""One win and three losses for sell in May and go away."" The reason for three loses is that he is not combing the calendar with other system.

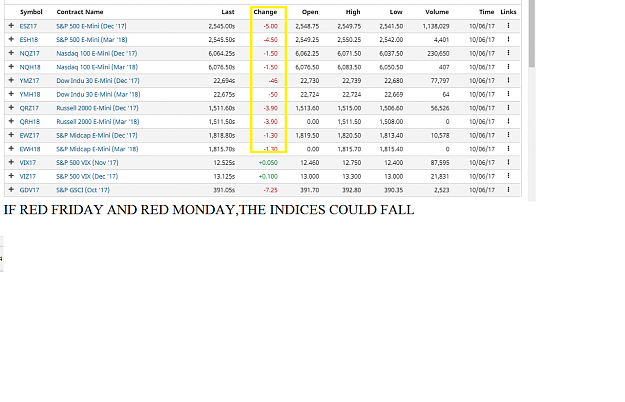

IF RED FRIDAY AND RED MONDAY,THE INDICES COULD FALL

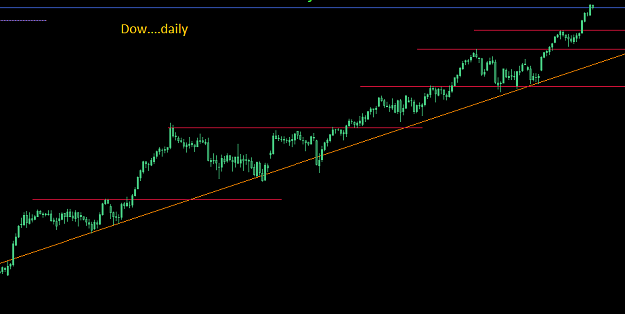

The U.S. stock market has been in a seemingly endless uptrend, and there is reason to think that won’t end anytime soon, as the next big trading catalyst should be a positive one for equity markets.

The third-quarter earnings season is scheduled to ramp up over the coming weeks, and some major investment banks say the market, despite trading near all-time highs, hasn’t priced in how good results could be relative to current forecasts.

According to FactSet, earnings for S&P 500 SPX, -0.18% companies are seen coming in at $32.34 a share in the third quarter, which represents growth of 2.81% from a year ago. Sales are seen rising 4.79% compared with the third quarter of 2016.

Morgan Stanley said the consensus forecast for earnings was “too low.” While results in the quarter could be impacted by Harvey and Irma—two recent hurricanes which contributed to the labor market’s first monthly job losses in seven years—that factor won’t be enough to meaningfully limit profits.

“A mix of conservative guidance and a strong [first half of the year], continued economic growth, and positive incremental margins set the quarter up for an easy beat,” the investment bank wrote in a note to clients. “We think companies will once again deliver versus consensus expectations.”

Morgan Stanley sees the earnings season as having a mixed impact on stocks, which have hit dozens of records throughout 2017. The firm forecast a market consolidation—“a sell the news event”—during the season, but added that the S&P 500 could then “make its next surge” toward 2,700, the bank’s first-quarter 2018 target for the benchmark.

The S&P 500 is about 6% below that target at current levels. In recent quarters, the firm pointed out, the S&P 500 has rallied going into earnings as investors decide estimates are too low. A “sell the news” event is when markets decline when assumed news, the expectations of which the market had risen on, proves to be validated and investors cash in on their bets.

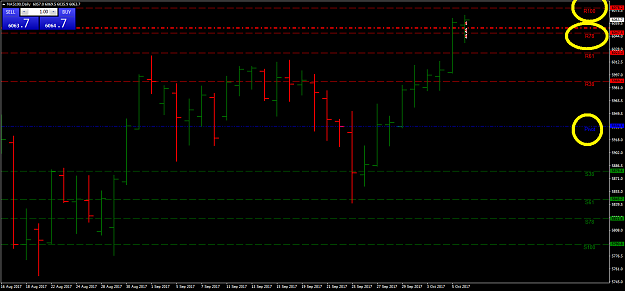

TimeS&P 500 IndexFeb 17Mar 17Apr 17May 17Jun 17Jul 17Aug 17Sep 17Oct 17 US:SPX 2,2002,3002,4002,5002,600

J.P. Morgan Chase & Co. was similarly bullish on the coming season, indicating that the overall earnings per share growth rate could be more than three times that of current consensus expectations. “Most of the activity variables we follow suggest EPS growth rate of 10% or more should be achievable in Q3,” it wrote, referring to earnings per share. “Economic activity was robust during [the third quarter], with strong global PMI prints, U.S. [Citigroup Economic Surprise Index] moving above zero, and ISM reaching the highest levels since 2004.”

