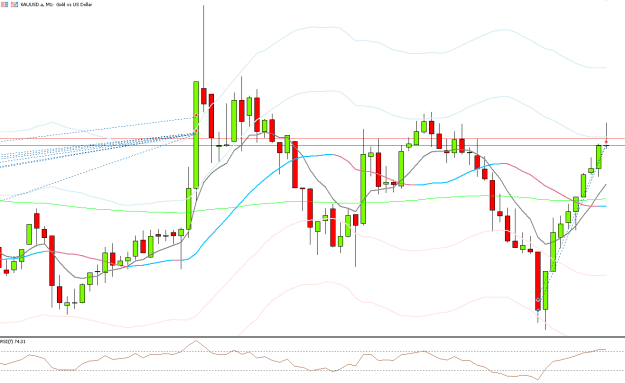

Dislikedthanks for the detailed information Abade, it has cleared up the jargon for me! i understand the need to use tick data in mt4 for accurate back testing, but i'm still not sure why if the back tester runs per tick it is still an issue in mt5? renko with wicks caught my attention as they appear to provide more price action, i may explore those a bit further, but i also think the renko overlay serves the same purpose with even more detail and it can also be dynamically adjusted according to ATR {quote} i knocked it up myself so you won't find it unless...Ignored

MT5 will only use tick data if it is available for any given period. Sadly, MT5 will only store a few months worth of tick data from the broker, so we have to download it externally and create custom instruments if we want extended periods of it.

