Key USD bearish threshold remains intact

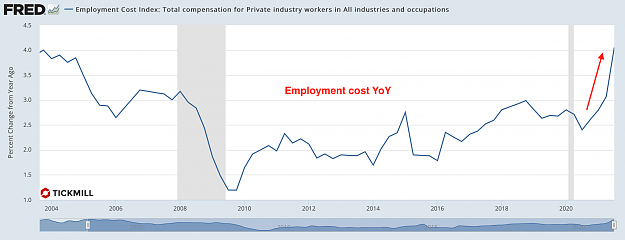

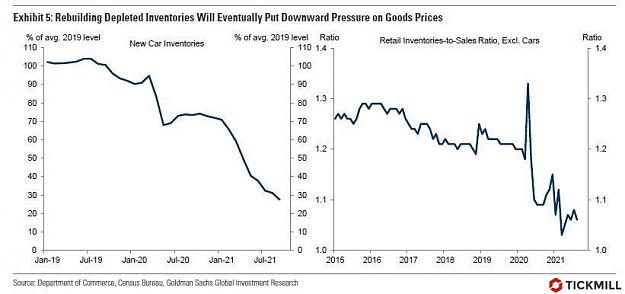

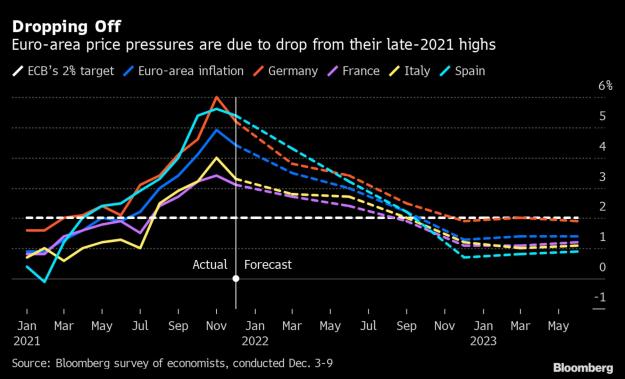

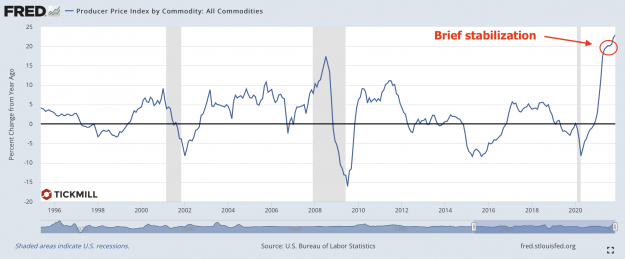

Eurozone inflation was materially higher than the consensus forecast in October, making it slightly difficult for the ECB to maintain a huge stimulus bias in the monetary policy. The data on Friday showed that the broad rise in prices in October amounted to 4.1% (forecast 3.7%). At the same time, core inflation, which doesn’t include fuel and other goods with volatile prices, also beat the forecast - 2.1% versus the expected 1.7%:

