Highlights of the latest Marker Research release on USD.

Full research available here.

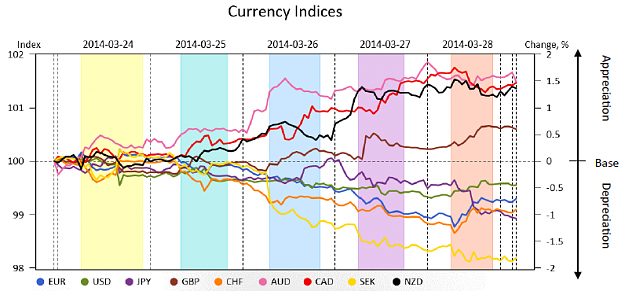

USD index, as most of the other currency indices, was a mediocre performer in the period of analysis. Only CAD and NZD indices managed to standout from the crowd. SEK demonstrated clear bearishness earlier in the period, but ended up with the rest of the indices on Monday. USD index started demonstrating clear bullish bias from mid day on Wednesday when it hit the period low (0.15% below the base value) at 10 GMT. Despite the worse than expected numbers earlier in the day, FOMC Meeting Minutes helped USD index to end the day 0.29% above the base value. Thursday did no bring much change as most of the US data came out better than expected.

Index continued to climb higher on Friday as all of the UK’s and some key Canadian numbers came out worse than expected and directed some flows in to the USD helping it to gain additional 0.1%. Substantially worse than expected Flash Services PMI numbers dragged the index closer to the base value. It ended Monday 0.3% lower than started. No major surprises were seen in numbers on Tuesday which allowed USD index to hold the status quo.

Gains and losses against other counterparts were rather marginal, most were in +/-0.2% range. Only noticeable results were seen against CAD, 1.23% gains, and NZD, 0.48% loss.

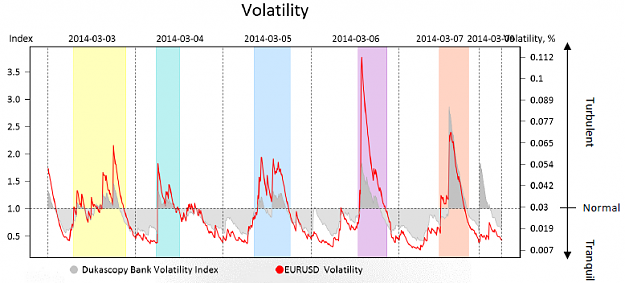

We saw a few rare cases when market (Dukascopy Bank Volatility Index) and EUR/USD showed substantially different reactions to the same events. First case took place on Thursday, when Chinese Flash Manufacturing PMI numbers shook the market (volatility 1.3 times higher than usual), but EUR/USD volatility was at 60-70% of it’s usual (long term) level. Second case was observed on Friday, when UK Retail Sales numbers came out. EUR/USD volatility approached, but remained below the long term value although market volatility at the same time was 1.2 times higher than usual. Despite the number of events/data releases on Wednesday the volatility was rather subdued, just slightly above the long term values.

Full research available here.

Attached Image (click to enlarge)

USD index, as most of the other currency indices, was a mediocre performer in the period of analysis. Only CAD and NZD indices managed to standout from the crowd. SEK demonstrated clear bearishness earlier in the period, but ended up with the rest of the indices on Monday. USD index started demonstrating clear bullish bias from mid day on Wednesday when it hit the period low (0.15% below the base value) at 10 GMT. Despite the worse than expected numbers earlier in the day, FOMC Meeting Minutes helped USD index to end the day 0.29% above the base value. Thursday did no bring much change as most of the US data came out better than expected.

Attached Image (click to enlarge)

Index continued to climb higher on Friday as all of the UK’s and some key Canadian numbers came out worse than expected and directed some flows in to the USD helping it to gain additional 0.1%. Substantially worse than expected Flash Services PMI numbers dragged the index closer to the base value. It ended Monday 0.3% lower than started. No major surprises were seen in numbers on Tuesday which allowed USD index to hold the status quo.

Gains and losses against other counterparts were rather marginal, most were in +/-0.2% range. Only noticeable results were seen against CAD, 1.23% gains, and NZD, 0.48% loss.

Attached Image (click to enlarge)

We saw a few rare cases when market (Dukascopy Bank Volatility Index) and EUR/USD showed substantially different reactions to the same events. First case took place on Thursday, when Chinese Flash Manufacturing PMI numbers shook the market (volatility 1.3 times higher than usual), but EUR/USD volatility was at 60-70% of it’s usual (long term) level. Second case was observed on Friday, when UK Retail Sales numbers came out. EUR/USD volatility approached, but remained below the long term value although market volatility at the same time was 1.2 times higher than usual. Despite the number of events/data releases on Wednesday the volatility was rather subdued, just slightly above the long term values.