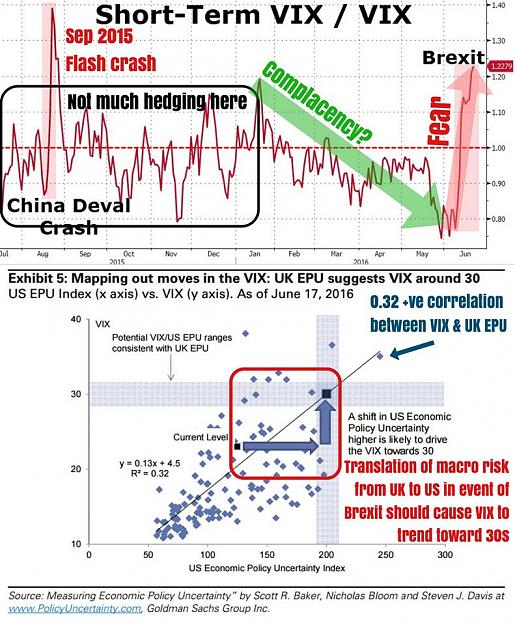

How are markets reacting to the apparent Brexit event risk which will climax in less than 2 days? Well, massive hedging at the front end of the VIX, inverting the front end of the VIX curve to the most it has been since the global stock market flash crash in August 2015.

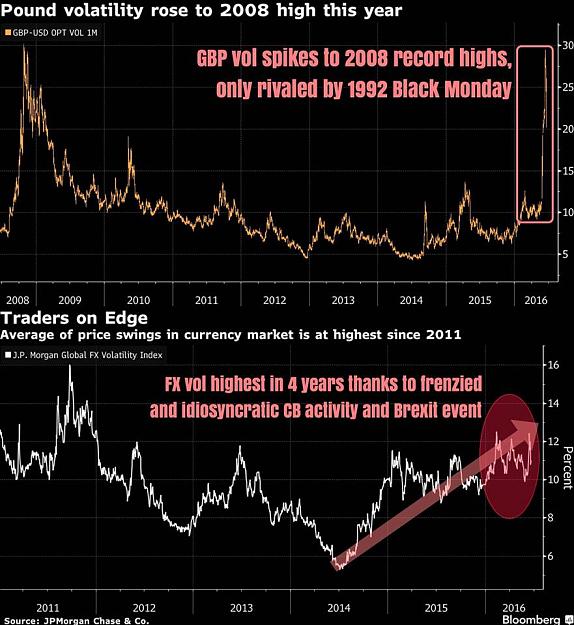

Months of complacency beginning in February (expressed by the steepening of the curve with ultra short-term vol trading below spot) has bred great fear and anxiousness when Brexit fears started to surface and everyone who wasn't hedged started to bid for short-term protection at ever higher premiums each day, leading to an inverted VIX curve at the front end and vol premiums to spike to crisis levels.

***

With U.S. Economic Policy Uncertainty (EPU) at current highs (see bottom pane), in the case of Brexit the U.S. EPU may rise substantially higher, pulling the VIX higher as well.

Goldman Sachs has more on the UK-US macro discrepancy and how that might affect the VIX:

"The VIX may reach the high 20’s to low 30’s if US EPU spikes. After languishing in the low teens over the past several months, last week the VIX broke through 20 for the first time since March. Given that the spread between the US and UK EPU indices is near an all-time high, in the case of a leave decision, it stands to reason that US policy uncertainty could be pulled higher. A simple back-of-the envelope calculation suggests that the current level of the UK EPU Index is consistent with an increase of 80 or so points in US EPU. Tying this back to the VIX, we arrive at VIX levels in the high 20s to low 30s."

