emailed out a lot of stuff, but for those without here are some things

CitiFX flow report

G10 Flows: Hazy, lazy days of summer

There are a few chances of some isolated storms as the market heads into summer; but for the moment, there’s not too much to report.

– AUDUSD: Turnover good; bias 57% in favor of selling

– NZDUSD: Turnover modest; bias 53% in favor of buying

– EURUSD: Turnover low; bias 51% in favor of selling

– USDJPY: Turnover good; bias 52% in favor of selling

– EURJPY: Turnover very low; small bias in favor of selling

– GBPUSD: Turnover reasonable; bias 55% in favor of buying

– EURGBP: Nothing of note

– USDCHF: Turnover so low, you can’t get under it

– EURCHF: Nothing of note

Goldman Sachs Summary of our Traders’ Strategies:

EUR: We remain core short, but we are mindful of the price action and will look to trade the range until further momentum emerges.

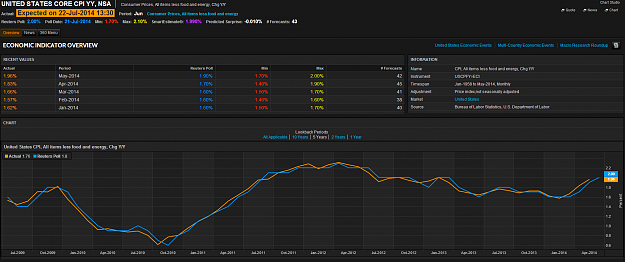

JPY: We are mindful of geo-political headlines throughout the course of the morning, however we feel the real catalyst today will be US CPI, with a strong print finally adding that risk premium into the front end of the US curve – we remain short USDJPY, but we will cut and re-assess through the 101.80 level.

GBP: Remain neutral in GBP at current levels but look to buy tactically on dips towards last week’s lows of 1.7037 in Cable, with 55dma 1.6941 below that of note - above 1.7120/40 resistance area.

AUD: US CPI at lunchtime today may see us break out of the tight range we have seen over the past few sessions – stops through the 0.9409/11 post employment double top potentially opening up a test of 0.9459/61.

JPMorgan

EUR

Yesterdays early AM bounce yesterday stalled at 1.35495, and the euro quickly retreated to the 1.3520s, where it is at the time of this writing. I had frankly expected a bit more of a short squeeze than that, and I was impressed by the way it sold back off so quickly. I slightly increased my short yesterday on the back of this price action. 1.3475 remains the crucial level on the downside, though selling technical breaks on no news is hardly a guaranteed strategy, as we saw last Friday. Those who have faded intermittent strength in this currency have fared better. On the calendar today is US CPI, which could potentially be the most important data point of the week, particularly if it surprises to the upside. Clearly the most watched global story at the moment is the Ukraine situation and the potential further sanctions against Russia that could emerge from the meeting of the EU Foreign Affairs Council, though it is not obvious what if any effect any of this will have on EURUSD. I remain short with partial stops at 1.3585 and 1.3715.

GBP

Another mundane Monday saw little change to prices and, consequently, there is little to add this morning. As stated previously, I have sold the EURGBP rally and will look to buy cable dips to 1.7040 with a stop sub-1.7000. We did see a little more profit taking in cable yesterday and, ahead of tomorrow's MPC minutes, that could continue today but sterling's underlying appeal remains. Only a move below 1.7000 or above 0.7965 in the cross would alter that view. This afternoon's US CPI data is more eagerly awaited than normal (released at 1.30pm) whilst UK public finance data is out at 9.30am. Good luck.

AUD

AUD a little higher overnight as Steven’s failed to mention the currency in his speech and surprisingly wasn’t asked about it in Q&A as he concentrated on monetary policy noting that “low interest rates are doing the sorts of things they normally do in most respects” and “up to this point we’re doing what can reasonably be done. But if there’s more that can reasonably be done at some point, then obviously we’d do that. But I’m content right now”. This now takes us to tonight’s 2Q CPI with market looking for headline +0.5% while RBA forecasts imply +0.4%.I would expect dips to be shallow ahead of the data with shorts and natural buyers disappointed that Steven’s didn’t continue jawboning the currency and would look for 0.9360/70 to contain the downside with a possible look up at 0.9420/30. NZD fairly quiet overnight and I would expect much of the same up until RBNZ tomorrow night with 0.8650/0.8730 a fair range ahead of the event. AUDNZD higher after Stevens speech and I expect this drift higher to continue into tonight’s Australian CPI with the 200 dma at 1.0884 a reasonable target.

