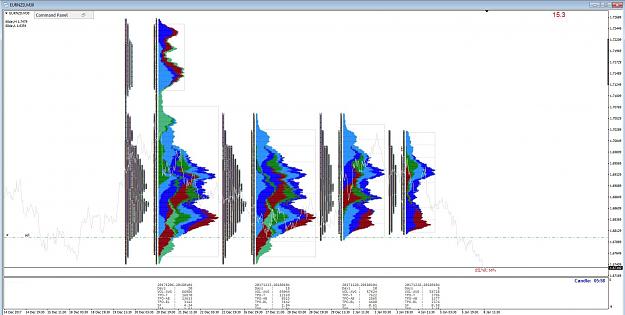

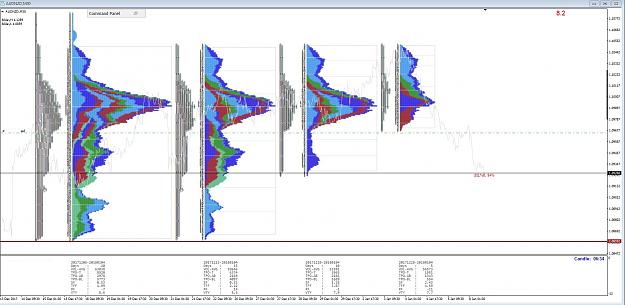

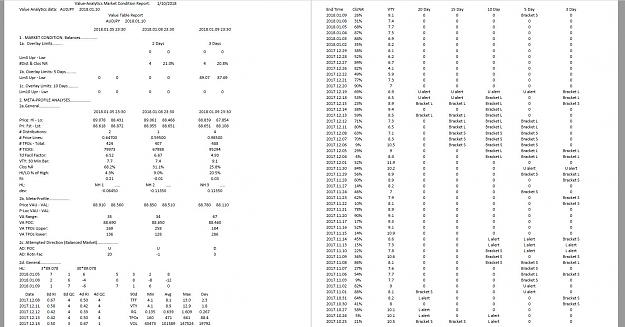

Markets are not efficient, rather they are effective - Jones

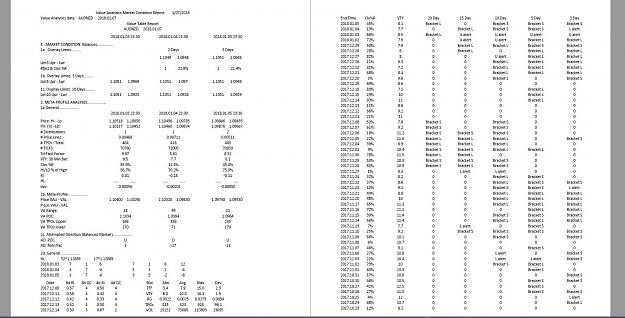

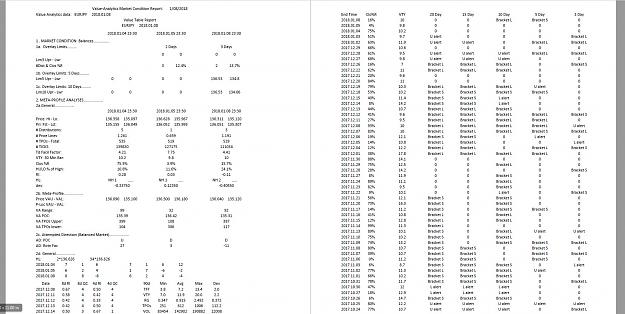

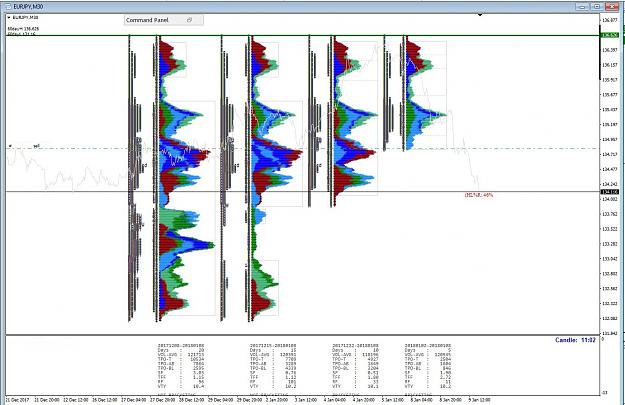

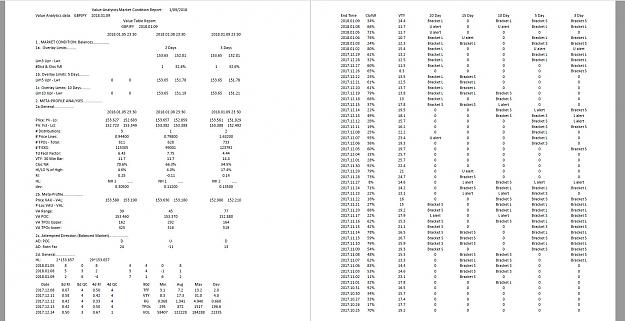

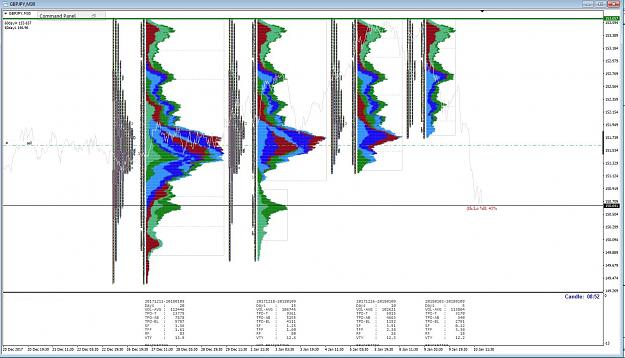

Auction Market Value Theory & Analytics

Auction Market Value Theory & Analytics

- #1,281

- Edited 12:37pm Jan 4, 2018 12:26pm | Edited 12:37pm

- Joined May 2009 | Status: Trader | 1,879 Posts

- #1,282

- Jan 4, 2018 11:31pm Jan 4, 2018 11:31pm

- Joined May 2009 | Status: Trader | 1,879 Posts

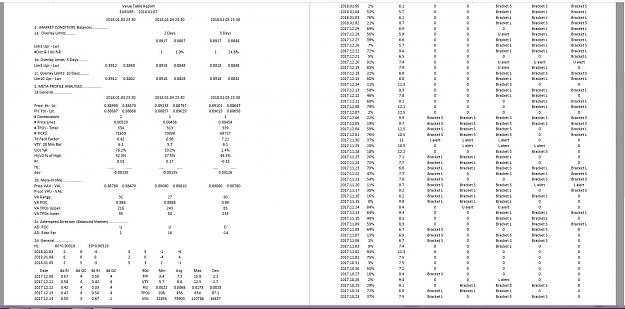

Markets are not efficient, rather they are effective - Jones

- #1,285

- Edited 5:17pm Jan 5, 2018 11:28am | Edited 5:17pm

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,287

- Edited Jan 8, 2018 10:04am Jan 7, 2018 10:00pm | Edited Jan 8, 2018 10:04am

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,288

- Jan 8, 2018 10:03am Jan 8, 2018 10:03am

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,289

- Jan 9, 2018 2:16am Jan 9, 2018 2:16am

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,290

- Jan 9, 2018 10:06am Jan 9, 2018 10:06am

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,292

- Edited 3:02pm Jan 9, 2018 2:43pm | Edited 3:02pm

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,293

- Jan 10, 2018 9:04am Jan 10, 2018 9:04am

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,295

- Jan 10, 2018 10:26am Jan 10, 2018 10:26am

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,296

- Jan 11, 2018 10:41am Jan 11, 2018 10:41am

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,297

- Edited 3:30pm Jan 11, 2018 2:43pm | Edited 3:30pm

- Joined Feb 2011 | Status: Trader | 1,405 Posts

- #1,298

- Jan 11, 2018 4:04pm Jan 11, 2018 4:04pm

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones

- #1,300

- Edited Jan 12, 2018 12:45am Jan 11, 2018 9:29pm | Edited Jan 12, 2018 12:45am

- Joined May 2009 | Status: Trader | 1,879 Posts

Markets are not efficient, rather they are effective - Jones