***

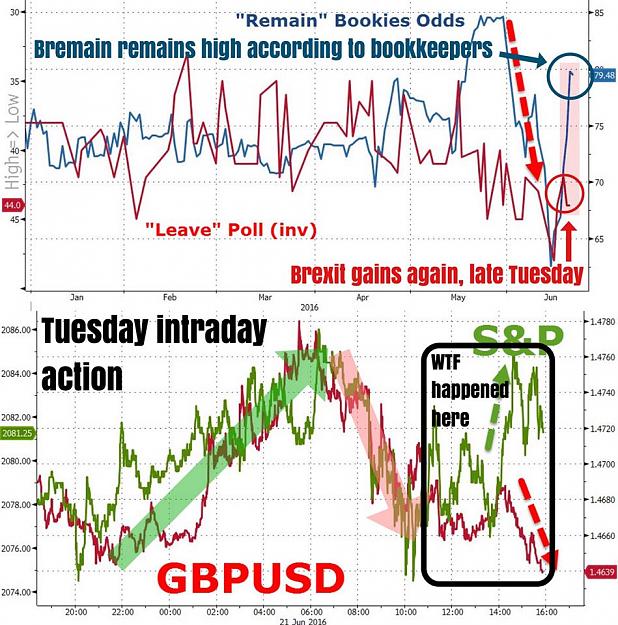

Here's how analysts and banks see markets trade should Brexit be voted for, courtesy of Bloomberg:

Morgan Stanley

* Base-case index target for the FTSE 100 in case of ‘leave’ is range of 5000-5300; for the Euro Stoxx 50 is 2400-2550

BofAML

* Sees European stocks moving 10% either way after Brexit vote; “leave” result would be risk-off event not just in U.K. but also Europe and, to a lesser extent, globally

* Sell-off in Europe could translate into 6%-7% drop for S&P 500

* “Unquantifiable risk” whether other EU countries would then attempt to leave EU

* Long European low-risk dividend stocks, long SXDP index vs short SX3P index, long European index dividend futures, long MSCI EM

Goldman Sachs

* On average, the ERP (equity risk premium) has risen by ~150bps in past risk-off events. If Brexit were to result in similar scenario, rise in ERP of 150bps from end-May levels would push Stoxx 600 down to 280 and Euro Stoxx 50 to 2400

* Cleanest expression of Brexit risk is in U.K. domestic stocks (GSSTUKDE) and especially those with high sensitivity to investment spending

JPMorgan

* In ’leave’ scenario, euro-area equities would likely underperform U.K. ones, whose relative performance would be helped by GBP weakness

* Stays overweight on U.K. equities, which trade “outright cheap” on P/B metric

Citi

* Given recent equity weakness, likely policy reaction, new oil price regime, base-case Brexit downside risk is ~5%; at extreme end of the outcome spectrum, European stocks could fall 10-20%

* FX weakness, especially in U.K., is a key offset and should, in time, support positive U.K. returns, excluding return of full-blown systemic risk

Deutsche Bank

* Sees 10% downside for European equities

* Overweight FTSE, underweight DAX: if Brexit, U.K. equities would outperform European stocks, given likely GBP depreciation as well as U.K. market’s defensive sector structure

Jefferies

* Sees 5%-10% decline in FTSE banks, euro-zone banks falling by at least an equivalent, if not greater percentage

Months of complacency beginning in February (expressed by the steepening of the curve with ultra short-term vol trading below spot) has bred great fear and anxiousness when Brexit fears started to surface and everyone who wasn't hedged started to bid for short-term protection at ever higher premiums each day, leading to an inverted VIX curve at the front end and vol premiums to spike to crisis levels.

***

With U.S. Economic Policy Uncertainty (EPU) at current highs (see bottom pane), in the case of Brexit the U.S. EPU may rise substantially higher, pulling the VIX higher as well.

Goldman Sachs has more on the UK-US macro discrepancy and how that might affect the VIX:

"The VIX may reach the high 20’s to low 30’s if US EPU spikes. After languishing in the low teens over the past several months, last week the VIX broke through 20 for the first time since March. Given that the spread between the US and UK EPU indices is near an all-time high, in the case of a leave decision, it stands to reason that US policy uncertainty could be pulled higher. A simple back-of-the envelope calculation suggests that the current level of the UK EPU Index is consistent with an increase of 80 or so points in US EPU. Tying this back to the VIX, we arrive at VIX levels in the high 20s to low 30s."

