DislikedAfter a full day of sitting in front of the monitor coding and debugging here is something different to look at. I managed to download historical real tick data from internet and feed this data to our beloved the volume profiler tool. Now I could use the real tick volume instead of estimating. Huge expectancy right? Well here are the results, not much of a difference if you ask me. And the phenomenon about the jaggedness of the tick volume profile: It took me sometime to realize this. It looks like people (or systems) still prefer to trade at 4...Ignored

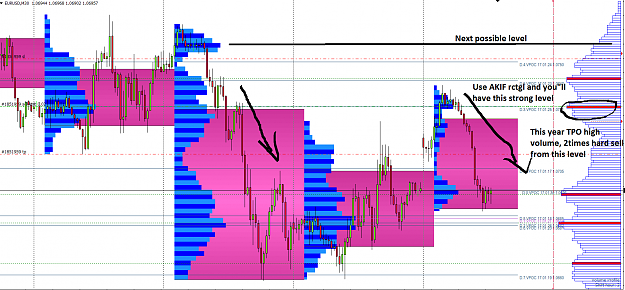

great work anyway, ;-). Even if to be SURE only, that the impact is not that big. However, looking at the charts you provided, there seems to be some significant difference between your estimated data (if that is your "Estimated M1 Volume") and the real feed (Bid/Ask). It's not at the VPOC, but at the other HVN, LVN (high volume, low volume nodes). Or do I understand something wrong here??

Also thanks for the clarification of the smoothness/jaggedness. I was (also) wondering all the time...