Highlights of the latest Marker Research release on EUR.

Full research available here.

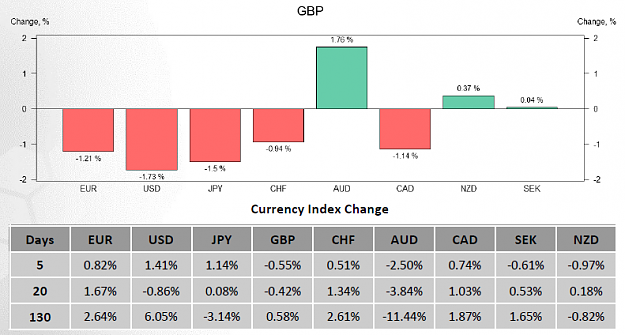

Unlike most of its major counterparts, the single European currency was not subjected to wide fluctuations in its the value. The five-day change totalled to merely 0.04%, whereas at the same time the New Zealand Dollar gained 0.86% and the U.S. Dollar plunged 0.97%. Other currencies finished the trading week somewhere in between. Accordingly, the Euro appreciated the most against the U.S. Dollar, namely 0.9%, but at the same time underperformed relative to the kiwi and the Yen—0.72 and 0.75 per cent respectively.

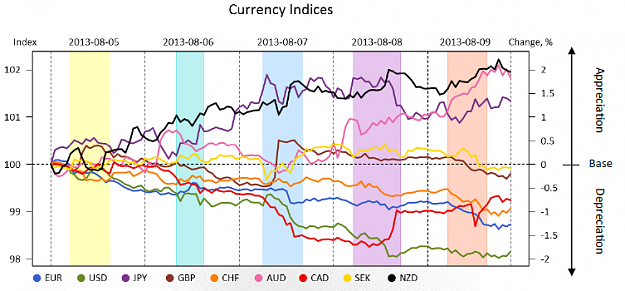

The farthest positive point from its base value the Euro’s equally-weighted index reached on Jul 24, when it surged up to 100.35 amid the promising statistics on the bloc’s secondary and tertiary sectors, even though the global sentiment suffered from the disappointing data on Chinese manufacturing industry that failed to pick up. The rally in the Euro, however, was stopped by the reports on the well-being of the U.S. economy, real estate and manufacturing of which seem to be improving.

The farthest negative level (99.77) was hit a day earlier, although there were no specific reasons for the investors to reduce their exposure towards the common currency. On the contrary, the context favoured bullish tendency, since the consumer sentiment appears to be gradually ameliorating, but was not realised.

Full research available here.

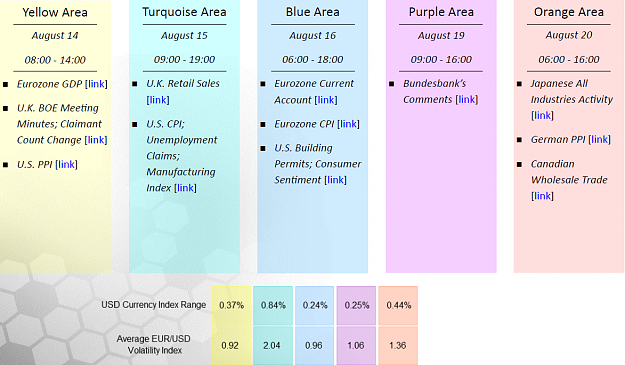

Attached Image (click to enlarge)

Unlike most of its major counterparts, the single European currency was not subjected to wide fluctuations in its the value. The five-day change totalled to merely 0.04%, whereas at the same time the New Zealand Dollar gained 0.86% and the U.S. Dollar plunged 0.97%. Other currencies finished the trading week somewhere in between. Accordingly, the Euro appreciated the most against the U.S. Dollar, namely 0.9%, but at the same time underperformed relative to the kiwi and the Yen—0.72 and 0.75 per cent respectively.

Attached Image (click to enlarge)

The farthest positive point from its base value the Euro’s equally-weighted index reached on Jul 24, when it surged up to 100.35 amid the promising statistics on the bloc’s secondary and tertiary sectors, even though the global sentiment suffered from the disappointing data on Chinese manufacturing industry that failed to pick up. The rally in the Euro, however, was stopped by the reports on the well-being of the U.S. economy, real estate and manufacturing of which seem to be improving.

The farthest negative level (99.77) was hit a day earlier, although there were no specific reasons for the investors to reduce their exposure towards the common currency. On the contrary, the context favoured bullish tendency, since the consumer sentiment appears to be gradually ameliorating, but was not realised.

Attached Image (click to enlarge)