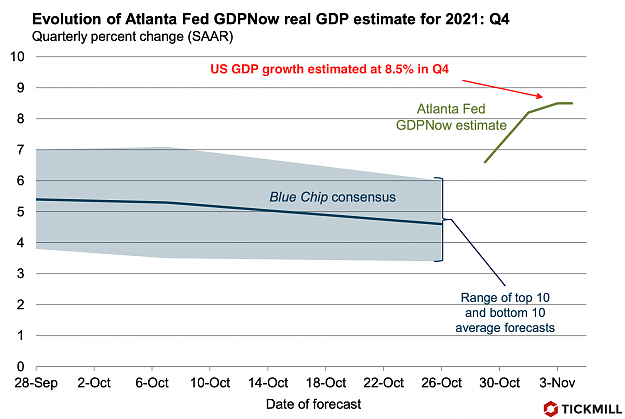

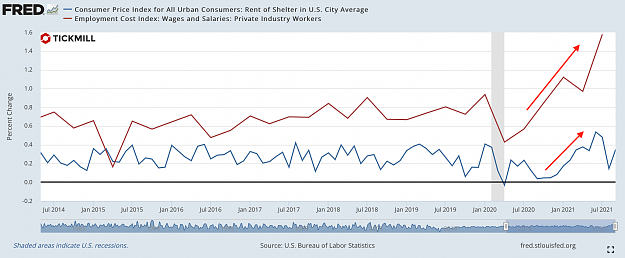

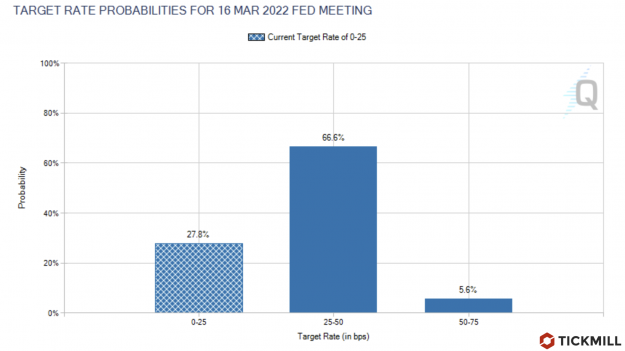

At a meeting on Thursday, the ECB gave a signal that officials are closely monitoring inflation, but still expect it to decay sooner than markets fear. Some officials, though, see a second round of inflationary effects, primarily caused by wage inflation, so they do not exclude that consumer inflation will remain above the target level of the ECB in 2023. In general, we can say that the European Central Bank signaled a reduction in asset purchases in December, which caused widening spreads between sovereign bonds of Eurozone countries and a positive reaction from the euro. The spread between the 10-year bonds of Italy and Germany jumped by 7 bp on Thursday as market participants became more confident that the ECB's artificial support for "second tier" EU sovereign bonds will soon begin to decline. Today this spread has added another 10 bp:

In addition to the factor of December tapering, Eurozone sovereign bonds are declining in price due to the risks of an early start of the ECB tightening cycle. Although Lagarde said it was important not to overreact to temporary supply shocks, the effects of which would soon wear off, market participants shifted their expectations of the ECB's first rate hike to October 2022, i.e. even earlier than previously expected. It is clear that the opinion of market participants regarding persistence of inflation is now very different from the opinion of the ECB, and if inflation risks do not materialize, battered bond prices may quickly recover, since the inflation premium will ultimately unwind. The euro will definitely benefit from this trend.

