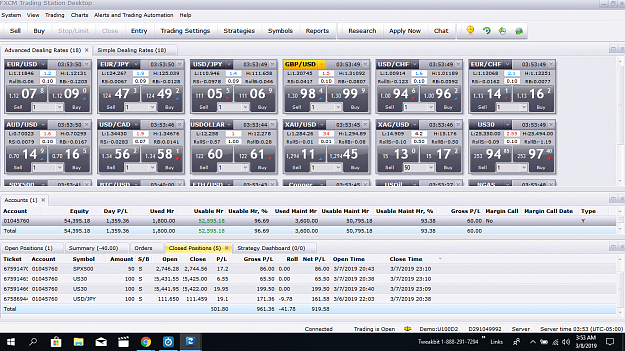

DislikedTicket Account Symbol Amount S/B Open Close P/L Gross P/L Roll Net P/L Open Time Close Time 67591470 01045760 SPX500 50 S 2,746.28 2,744.56 17.2 86.00 0.00 86.00 2019-03-07 20:43 2019-03-07 23:10 67591463 01045760 US30 100 S 25,431.55 25,425.00 6.55 65.50 0.00 65.50 2019-03-07 20:38 2019-03-07 23:10 67591466 01045760 US30 100 S 25,441.95 25,422.00 19.95 199.50 0.00 199.50 2019-03-07 20:40 2019-03-07 23:09 67586944 01045760 USD/JPY 100 S 111.650 111.459 19.1 171.36 -9.78 161.58 2019-03-06 22:03 2019-03-07 20:38 Total 62.80 522.36 -9.78 512.58 tonight...Ignored

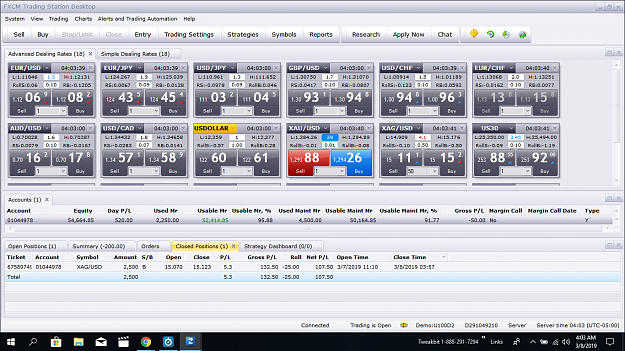

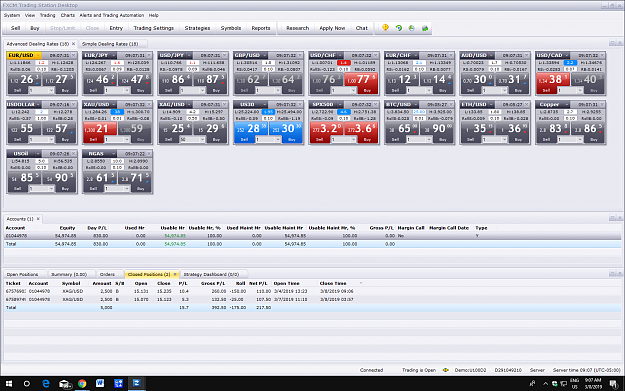

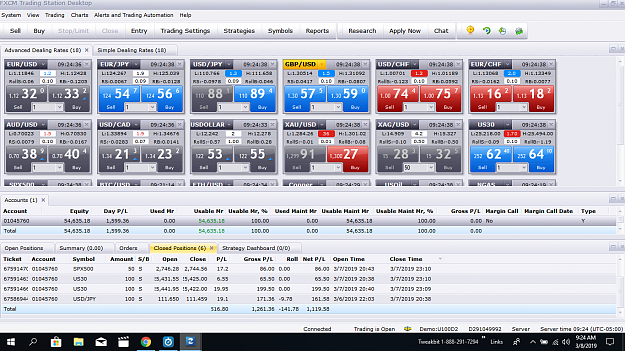

Attached Image (click to enlarge)