Then do yourself a favour by registering for agea.com's streamster platform, and locate a username by the name Joshfx96. Follow his postings. You will understand my point.

Why do people not realize that if trend-like patterns can be generated by a random walk, the inverse is nót necessarily true.. With enough iterations (or with a bit of luck) I could reproduce a particular mathematical function, let's say y=x^2, on an arbitrary domain with arbitrary step sizes in x. Does that mean that y=x^2 is random? No. The same holds for forex trends: of course I can iterate a random walk creator a couple of times, stumbling upon a pattern that looks like one typically observed in forex price charts, and consequently I claim to have "proven" forex to be fully random?

The number of variables and the velocity of their changing values does not allow any individual, even those equipped with super fast quantum computers, to write an algorithm that predicts unerringly future prices.If we cannot find hard evidence that forex prices are predictable (not a random walk ) than we must , by default ,rely on circumstantial evidence. In this area the evidence , although not "hard ", is abundant. One merely has to go to the trades page on this very website and view the records of highly successful traders. The chances of their trades being the result of random entries and exits to the market is nil. Long term profitable traders, by the very fact of their existence at all , is the only evidence we need to prove that markets are not random, but rather a consequence of price actions that have preceded them.

of course I can iterate a random walk creator a couple of times, stumbling upon a pattern that looks like one typically observed in forex price charts, and consequently I claim to have "proven" forex to be fully random?

Ignored

Of course not - but that wasn't the point here. The question is: Can you prove that the markets are not random at all?! I think we shouldn't discuss if the one or the other is true because we can't prove it. And as neither the one nor the other can be proved, I stick to the worst case scenario (for me the more probable scenario) that markets behave random most of the time. If we can beat randomness, we should be able to trade successfully, too. It may be worthless to prove the market's randomness by generating random patterns fitting the market (which wasn't my point at all - I've just showed it in order to show that trends can be generated by random data, too) - but it is also worthless to claim the opposite without any proof.

{quote} Then do yourself a favour by registering for agea.com's streamster platform, and locate a username by the name Joshfx96. Follow his postings. You will understand my point.

Ignored

I tried to register on that website but everytime I tried website gave me errors. Could you help me?

{quote} Of course not - but that wasn't the point here. The question is: Can you prove that the markets are not random at all?! I think we shouldn't discuss if the one or the other is true because we can't prove it. And as neither the one nor the other can be proved, I stick to the worst case scenario (for me the more probable scenario) that markets behave random most of the time. If we can beat randomness, we should be able to trade successfully, too. It may be worthless to prove the market's randomness by generating random patterns fitting the...

Ignored

i can say to you that market is not random. if i can pinpoint the market top when it's in a strong bullish trend or market bottom at the strong bearish trend, do you think it's random ? You should read more book and get more knowledge instead need others to prove to you.

=== How does an AVERAGE CANDLESTICK look like? ===

Have you ever asked how an average candlestick does look like? How is the "normal" ratio of the upper or lower wicks to the candle's range? Is it like 10 % wicks on both sides (on average)? Or 40 %?

Since the former discussion was more or less about the randomness of the markets (which wasn't my original intention of my 2nd post), I'd like to show how you may arrive a conclusion in regards to the average candlestick structure. I think the morphology of candlesticks may be explained by random walks ...

It all starts with a one-dimensional Gaussian random walk that we want to consider ... This random walk starts at an arbitrarily chosen origin, the open prize of your candlestick. Now prize can go either up or down, whereas the probability of the increments (the number of ticks the prize changes) is determined by a normal distribution. We let the experiment run for 1 minutes, 5 minutes, 1 hour, 1 day, or whatever time interval your candlestick should represent. After one run we repeat the experiment again and again and again ... After (let's say 10,000) repetitions we can calculate the proportion of the upper and lower wick for each and every run, and we can calculate the average proportion.

Fortunately, we don't even have to model it. Stochastics gives us two important formula:

The average walking distance reached after N steps i calculated as sqrt(2 * N/pi).

The expected maximal distance reached in a walk with N steps is calculated as sqrt(N * pi/2).

We could chose any value for N to solve both formulas or we can set N = 1. Then we derive sqrt(2/pi) and sqrt(pi/2).

