Good points. Dont think we need actual market prices to be normally distributed for reversion to mean to work. We can force data to exhibit normal properties through averaging. Individual candles contain a lot of data which is probably not centred by distribution. That's OK. Say if we take the individual midpoints of a series of candles, (H+L)/2, then apply an averaging function such as an MA to these calculated values, then this dataset will exhibit roughly normal tendencies (mean of means). Without even curve fitting an MA, price action will always "mysteriously" appear to be centred around or reverting towards the MA.

Really like CrucialPoint's insights into the use of MAs in forex trading. Dont have to use the midpoint in the exercise above but it aligns with what CrucialPoint says in his posts about using what is inside the pot to determine which way the wind is blowing.

Really like CrucialPoint's insights into the use of MAs in forex trading. Dont have to use the midpoint in the exercise above but it aligns with what CrucialPoint says in his posts about using what is inside the pot to determine which way the wind is blowing.

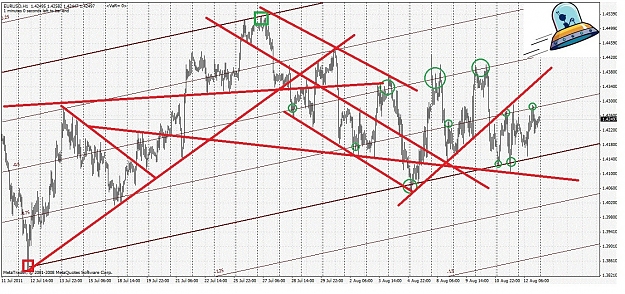

DislikedI don't know if Andrew's Pitchfork works or not, personally I doubt it. I did a rather crude mechanical test on my blog and couldn't find any evidence of reversion to the mean (or reversion to the median in my test's case) providing any kind of edge.

What the tests did show was that reversion to the mean strategies tend to win more often than they lose, but they don't win more than they lose, they lose more pips and it works out about 50/50 with no tradable edge. At least that was why my limited experiment showed.

http://www.myforexdot.org.uk/reversi...n-trading.html...Ignored

Audentes Fortuna Juvat