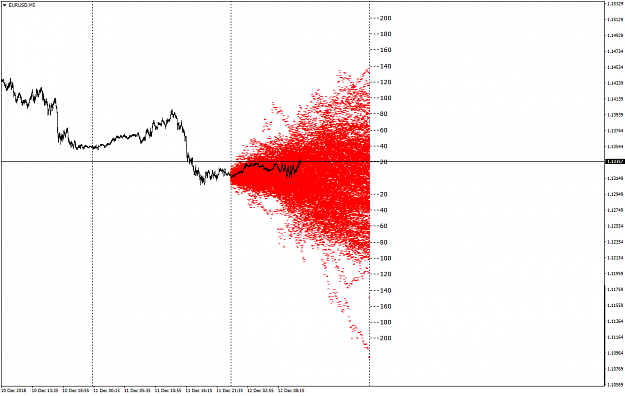

@AO: Your proposition is that the overall market movement is constant. Right?

Now let's consider a triangulated market with just 3 currencies A, B, and C. Then M(A) + M(B) + M(C) = const for 1 time unit (where M(X) is the sum of all movements of the currency X). Is this what you are saying or do I misinterpret/misunderstand your point?

I've thought that whenever the currency pair AB moves strongly, AB, AC, and thus BC have to react (move) strongly, too.

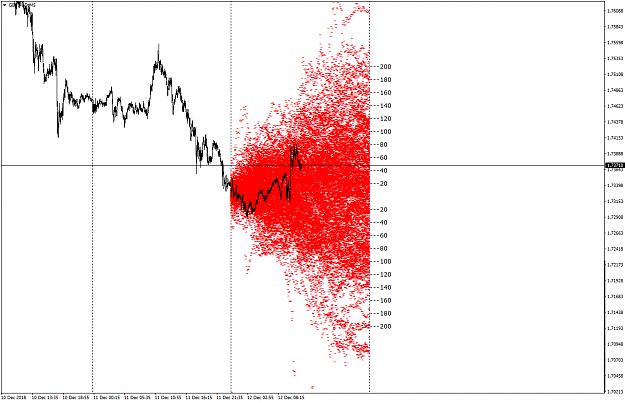

Now let's consider a triangulated market with just 3 currencies A, B, and C. Then M(A) + M(B) + M(C) = const for 1 time unit (where M(X) is the sum of all movements of the currency X). Is this what you are saying or do I misinterpret/misunderstand your point?

I've thought that whenever the currency pair AB moves strongly, AB, AC, and thus BC have to react (move) strongly, too.