The power of compounding magnifies every trading mistake we make and slippage we experience. If one has a system with a CAGR ("Compounded Annual Growth Rate") of 30%, a negative trading mistake of $10 from a trade today would result in $137.86 lesser profits at the end of the next 10 years.

In this journal, I will record my weekly trading deviation. I define the trading deviation of a trade as:

In this journal, I will record my weekly trading deviation. I define the trading deviation of a trade as:

(Pips gained in live trading - Pips gained in backtesting) / Distance of stop loss

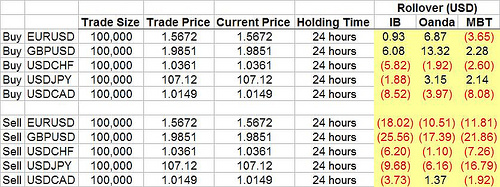

In my backtests, I assume trading costs of 2 pips for EUR/USD, 3 pips for USD/CHF, 2 pips for USD/JPY, 4 pips for GBP/USD, 4 pips for USD/CAD and 7 pips for GBP/JPY.

As a example, I put on a USD/CHF trade with a stop loss of 50 pips. In my live trading, I was stopped out for a loss of 54 pips. In my backtesting, I will be stopped out for a loss of 50+3=53 pips (distance of stop loss plus cost of trading of 3 pips). My trading deviation for this trade is:

[-54 - (-53)] / 50 = -1 / 50 = -0.02