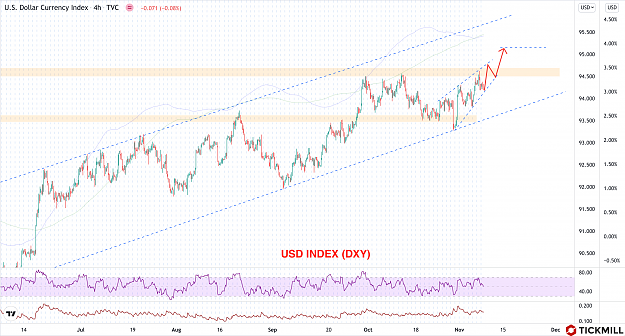

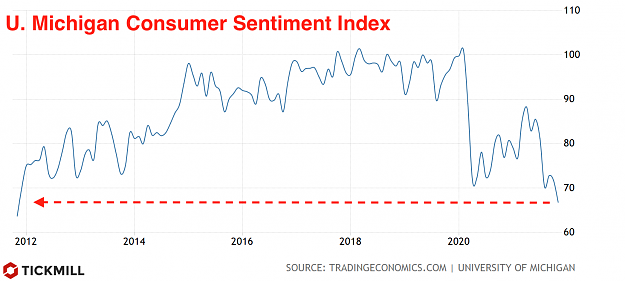

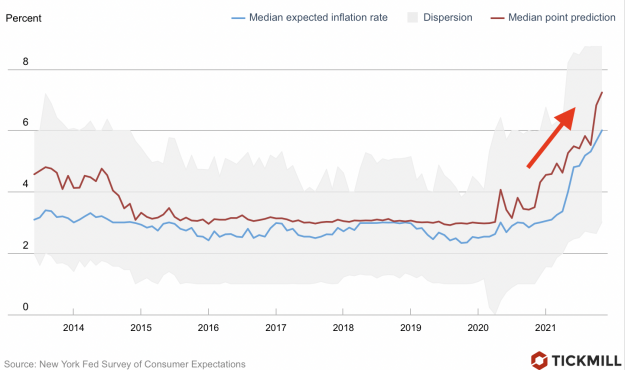

Today, the data is due on US inflation and consumer sentiment from U. Michigan for October, key for the Fed's policy. A higher-than-expected rate of inflation, measured in terms of percentage growth of consumer spending, could mean a more aggressive pace of phasing out the Fed's asset purchases, which it is likely to announce in November. Next week, market participants will focus on the October Non-Farm Payrolls report, which will additionally help to improve expectations about the Fed’s policy move in the near future. Risks for the dollar are biased towards further growth next week as this week's correction appears to have been run out of steam. If DXY manages to close above 93.50 mark, this should be another strong technical signal for recovery next week, since a key bullish trendline will remain intact:

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Eurozone inflation was materially higher than the consensus forecast in October, making it slightly difficult for the ECB to maintain a huge stimulus bias in the monetary policy. The data on Friday showed that the broad rise in prices in October amounted to 4.1% (forecast 3.7%). At the same time, core inflation, which doesn’t include fuel and other goods with volatile prices, also beat the forecast - 2.1% versus the expected 1.7%:

Attached Image (click to enlarge)

At a meeting on Thursday, the ECB gave a signal that officials are closely monitoring inflation, but still expect it to decay sooner than markets fear. Some officials, though, see a second round of inflationary effects, primarily caused by wage inflation, so they do not exclude that consumer inflation will remain above the target level of the ECB in 2023. In general, we can say that the European Central Bank signaled a reduction in asset purchases in December, which caused widening spreads between sovereign bonds of Eurozone countries and a positive reaction from the euro. The spread between the 10-year bonds of Italy and Germany jumped by 7 bp on Thursday as market participants became more confident that the ECB's artificial support for "second tier" EU sovereign bonds will soon begin to decline. Today this spread has added another 10 bp:

Attached Image (click to enlarge)

In addition to the factor of December tapering, Eurozone sovereign bonds are declining in price due to the risks of an early start of the ECB tightening cycle. Although Lagarde said it was important not to overreact to temporary supply shocks, the effects of which would soon wear off, market participants shifted their expectations of the ECB's first rate hike to October 2022, i.e. even earlier than previously expected. It is clear that the opinion of market participants regarding persistence of inflation is now very different from the opinion of the ECB, and if inflation risks do not materialize, battered bond prices may quickly recover, since the inflation premium will ultimately unwind. The euro will definitely benefit from this trend.

Today, the data is due on US inflation and consumer sentiment from U. Michigan for October, key for the Fed's policy. A higher-than-expected rate of inflation, measured in terms of percentage growth of consumer spending, could mean a more aggressive pace of phasing out the Fed's asset purchases, which it is likely to announce in November. Next week, market participants will focus on the October Non-Farm Payrolls report, which will additionally help to improve expectations about the Fed’s policy move in the near future. Risks for the dollar are biased towards further growth next week as this week's correction appears to have been run out of steam. If DXY manages to close above 93.50 mark, this should be another strong technical signal for recovery next week, since a key bullish trendline will remain intact:

Attached Image (click to enlarge)

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.