how these errors impact the expectancy of the model, and this is what you actually should be trading.

The opportunities are in the errors.

Everyone trading is doing this whether they formally recognize it or not. The problem is, they are betting on the wrong input for the model they don't even know they are using and this is why they consistently lose.

Most retail traders are assuming the price will be more skewed in one direction or another if they use a certain entry signal, which is why they are either going long or short in a pair.

So in their model, whether they recognize it or not, they are betting that the expectancy of a fair market, which is essentially transaction costs, is wrong because the market is going to go up or down via skew. They think it's higher than that using their entry signals.

But in reality, you can assume with a high degree of certainty that the skew of the pair's distribution is essential right at or near 0 overtime.

So if you are betting that the skew of the distribution will be well above or below 0 consistently over time using your entry signal, you will never make any money because that input is one of the least likely to error in the model they don't even realize they are using...

There is also a bit of a fallacy in this line of thought because, if there was some signal that if used would consistently result in the skew being significantly positive or negative, you wouldn't need the signal because the "edge" would be built into the distribution itself.

Thinking about trading MA crosses on SPY over the last 100 years... It's not the MA crosses creating positive expectancy for "trend-traders", it's the distribution itself. This is why timing SPY almost always will perform worse than buying and holding it. By timing it, you are actually handicapping the one thing that is driving your expectancy, the distribution itself.

I think what really could skew distribution or shift fair value are news and sentiment. Some old stats indicates that market only trends 20% of the time. In other words, most of the time fair value doesn't move much. So, 80% of the time trader should fade the extreme moves (model errors) and follow it when fair value is shifting. A trader once taught me "worry about your forecast first rather than your entry" which is opposed to what most retail traders do.

I think what really could skew distribution or shift fair value are news and sentiment. Some old stats indicates that market only trends 20% of the time. In other words, most of the time fair value doesn't move much. So, 80% of the time trader should fade the extreme moves (model errors) and follow it when fair value is shifting. A trader once taught me "worry about your forecast first rather than your entry" which is opposed to what most retail traders do.

Ignored

I have heard the 80/20 rule as well and have always found it interesting.

for me though, I have always found it hard to determine what is a trend and what’s just a tail move in a distribution with no skew? Hard to tell the difference, at least for me.

the skew is like the sample paths, in that even when it’s perfectly fair, it doesn’t mean that the paths are likely to have 0 skew it just means 1/2 of them have positive skew and 1/2 have negative skew.

Thanks for sharing, I'm new to Forex Factory and delighted to have found a community with so much helpful and valuable information and support. I've been trading for about a year and I think I've followed a pretty typical journey so far, initial low cost disasters, learned fast and improved a lot (or so I thought), enjoyed some amazing success, became overconfident, more much higher cost disasters, now cautious, treading carefully and determined.

I hope it's Ok that I refer all the way back to the chart you posted on Aug 14. I'm able to replicate that almost perfectly, but I can see your RSI settings provide much greater clarity than I can see with the TV default settings. Do you mind sharing the changes you made to create the less noisy graph as shown on your screenshot?

Thanks.

{quote} I have heard the 80/20 rule as well and have always found it interesting. for me though, I have always found it hard to determine what is a trend and what’s just a tail move in a distribution with no skew? Hard to tell the difference, at least for me. the skew is like the sample paths, in that even when it’s perfectly fair, it doesn’t mean that the paths are likely to have 0 skew it just means 1/2 of them have positive skew and 1/2 have negative skew.

Ignored

That's very hard to tell. For me, multiple timeframes analysis is analyzing a distribution within a distribution. A tail move with a skew must be a move that moves away from lower timeframe's distribution and affect higher timeframe's. If higher timeframe accepts the move, then it's not just a tail with no skew. The distribution is developing to left/right. And vice versa, if the higher timeframe rejects it, lower timeframe is a noise and it's time to profit from this model error like you said. When timeframes sync, the sentiment is strong and that's when big trends happen. But it's very exhausting to watch this in real time. What usually happens is m15 align with m5 and there's a opportunity on m1 but h1 is blocking on the way.

This a long Saturday post to hopefully nudge you so you start changing how you think about trading. How to use a model and profit from errors... I have written about it many times in the past but never as clearly as I want to lay it out here and it's how to use a model in order to trade. Many people on Twitter will often post about "entry models" or "smart money" models but can't actually articulate what the model is. I am not saying they don't work, they might. But what I am saying is, they aren't clearly articulating what they are actually doing...

Ignored

@RisKcuit

Thanks for your long post where the content is about option theory.

How do you translate that into normal forex trading and the discusions we were having since last week?