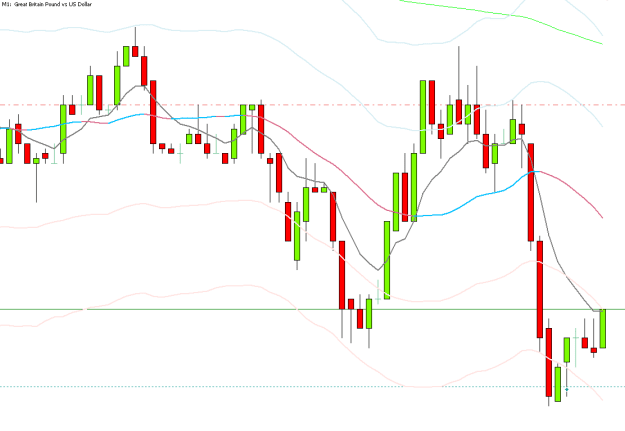

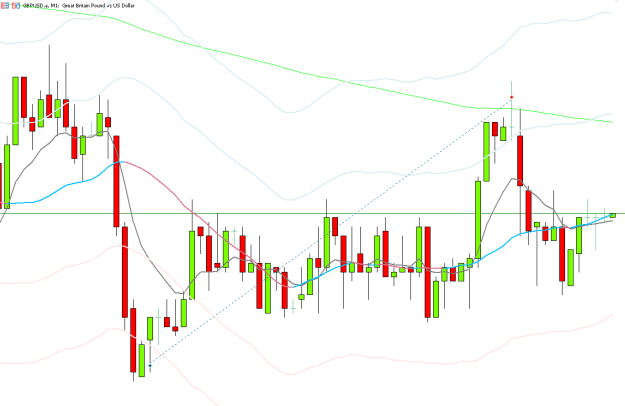

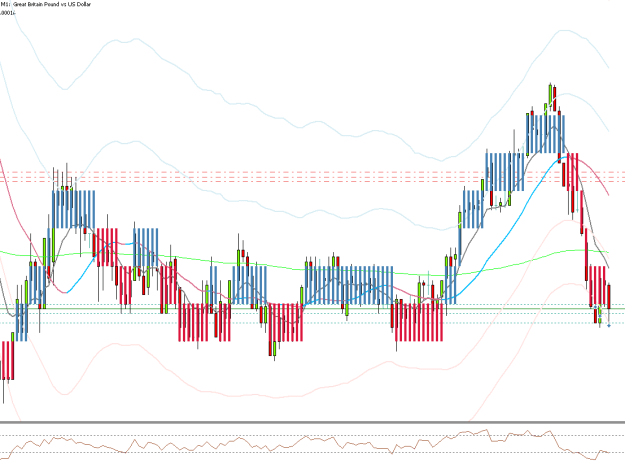

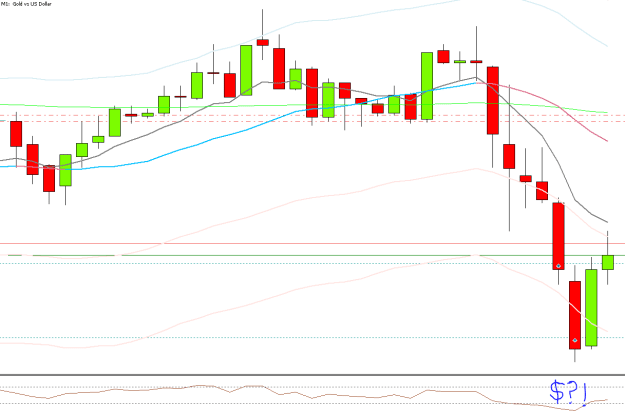

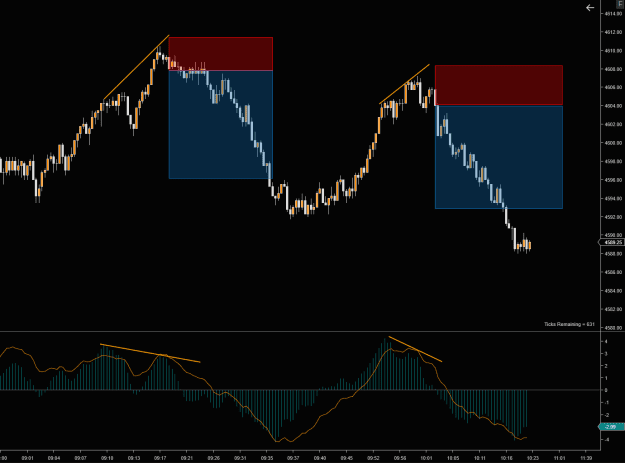

I personally don't use "tick by tick" modelling for developing, as my systems don't use any kind of inside bar information/execution, they only operate close by close, therefore anything beyond "Open prices only" modelling is overkill. However, the true value of tick data (for me) is to build the charts with the highest degree of detail available. For example, if we used 4 hour OHLC (very low detail) to build a renko chart it would look like this:

Attached Image (click to enlarge)

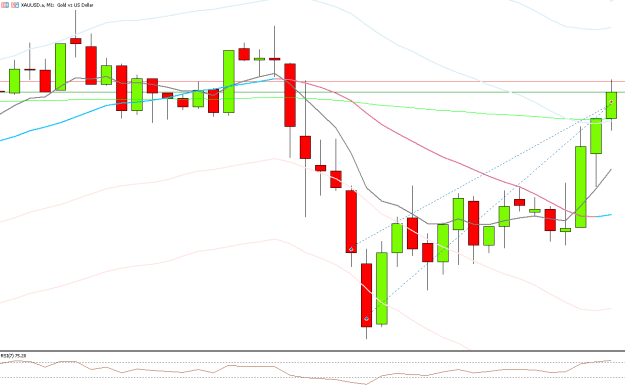

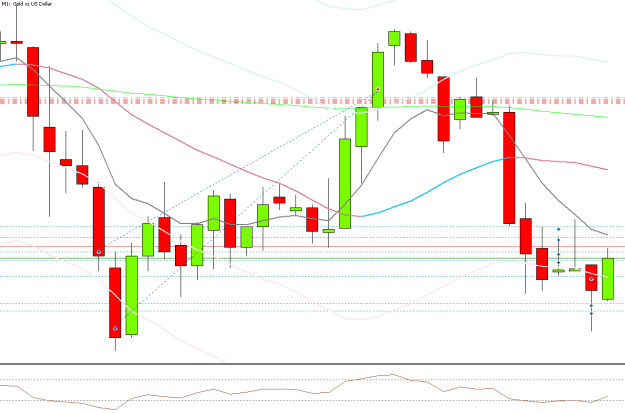

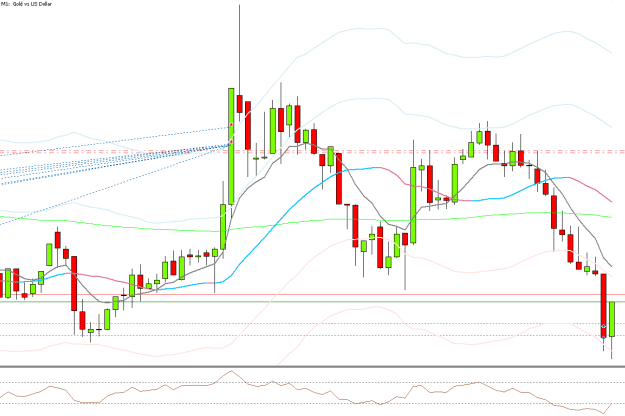

It looks extremely lean and nice, so much that it could be traded without any kind of analysis. However, we both know that real price chops a lot more than that. The detail is lost so the chart is useless for any kind of development. Something similar happens when 1 minute OHLC data and a small brick size is used, but to a lesser degree. Of course, if we run live charts 24/7 and we don't care about the distant past this is no issue at all, and the charts will have the highest degree of detail available by default.

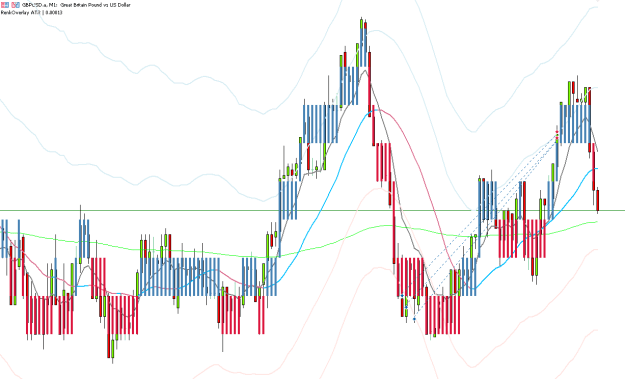

ATR adjusted overlay renko is a worthwhile experiment for sure! I am looking forward for new developments, experiments and findings, thanks for sharing

1