***

Here's how analysts and banks see markets trade should Brexit be voted for, courtesy of Bloomberg:

Morgan Stanley

* Base-case index target for the FTSE 100 in case of ‘leave’ is range of 5000-5300; for the Euro Stoxx 50 is 2400-2550

BofAML

* Sees European stocks moving 10% either way after Brexit vote; “leave” result would be risk-off event not just in U.K. but also Europe and, to a lesser extent, globally

* Sell-off in Europe could translate into 6%-7% drop for S&P 500

* “Unquantifiable risk” whether other EU countries would then attempt to leave EU

* Long European low-risk dividend stocks, long SXDP index vs short SX3P index, long European index dividend futures, long MSCI EM

Goldman Sachs

* On average, the ERP (equity risk premium) has risen by ~150bps in past risk-off events. If Brexit were to result in similar scenario, rise in ERP of 150bps from end-May levels would push Stoxx 600 down to 280 and Euro Stoxx 50 to 2400

* Cleanest expression of Brexit risk is in U.K. domestic stocks (GSSTUKDE) and especially those with high sensitivity to investment spending

JPMorgan

* In ’leave’ scenario, euro-area equities would likely underperform U.K. ones, whose relative performance would be helped by GBP weakness

* Stays overweight on U.K. equities, which trade “outright cheap” on P/B metric

Citi

* Given recent equity weakness, likely policy reaction, new oil price regime, base-case Brexit downside risk is ~5%; at extreme end of the outcome spectrum, European stocks could fall 10-20%

* FX weakness, especially in U.K., is a key offset and should, in time, support positive U.K. returns, excluding return of full-blown systemic risk

Deutsche Bank

* Sees 10% downside for European equities

* Overweight FTSE, underweight DAX: if Brexit, U.K. equities would outperform European stocks, given likely GBP depreciation as well as U.K. market’s defensive sector structure

Jefferies

* Sees 5%-10% decline in FTSE banks, euro-zone banks falling by at least an equivalent, if not greater percentage