Such results would be “reassuring” for investors, J.P. Morgan said, and “one of the positive catalysts that will drive the equity rally into the year-end.”

Other firms were more tepid about what earnings would say about the economy, and the impact they could have on the market. Goldman Sachs noted that estimates for the quarter have been dropping, albeit by a smaller degree than is typical, and that third-quarter growth would represent a deceleration from the first and second quarters of the year, when profits rose by double digits.

Profit expectations have dropped 4.2% since the end of June, when earnings were seen coming in at $33.76 a share, according to FactSet. The S&P 500 has risen 5.1% over that same period.

“Given the low bar for 3Q earnings and solid economic data, we expect the average EPS surprise will be modestly positive, but smaller than the beats in” the first half of 2017, Goldman Sachs analysts wrote. David Kostin, the chief U.S. equity strategist, added that enthusiasm over the prospects for tax reform, would trump the deceleration in earnings as a market driver.

MORE than half of American households have less than one month of income available in readily accessible savings to use in case of an emergency, a new report from the Pew Charitable Trusts finds.

Many financial advisers recommend that families have a savings account holding three to six months’ income, in case of a job loss or an unexpected major expense. But regardless of income level, the report found, most Americans lack the recommended level of savings.

Even if they tapped all available resources, including assets that can be costly to tap, like retirement accounts and investments, the typical middle-income family can replace just four months of income, the report found.

The report, “The Precarious State of Family Balance Sheets,” found that even though the economy has recovered from the Great Recession, many households remain financially insecure. Most families, the report said, “feel vulnerable and stressed, and could not withstand a serious financial emergency.”

The position of lower-income households is particularly precarious, the report found, with less than two weeks’ income available in their savings and checking accounts and cash on hand. Such families generally have less access to credit than higher earners, so have fewer options during a financial crisis.

The report drew from a variety of economic data sources, including surveys from the United States Census Bureau and the University of Michigan.

Slower income growth in the last decade may have contributed to inadequate savings levels, researchers said. But some trends described in the report, they said, aren’t new. For instance, the report found substantial fluctuation in family income is the norm; in any given two-year period, nearly half of households experience a change in income of more than 25 percent — whether up or down. Such volatility, which has been fairly constant since 1979, “likely contributes to families’ inability to build a financial cushion,” said Erin Currier, director of Pew’s financial security and mobility project, in a call discussing the findings with reporters.

The report and additional research that is underway are aimed at achieving a broader understanding of household finances that will help policy makers create programs that promote “asset accumulation.”

Personal financial experts say there are ways to build savings, even with limited income. “The hardest part is the psychological side,” said Daniel Boylan, an instructor of finance at Ball State University in Muncie, Ind. “The idea of saving six months of income sounds impossible.”

Mr. Boylan advises setting an initial goal of one month’s pay, then moving on to two months’ after the first goal is attained, then three months’, and so on. “Take it one step at a time,” he said.

J. Michael Collins, director of the Center for Financial Security at the University of Wisconsin-Madison, advises automating savings by having a fixed amount — even if it’s a very small amount — regularly transferred from your checking account to a savings account. “If it’s up to you to decide every month if you want to do it and how much,” he said, “it won’t happen.”

Jonathan Morduch, a professor of public policy and economics at New York University who has studied the financial habits of low- and moderate-income families, said even lower-income families saved, but they tended to put aside money for specific items they knew they would need in the next two to three months — say, back-to-school clothes or holiday gifts — rather than building reserves for an emergency that may or may not happen.

For some people, getting started is the biggest hurdle. Christina Mele, 50, who works for a temp agency in Virginia Beach, Va., said she had never had a savings account until she started saving for an emergency fund last year, after enrolling in the Bank On education program sponsored by the City of Virginia Beach, local banks and community groups.

