So the Hedge is multicollinearity or not ? spurious regressions or not ?

Ignored

Many of them are spurious from the beginning on or continue working only for a short time into the future, this is the main problem. Moving the "back"- and "now"-lines around on historical data and watching how it "behaves" will give you an impression what might happen to you when you buy or sell in a certain situation, how much history is needed, how long it usually lasts, etc.

Multicollinearity exists but can be safely ignored because multicollinearity does not have any influence on the prediction performance of a linear regression model.

thank you very much 7bit for sharing your knowledge , may you explain about diff and intercept in setting of your expert (in fact indicator) and What does differ it if we change false to true in this two selections ? i changed it and for example when diff was false, the graph of Arb-O-Mat was totally in a range situation but when changed to true, it got in a trendy situation and the lot ratios differed too.thank you again 7bit.

thank you very much 7bit for sharing your knowledge , may you explain about diff and intercept in setting

Ignored

I'm not going to answer this question yet another time.

Go back to the beginning of the thread and start reading it in its entirity. I'm not going to explain the same things repeatedly every week again and again and again. Its all archived in the thread for exactly this purpose. Also you should read the source code, there you will see much clearer than I could ever explain what exactly it does.

Also there is not much new "knowledge" coming from me, I only did the boring and time consuming job of coding some existing concepts in mql4.

I'm not going to answer this question yet another time.

Go back to the beginning of the thread and start reading it in its entirity. I'm not going to explain the same things repeatedly every week again and again and again. Its all archived in the thread for exactly this purpose. Also you should read the source code, there you will see much clearer than I could ever explain what exactly it does.

Also there is not much new "knowledge" coming from me, I only did the boring and time consuming job of coding some existing concepts in mql4.

Ignored

yes, you're right, this tool is very tempting so i'm testing it on a demo account and i think if we spend time on it, we can make a profitable strategy with it. also i have a suggestion : may you add gold and silver ?

as you know this metals have high correlation with some currencies like AUD ,NZD,CAD and it can increase ability of this indicator, in other hand gold or silver versus all currency in long period of time will be in an up trend because of inflation in all currencies hence trendomat indicator can be more reliable. Danke shön 7bit.

I was under the impression that R was supposed to execute faster than mql4 code, but my indicator is pretty slow

I need a linear regression indicator (of price to time for a single currency) that can execute very quickly for optimization purposes.

I think my code is redundant (I am regenerating the data arrays each time), but I can't figure out how to push a new value onto the vector. If you have a moment to glance over the following code I would be much obliged.

I was under the impression that R was supposed to execute faster than mql4 code, but my indicator is pretty slow

Ignored

You are moving the entire array to R and the results back evey time. This will take the most time.

You can do the following on every new bar:

RAssignDouble(R, "hist0", Close[0]);

// the newest is at position 1

RExecute(R, "hist <- c(hist0, hist)"); // insert it at the beginning

RExecute(R, "hist <- hist[-length(hist)]") // remove the last element

and the same also with "time". Maybe you could combine the last two lines in one, I wrote it in two lines to make it more clear, you should test it on the R console first to make sure that it really removes the last element, I haven't tested this.

Make sure you call this only on every bar and not on every tick. Also I am not sure why you rev() the prediction, it should already be in the order newest first, oldest last, the same way the MT4 buffers need it (I haven't tested it and might be wrong but this look strange to me)

Also is it really needed to copy the whole regression line point by point into the indicator buffer everytime? Maybe you only need slope and intercept or only the last value for the calculations in your EA.

And btw. you don't need rIsBusy() since you dont use RExecuteAsync() anywhere, there is no way it could ever be busy without executing something async, likewise you also don't need to order the code backwards and use exists() like you do it, since this looks confusing, this was only needed in my example where I used RExecuteAsync() and there existed parallel execution and the calculations from the last start() were not completed when the next start() began. But this kind of asynchounouus execution would not work when using it in the backtester anyways since in the tester it MUST block and complete all calculations before it may move on to the next tick.

If you just need a drop in replacement for the regression line indicator you should maybe really think about re-implementing the indicator in Pascal, this is how I would do it, begin with my improved SMA example somewhere near the end of the Lazarus thread as a starting point to see how to write into indicator buffers from within the dll.

Thanks for the response. I will try your suggestions.

I read your object pascal thread and I initially intended to port the indicator to that but I was somewhat overwhelmed by the syntax. It seems like that might be the way to go after all.

I read your object pascal thread [...] but I was somewhat overwhelmed by the syntax.

Ignored

You will love the Pascal syntax and grammar once you are a bit more familiar with it.