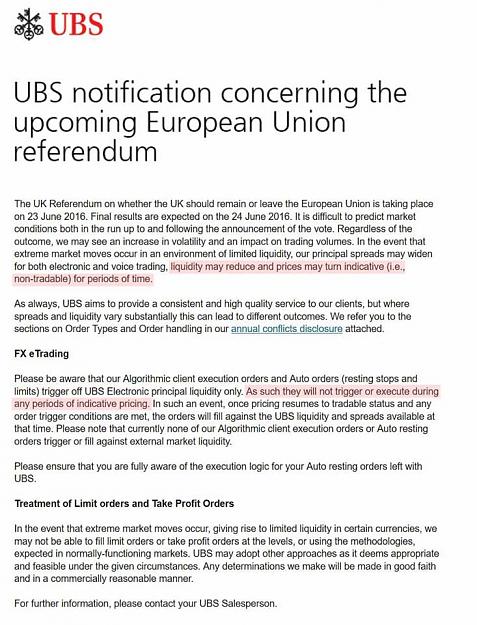

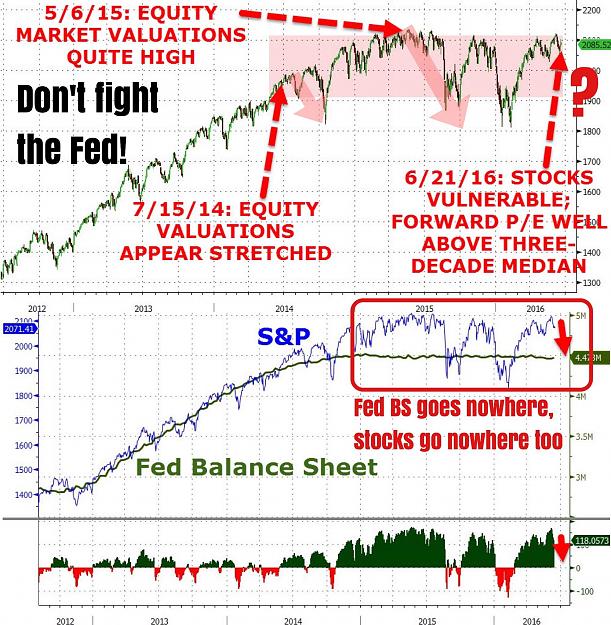

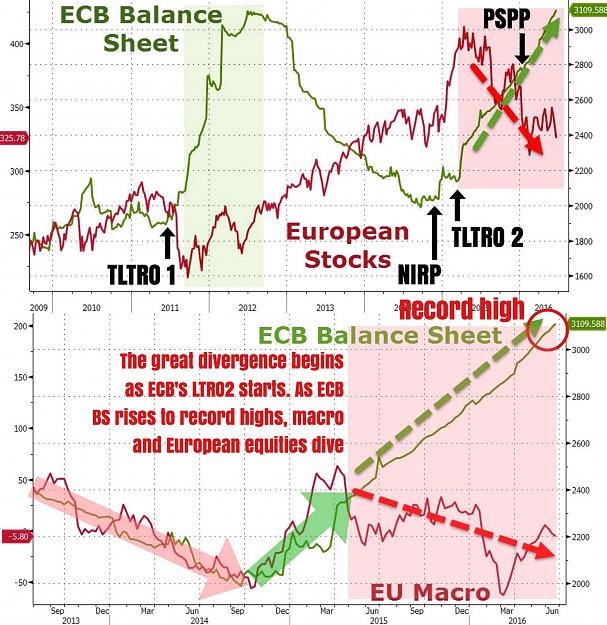

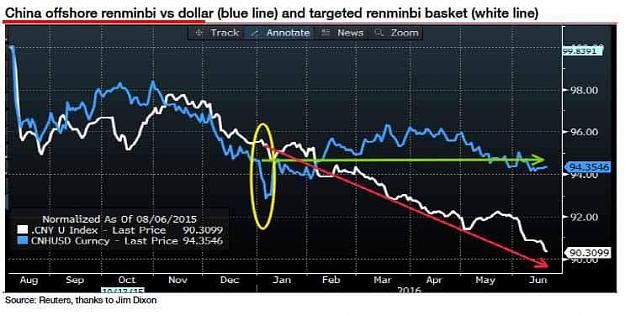

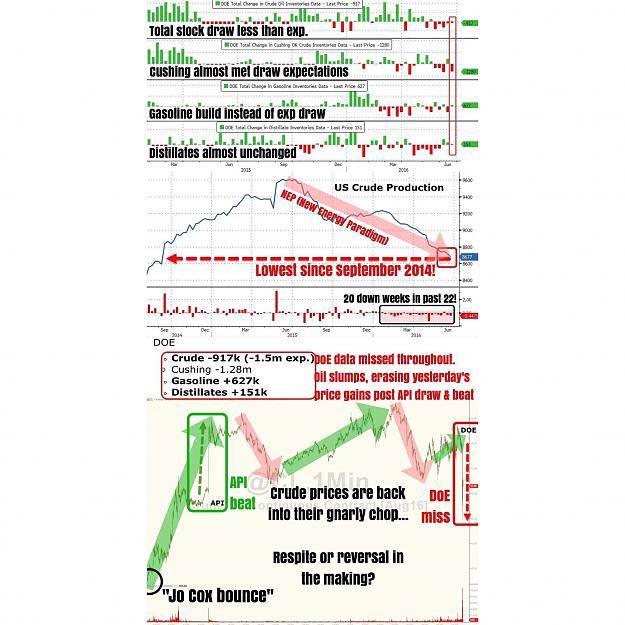