Now let's assume that our random walk ends above our starting point (the candlestick is a bullish candlestick). Thus, we would expect the close prize to be sqrt(2/p) above the open:

open = 0

close = sqrt(2/pi) = 0.7978846

In this case the expected maximal distance reached in our random walk represents the high prize,

high = sqrt(pi/2) = 1.253314

Now we only need to calculate the expected average low. It can be derived by subtracting the high prize from the close value (assuming that instead of a bullish candle starting at the open we see a bearish candlestick starting with the close of the bullish candlestick):

low = close - high = -0.4554294

With these numbers you can calculate the expected average candlestick ratios, i.e.

wicks/total candlestick range = 0.4554294/1.708743 = 0.2665289

body/total candlestick range = 0.7978846/1.708743 = 0.4669424

Thus, the ratio we may expect to see on average is close to 1/4 : 1/2 : 1/4.

Now you may think "so what, this is just fucking theory!" Yes, it is. However, the true mean proportions of the wicks and the body are very close to the numbers we calculated above. You can compare the numbers given here with the empirical values calculated elsewhere by jimsterk.

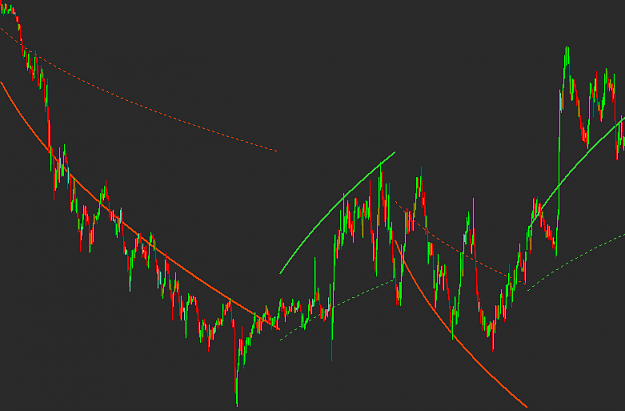

But remember - these are just the numbers you will see if you calculate the mean over a big number of candles. If you just look at a small sample the numbers can deviate much. But what does the deviation of a current candlesticks form may tell you about the strength of bulls and bears during the lifetime of that candlestick? Maybe you could use this info in order to determine if a trend that you see is stronger than you would expect it on average (cf. image below). Just more food for thoughts ...

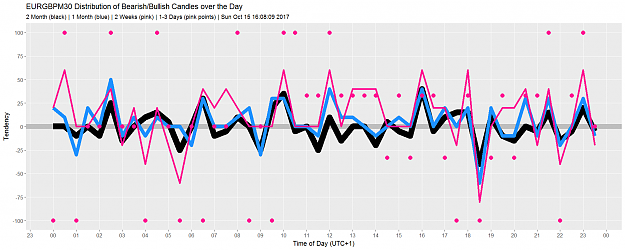

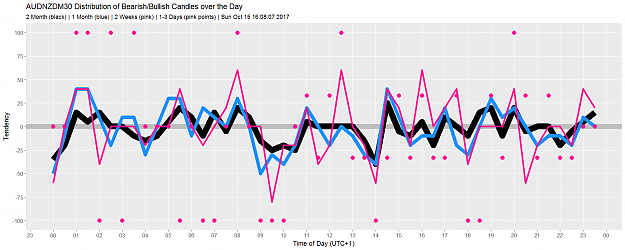

To the question if markets are random or not another view: Some times ago I did some research (with R), regarding the question if currency pairs form patterns in their up and down over the day. Yes they do, at least sometimes. Patterns appear, get stronger and disappear. Sample (see picture): EURGBP has a strong tendency to go down at 18:00, the pattern exists since 2 month and got stronger in the last month, and is very strong in the last 2 weeks and the last 3 days.

To the question if markets are random or not another view: Some times ago I did some research (with R), regarding the question if currency pairs form patterns in their up and down over the day. Yes they do, at least sometimes. Patterns appear, get stronger and disappear. Sample (see picture): EURGBP has a strong tendency to go down at 18:00, the pattern exists since 2 month and got stronger in the last month, and is very strong in the last 2 weeks and the last 3 days. {image} {image}

=== The myth of risk:reward ratios === I guess everybody who starts studying the markets may have heard one platitude: "Only open trades with high rewards and low risks!" What does it mean? It means that you should only enter a trade where your predefined prize target is more distant to your entry than your exit level. Sounds great, doesn't it? I mean, you will always win more than you lose. Not bad?! Hell no! Let's analyze it. Although this may be not the full truth, let's consider that the market is random, i.e. you have no idea on where/when...

Ignored

All this is based on the hypothesis that market is random.......but it is not

Admittedly you do not have a background in Statistics, but this is basic Statistics. In order to create a probability, or odds, you need an average.

