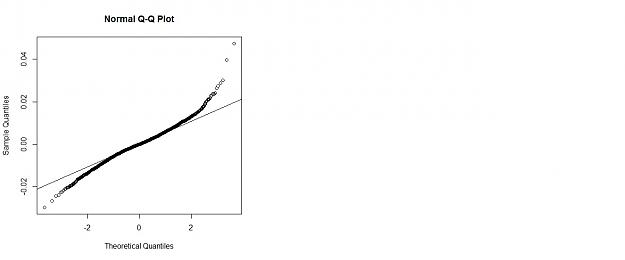

I think one of the biggest differences between profitable traders and unprofitable traders is that a profitable trader should pick a genuine price chart from a bunch of random ones, as nubs has apparently done. If you cannot identify nonrandom chart behavior you have no hope of exploiting it. Demonstrating nonrandomness in one chart though doesn't indicate nonrandomness in other charts - especially across different instruments. Finding patterns on a gold chart doesn't mean gbp/chf is exploitable.

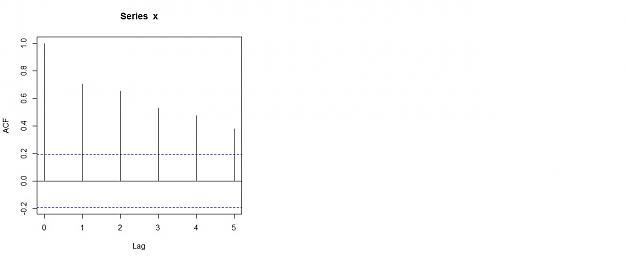

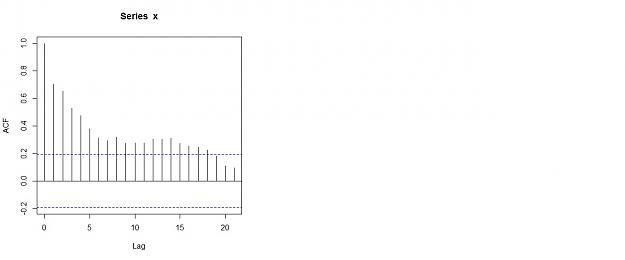

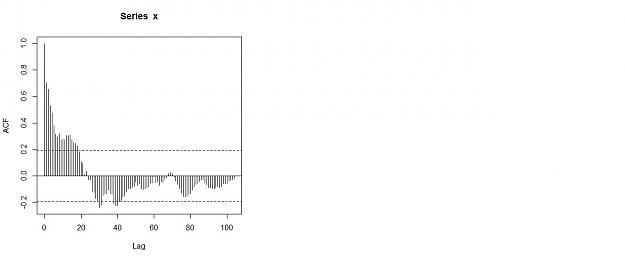

As you say, what nubcake called "swagger" is probably shifting volatility, which is a big indication of nonrandomness. I trade 1H charts with a 10 period ATR, which I use to time entries. A randomly generated price chart will show variable volatility and will exhibit patterns suggesting nonrandomness, but those patterns won't be repeated regularly. The way volatility rises and falls predictably at the same time every day is something a random generator cannot reproduce - even if its entries are increased and decreased throughout the day.

The fundamental picture also testifies against EMH. Pull up a daily USD/JPY chart, scroll back to reveal over a year of price action, and try to pinpoint the moment Shinzo Abe announced his intentions to pound the yen. It isn't hard to spot. Or look at the last six years on EUR/USD and correlate price action with various stages of the global financial crisis. These sweeping moves on long term charts create tremendous directional bias on short term charts.

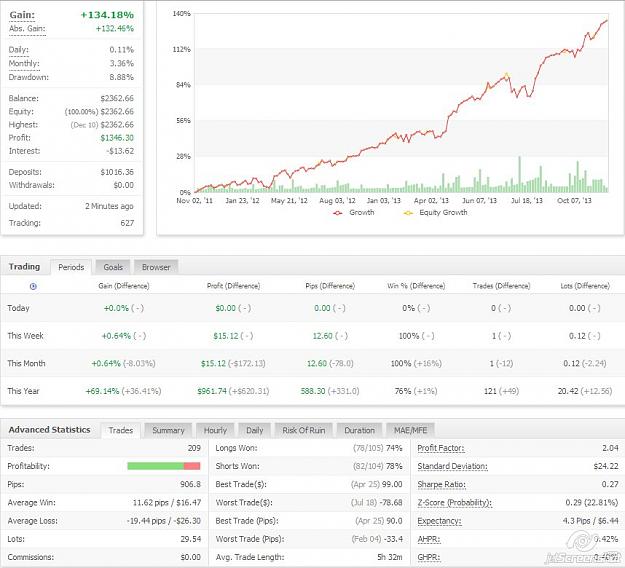

Finally, EMH implies that it is impossible to consistently and sustainably profit from price movements. Creative MM such as martingale can delay drawdowns to appear profitable in the short term, but if there is just one guy in the world steadily profiting from forex without doing this, that means EMH is wrong. And there are several MyFXbook accounts showing performances that cannot possibly be achieved without exploiting clear repeating, nonrandom chart behavior.

As you say, what nubcake called "swagger" is probably shifting volatility, which is a big indication of nonrandomness. I trade 1H charts with a 10 period ATR, which I use to time entries. A randomly generated price chart will show variable volatility and will exhibit patterns suggesting nonrandomness, but those patterns won't be repeated regularly. The way volatility rises and falls predictably at the same time every day is something a random generator cannot reproduce - even if its entries are increased and decreased throughout the day.

The fundamental picture also testifies against EMH. Pull up a daily USD/JPY chart, scroll back to reveal over a year of price action, and try to pinpoint the moment Shinzo Abe announced his intentions to pound the yen. It isn't hard to spot. Or look at the last six years on EUR/USD and correlate price action with various stages of the global financial crisis. These sweeping moves on long term charts create tremendous directional bias on short term charts.

Finally, EMH implies that it is impossible to consistently and sustainably profit from price movements. Creative MM such as martingale can delay drawdowns to appear profitable in the short term, but if there is just one guy in the world steadily profiting from forex without doing this, that means EMH is wrong. And there are several MyFXbook accounts showing performances that cannot possibly be achieved without exploiting clear repeating, nonrandom chart behavior.

si hoc legere scis nimium eruditionis habes

1