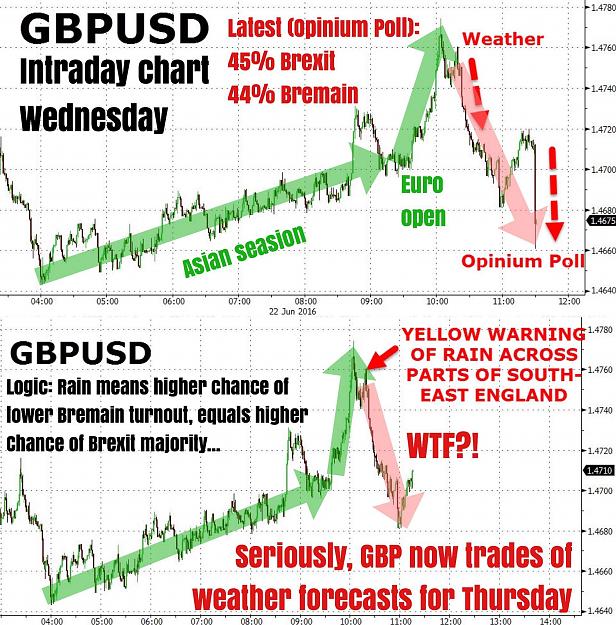

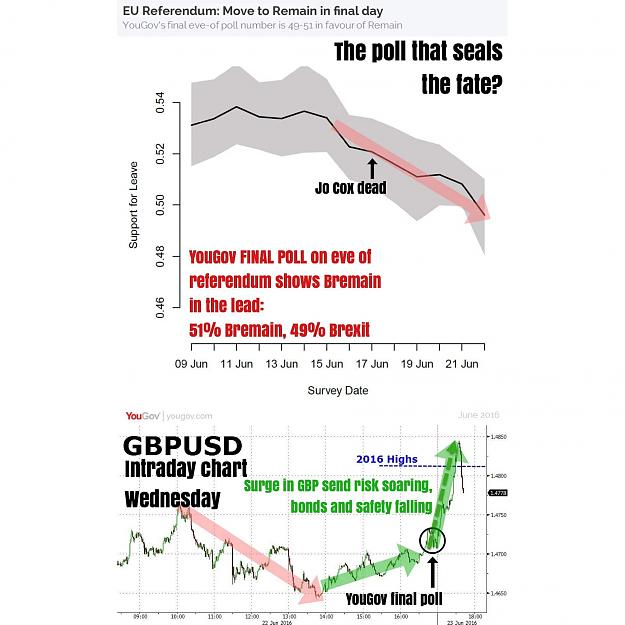

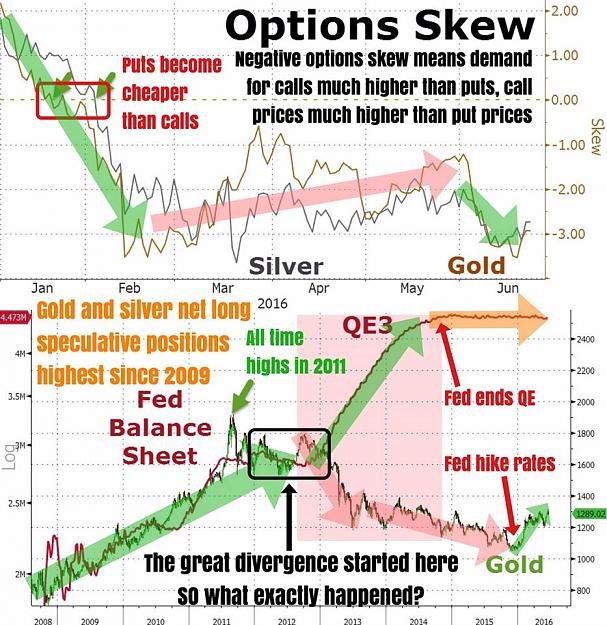

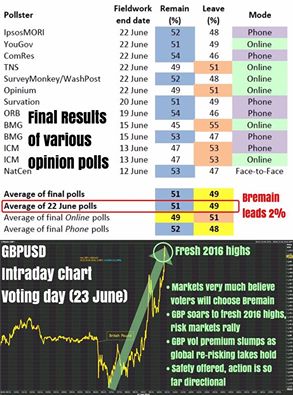

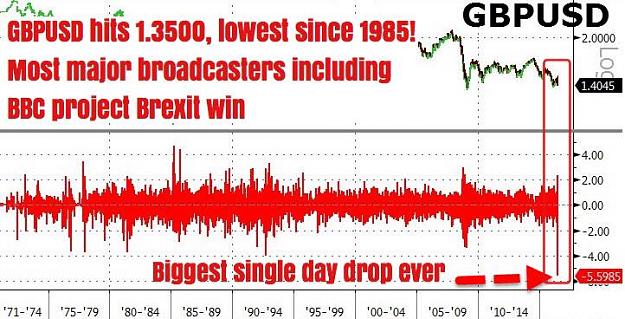

Attached Image (click to enlarge)