You will find that it is by orders of magnitude less complex and has less anomalies than C++ (or any other C-like language) without sacrificing any expressiveness. The fact that type identifiers are written to the right side of a variable and not to the left - and generally the fact that the placement of a syntax element tells everything about its meaning - helps making the grammar completely context insensitive which is the reason why people intuitively find it easy to read and the compiler needs only one pass and the parser needs no symbol table which makes it roughly 10 times faster than any C++ compiler to parse and compile any given snippet of code.

Even today's modern languages like Scala are now borrowing from these old and proven concepts to make things possible that would not have been thinkable with a C++ like grammar and most mission critical software in aircrafts, spacecrafts and military applications today is written in Ada (which evolved from the Pascal family of languages) rather than in C++ because the strict and regular Pascal-like language grammar allows the correct functioning of a piece of software to be mathematically proven from analyzing the source code alone while in a C++ like language you have to actually run it and do trial and error and hope for the best which is simply not acceptable for certain mission critical applications.

I am aware that the above statements have the potential to incite a religious programming language flame war. Let it begin ;-)

Many thanks for sharing this great work, 7bit. Excellence in action.

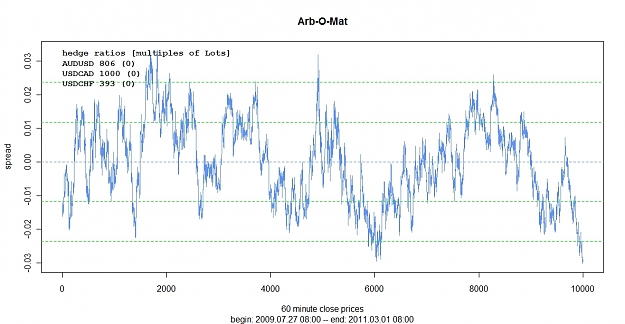

My question is similar to the one addressed below. I tried to use other indices than forex pairs, and for some reason it appears to always give them 0 loading.

Do I do something wrong, or is there an easy way to fix this?

I tried to use other indices than forex pairs, and for some reason it appears to always give them 0 loading.

Ignored

After the regression the coefficients are multiplied by a certain factor to get lot sizes for dollar based lots. These factors are determined by the name of the instrument, it only works when there is "USD" in the name and it depends on whether it is xxx/USD or USD/xxx.

This is also the reason it does not work with crosses xxx/yyy without USD. It could be made to work but I simply did not because it is only an experimental proof of concept, a rough prototype, a quick and dirty hack, not more.

I chose this rather strange way of determining the factor to be able to run it in the strategy tester. In the strategy tester you cannot use MarketInfo() to determine the tick values and Lot sizes of other instruments than the one of the current chart (Strategy tester is the most half-baked and buggy component of the entire MT4 platform).

You would have to modify the code that calculates these factors, the best way would be to use information returned by MarketInfo(). I don't have any indices on my platform, I have only forex, so I did not include any code to deal with it.

You would have to modify the code that calculates these factors, the best way would be to use information returned by MarketInfo(). I don't have any indices on my platform, I have only forex, so I did not include any code to deal with it.

Ignored

Thank you for your reply!

Well, I would call this a little more than a dirty hack... And I certainly appreciate that you stayed away from MarketInfo(). I hate EAs that overuse MarketInfo() and then leave you stranded with the Strategy Tester.

I added a line of code that recognizes the first 3 letters of the non-usd symbol, and weighs the coef[i]. Now it seems to recognize it. I only have to figure out if I have to use the contract size or the tick value (tick sizes are all different). Always confuses the heck out of me.

Thanks again for this great tool.

p.s. If you revamp the EAs some day - would be great to have an input parameter that determines how frequently you want to refresh your calculations. For people like me who have old computers with the small brain of an automatic toaster.

The "BasketFile" blank input is a kind of "set file" you can set, which shall contain the basket description.

It is a replacement for the "BasketPairs" inputs.

You can "save" your baskets into various basket files and load them easily that way....

Ignored

As a possible connection between your indi and a trading EA, as it reads a file with the currencies and weights of them to trade a basket.

|

Joined Aug 2010

|

Status: Master ur EXIT. Entry is secondary.

|29 Posts

Took this H1 tf trade earlier today on demo. Looks like a nice stable basket. Ive had 5 consecutive winners on different baskets and tf's in the last 2 weeks. No losses yet. I am really liking this bit of coding brilliance Prof 7Bit. I'm busy digging deep into "R" and you have certainly opened my eyes to "basket trading" and its many NEW possibilities. Thank you for sharing!