DislikedCould you give us an update on your strategies that you described with your alpha factory, are they profitable.Ignored

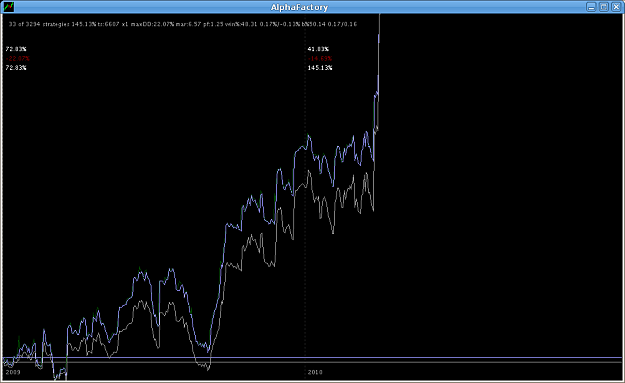

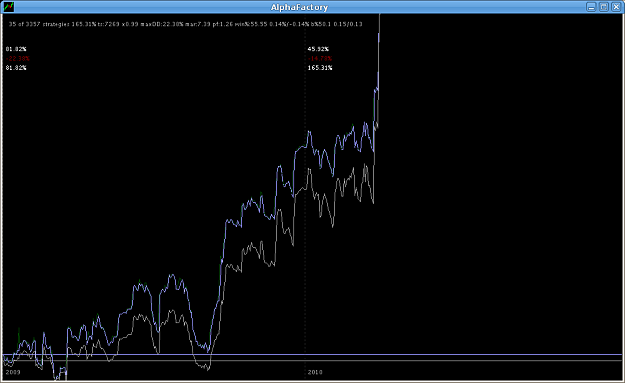

I should note that I only use 4 pairs (EURUSD, GBPUSD, USDJPY and AUDUSD) and the stats I have shown include commissions (I padded spread a bit more than necessary to include slippage as well).

The problem with only 4 markets is that there is quite a lot of correlation between them so I don't get as smooth curve as I would like to and as everyone knows (or should know

I think I also have quite a solid fitness algo which is IMHO one of the most important things. I'm still not sure if it's even near optimal - trading is not exactly the easiest data to optimize to.

I'm moving to different architecture in my testing (totally event driven) after that I think I can speed the optimization at least 10-100x (see my earlier post about this). After that I think I'll have much more interesting pics, my current tests are about 10000-20000 iterations.

I'm quite intersted, those people who have event driven platforms already, have you done optimal method searches and what kind of results have you gotten in-sample vs out-sample.