Ignored

To be honest, I'm working as a stats teacher at the university. And thus I can't agree with all your points. For instance, you don't need an average to calculate probabilities. There are even distributions that don't have a mean (an average) per se ... But yes, all my points were challenging (and don't need to be true in all cases) in order to proceed a discussion. And as such I enjoy your point of view. Thanks!

All this is based on the hypothesis that market is random.......but it is not

Ignored

Yes, maybe. I wrote in my 2nd post "Is it only possible with an edge that shifts the winning probability in our favor?". Doesn't it imply that I agree that the market doesn't have to be pseudo-random all the time? I would be very happy if you or any other readers would give some indications/proofs/facts on why the market isn't random. If you claim that it isn't random means that you should be able to predict it with a probability > 50 % (at least partly - but then it is pseudo-random again). I'd like to see an experiment/setup where the outcome of your predictions is mostly positive. (And no, I don't doubt that you're a successful trader!)

{quote} You most certainly do need an average, LOL. You sure you teach this? You just said you didn't know anything about it and now you are a teacher and don't know that probability is the average of averages? You might want to delete that post.

Ignored

Yes, I am. Where have I said that I don't know anything about it? And where is the contradiction? There are strategies that work if the market is random and that won't work if it is deterministic and vice versa. I said the market can be random and partly deterministic at the same time (pseudo-random). Don't get why you attack me ... I just showed my point of view and asked in a polite way if someone can show some proofs/evidences that the market is not random. I haven't seen one so far - I've only seen statements without indications.

You sure you teach this? You just said you didn't know anything about it and now you are a teacher and don't know that probability is the average of averages?

Ignored

This is only partly true and NOT for all distributions. For instance, the Cauchy distribution doesn't have a mean (average), the Poisson distribution doesn't have a mean or standard deviation (yes, it has either a mean or a standard deviation). And yet you can calculate probabilities for these distributions. And no mean is involved.

{quote} With random I mean that nobody can really predict the future prize path with 100 % accuracy because nobody knows the intentions of all market's participants.

Ignored

That is precisely why we should always go for high RRR.

Joined Aug 2010

|

Status: Stare Into the Lights My Pretties!

|795 Posts

First of all, there are different types of randomness. https://en.wikipedia.org/wiki/Seven_..._of_randomness

The worst kind is pure randomness (or extreme randomness with complete lack of repeatable patterns). And the markets definitely do not fall into this category.

The markets are a mix of mild random and nonrandom elements. But the random element are not really random. They are simply unknowns in a very complex equation. Trying to solve this equation for the purposes to find the unknowns is a waste of time.

Instead, you have to focus on the known nonrandom and repeatable elements. See if you can stitch together a consistent strategy with stable outcomes.

You don't need any indicators if you approach the market with automated algo systems. But some indicators can be very useful for discretionary trading because they give you stable reference points and help you to spot some repeatable patterns which may be hard to see on naked chart.

But at the lowest level ALL information is encrypted in the price. With enough effort you can decrypt this info using pure math and you can find some very nice but very subtle patterns which are completely hidden for 99,9% of the traders. Only a small number of quant traders know about them.

Here is one of the people and pioneers in the field who knows what is up.

The forex markets are not random, if they were random, there wouldn't be any participants, if it was random it could well just open the EURUSD at 100.5678 tomorrow morning, and if it did that, no one would be trading, just like the Venezuelan Boliviar.

The forex markets are not about statistics, forex is about business and it's participants, I'm not saying that statistics aren't applicable, but it can't be the main focus.

The forex markets are not about fundamentals either, although they do play their part.

{quote} Yes, maybe. I wrote in my 2nd post "Is it only possible with an edge that shifts the winning probability in our favor?". Doesn't it imply that I agree that the market doesn't have to be pseudo-random all the time? I would be very happy if you or any other readers would give some indications/proofs/facts on why the market isn't random. If you claim that it isn't random means that you should be able to predict it with a probability > 50 % (at least partly - but then it is pseudo-random again). I'd like to see an experiment/setup where the...

Ignored

The problem is not in the lack of an edge........mostly the problem is in the trader who fails to exploit an edge

To me SL is like giving yourself a light fine for entering a stupid trade (it didn't look stupid at the time) instead of getting a hefty fine later.

The problem is, how many light fines are you going to give yourself before you make a good trade with a decent profit? Also, your next profitable trade is that profit minus the light fines you have been giving yourself.

If you have mastered the art of smacking your own bottom every time you make a bad trade, then go for it otherwise maybe just look into other ways to make a buck that doesn't involve a self inflicted smack to yourself.