CitiFX flow report

G10 Flows: Hazy, lazy days of summer

There are a few chances of some isolated storms as the market heads into summer; but for the moment, there’s not too much to report.

– AUDUSD: Turnover good; bias 57% in favor of selling

– NZDUSD: Turnover modest; bias 53% in favor of buying

– EURUSD: Turnover low; bias 51% in favor of selling

– USDJPY: Turnover good; bias 52% in favor of selling

– EURJPY: Turnover very low; small bias in favor of selling

– GBPUSD: Turnover reasonable; bias 55% in favor of buying

– EURGBP: Nothing of note

– USDCHF: Turnover so low, you can’t get under it

– EURCHF: Nothing of note

Goldman Sachs Summary of our Traders’ Strategies:

EUR: We remain core short, but we are mindful of the price action and will look to trade the range until further momentum emerges.

JPY: We are mindful of geo-political headlines throughout the course of the morning, however we feel the real catalyst today will be US CPI, with a strong print finally adding that risk premium into the front end of the US curve – we remain short USDJPY, but we will cut and re-assess through the 101.80 level.

GBP: Remain neutral in GBP at current levels but look to buy tactically on dips towards last week’s lows of 1.7037 in Cable, with 55dma 1.6941 below that of note - above 1.7120/40 resistance area.

AUD: US CPI at lunchtime today may see us break out of the tight range we have seen over the past few sessions – stops through the 0.9409/11 post employment double top potentially opening up a test of 0.9459/61.

JPMorgan

EUR

Yesterdays early AM bounce yesterday stalled at 1.35495, and the euro quickly retreated to the 1.3520s, where it is at the time of this writing. I had frankly expected a bit more of a short squeeze than that, and I was impressed by the way it sold back off so quickly. I slightly increased my short yesterday on the back of this price action. 1.3475 remains the crucial level on the downside, though selling technical breaks on no news is hardly a guaranteed strategy, as we saw last Friday. Those who have faded intermittent strength in this currency have fared better. On the calendar today is US CPI, which could potentially be the most important data point of the week, particularly if it surprises to the upside. Clearly the most watched global story at the moment is the Ukraine situation and the potential further sanctions against Russia that could emerge from the meeting of the EU Foreign Affairs Council, though it is not obvious what if any effect any of this will have on EURUSD. I remain short with partial stops at 1.3585 and 1.3715.

GBP

Another mundane Monday saw little change to prices and, consequently, there is little to add this morning. As stated previously, I have sold the EURGBP rally and will look to buy cable dips to 1.7040 with a stop sub-1.7000. We did see a little more profit taking in cable yesterday and, ahead of tomorrow's MPC minutes, that could continue today but sterling's underlying appeal remains. Only a move below 1.7000 or above 0.7965 in the cross would alter that view. This afternoon's US CPI data is more eagerly awaited than normal (released at 1.30pm) whilst UK public finance data is out at 9.30am. Good luck.

AUD

AUD a little higher overnight as Steven’s failed to mention the currency in his speech and surprisingly wasn’t asked about it in Q&A as he concentrated on monetary policy noting that “low interest rates are doing the sorts of things they normally do in most respects” and “up to this point we’re doing what can reasonably be done. But if there’s more that can reasonably be done at some point, then obviously we’d do that. But I’m content right now”. This now takes us to tonight’s 2Q CPI with market looking for headline +0.5% while RBA forecasts imply +0.4%.I would expect dips to be shallow ahead of the data with shorts and natural buyers disappointed that Steven’s didn’t continue jawboning the currency and would look for 0.9360/70 to contain the downside with a possible look up at 0.9420/30. NZD fairly quiet overnight and I would expect much of the same up until RBNZ tomorrow night with 0.8650/0.8730 a fair range ahead of the event. AUDNZD higher after Stevens speech and I expect this drift higher to continue into tonight’s Australian CPI with the 200 dma at 1.0884 a reasonable target.