She set up a savings account at a credit union and has 5 percent of her paycheck automatically deposited to the account. She declined an A.T.M. card so that she couldn’t easily get to the money. She has saved $600 toward her goal of $1,000. “If you have to physically walk into a branch to withdraw the money,” she said, “you’ll think twice.”

Here are some questions about building emergency savings:

■Where should emergency savings be kept?

An emergency savings account should be accessible — since the point is to be able to get the money quickly if you need it — but not too accessible. Using a bank separate from where you have a checking account helps. Enlisting a trusted friend or family member as a “money guard” can help you stay on track.

Mr. Morduch said one young man he encountered in his research was trying to save for a deposit to get his own apartment, so he gave his cash to his mother to keep in her account, even though he had his own savings account.

■It’s tax season, so what about saving my income tax refund?

Putting at least part of a tax refund, or a bonus, into a savings account can be a relatively painless way to start an emergency fund, Mr. Morduch noted. The Internal Revenue Service lets taxpayers split their refund for direct deposit into as many as three different accounts; to do so, you’ll need to file Form 8888 with your return.

■Are there tools available that can help promote savings?

The America Saves campaign encourages consumers to sign a pledge, which helps them make a commitment to save, and to sign up on its website to receive texts with savings reminders and tips.

Morgan Stanley sees the earnings season as having a mixed impact on stocks, which have hit dozens of records throughout 2017. The firm forecast a market consolidation—“a sell the news event”—during the season, but added that the S&P 500 could then “make its next surge” toward 2,700, the bank’s first-quarter 2018 target for the benchmark.

Hello alicia, how are you? You are trading some different systems. What do you think it's the best? I've just started on stocks this week. What do you think about ichimoku? Best regards

Ignored

The all time best system for all markets is the turtle system.

i m just creating and testing ideas.but the turtle system has been arround for ever and still is used by top traders.

How could the Turtles possibly know the balance sheets and assorted other financial metrics of all five hundred companies in the S&P 500 index? Or how could they know all the fundamentals about soybeans? They couldn’t. Even if they did, that knowledge would not have told them when to buy or sell along with how much to buy or sell. Dennis knew he had problems if watching TV allowed people to predict what would happen tomorrow—or predict anything for that matter. He said, “If the universe is structured like that, I’m in trouble.”

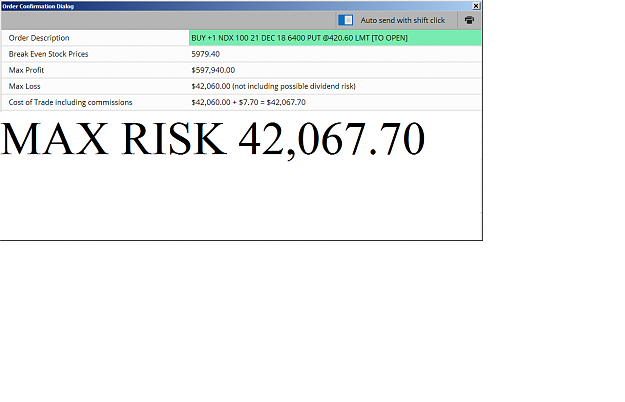

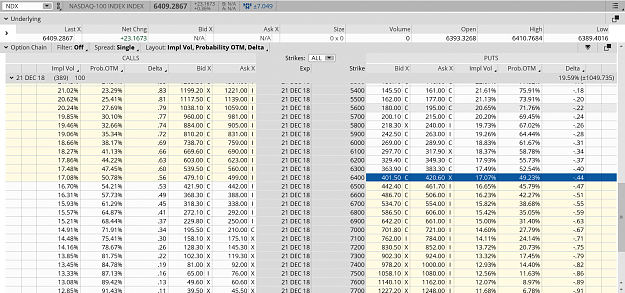

DEMO to pratice options vs forex.

Risking 50 k per trades i can kill my account in just 1 day when trading forex, but if i trade LEAPS i have over 9 months to be wrong.

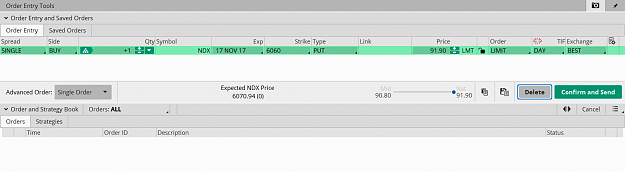

reason for the trade :I think that the stock market is due for a significant correction