This is why you've suggested cointegration is not an ultra-short TF type of strategy correct?

Since brokers give out less data on lower TF's. Could meshing 1 min TF data from historical sources with the live MT feed help overcome this challenge? Conceivably, this would widen our "assumption horizon"?

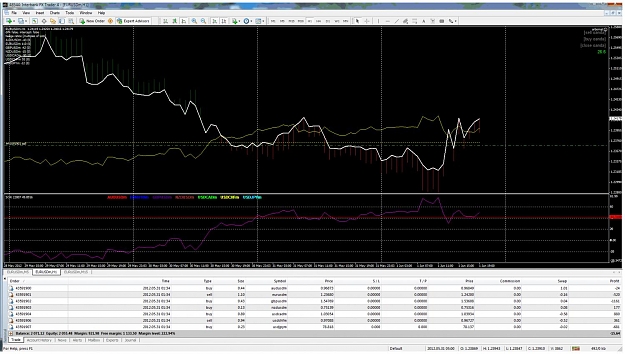

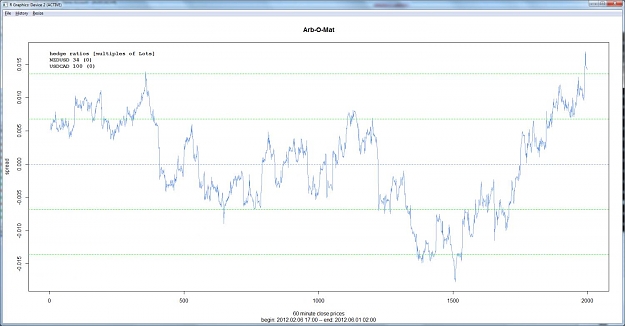

To everyone, I want to stress that I've focused most of my attention to only pair trading nzdusd // usdcad. If yoyu read 7bit's thread, this was used successfully about 2 years ago. As far as I can tell, the relationship remains strong. You can see I've posted 2 live trades on this hedge using the arbomat demo version. Both profitable. While the hedge calculations change, I've found on this pair (so far) don't appear to need any active balancing as is suggested on larger multi pair baskets.

Next live trade will be when price crosses below the 2nd horizontal line above mean:

If anyone sees a flaw in this approach let me know. Otherwise, I suggest others try it on demo and see how it goes.

One more edit then I'll shutup: I looked at a commercial cointegration platform just trying to glean some information. With equities, they look at the whole sector the stock is in. Cointegration could be tested on dozens or even hundreds of stocks in the same niche. This gives you more data points. How can we apply this logic to fx? Well usdcad nzdusd are both commodity currencies. So for fx standards, the same sector.

What other "sectors" based on fundamental information can we come up with? The possibilities are endless, but I think it would be interesting if people on the thread also looked at it from this angle.

Since brokers give out less data on lower TF's. Could meshing 1 min TF data from historical sources with the live MT feed help overcome this challenge? Conceivably, this would widen our "assumption horizon"?

To everyone, I want to stress that I've focused most of my attention to only pair trading nzdusd // usdcad. If yoyu read 7bit's thread, this was used successfully about 2 years ago. As far as I can tell, the relationship remains strong. You can see I've posted 2 live trades on this hedge using the arbomat demo version. Both profitable. While the hedge calculations change, I've found on this pair (so far) don't appear to need any active balancing as is suggested on larger multi pair baskets.

Next live trade will be when price crosses below the 2nd horizontal line above mean:

Attached Image (click to enlarge)

If anyone sees a flaw in this approach let me know. Otherwise, I suggest others try it on demo and see how it goes.

One more edit then I'll shutup: I looked at a commercial cointegration platform just trying to glean some information. With equities, they look at the whole sector the stock is in. Cointegration could be tested on dozens or even hundreds of stocks in the same niche. This gives you more data points. How can we apply this logic to fx? Well usdcad nzdusd are both commodity currencies. So for fx standards, the same sector.

What other "sectors" based on fundamental information can we come up with? The possibilities are endless, but I think it would be interesting if people on the thread also looked at it from this angle.

DislikedThis is actually a very good observation. Yes, it is repainting because the sizes (as Mediator pointed out) have changed. Everyone who tries this should study the following video and think about the implications. (make particular note of how much / how little the sizes change during this test period).

Holy Grail??? Or Not!

Also spending a few minutes reading through the early pages in this thread on the origins of arb-o-mat might be informational:

http://www.forexfactory.com/showthre...=262827&page=4...Ignored

Skype: heliosphan187