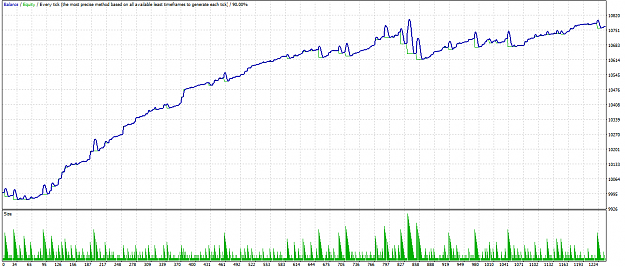

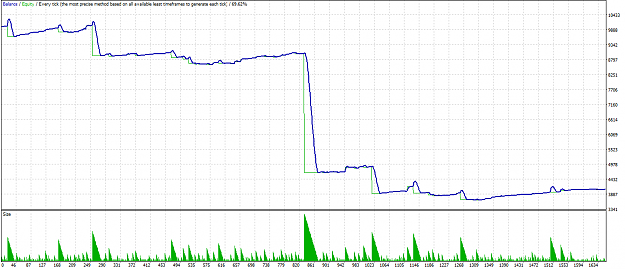

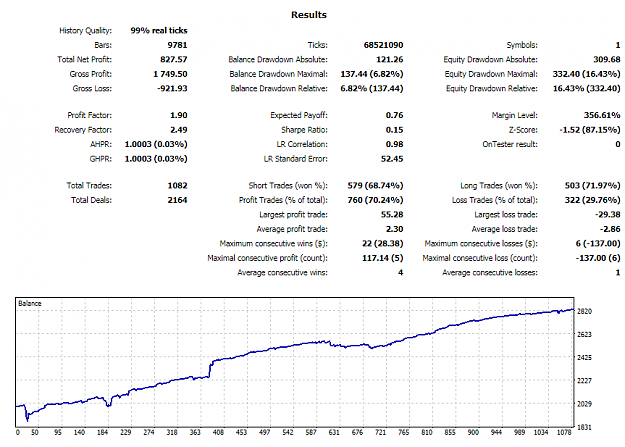

I just implemented the strategy described in Post 1 in MQL5 and did a backtest based on real ticks from 2017-01-01 until 2018-07-30 on GBPUSD,H1 starting with 2000 USD capital:

Attached Image (click to enlarge)

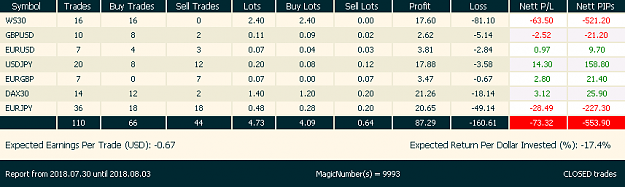

I observed that the big losses are mostly due to days that price moves in one direction. We may get better results if we can filter those days.

I just implemented the strategy described in Post 1 in MQL5 and did a backtest based on real ticks from 2017-01-01 until 2018-07-30 on GBPUSD,H1 starting with 2000 USD capital: {image} I observed that the big losses are mostly due to days that price trends in one direction. We may get better results if we can filter those days.

Ignored

So you took every trade (on every new high/low), no minimum ATR band level or something else?

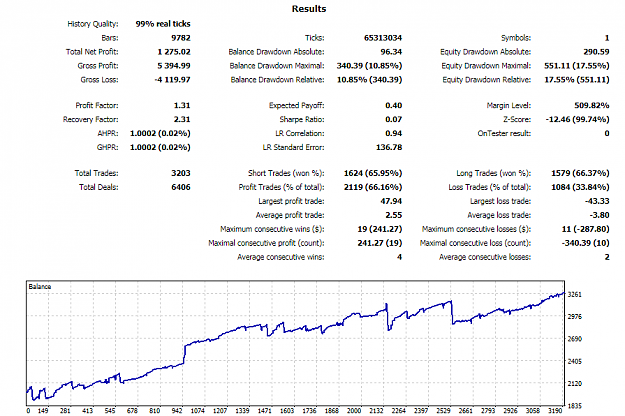

I try to limit the losses with the hard stop at ATR band level 6 and only take trades in the H4 EMA direction with my 2nd method (magic nr. 9990) for example.

Last week (2018.07.30 - 2018.08.03) wasn't a good week for this method in general, we often had such situations where price trends in one direction the whole day. Therefore the original method from post 1 had its first red week. With my method I got still a good green week (because of Dow)!

9990 = my variant of SMR with 4H MA filter, BE stop, no fixed timed 25%/50% exits but "candlestick jumping stop loss" - see above for more details

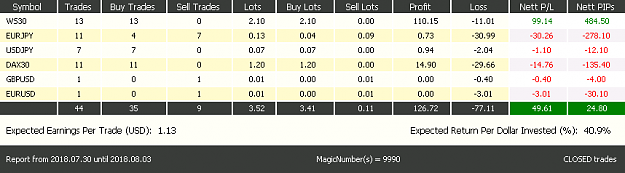

9993 = original method from post 1 with only BE stop added. _ EA trades the broker min lots per symbol (0.01 for forex symbols, 0.10 for dax/dow) with some small kind of martingale (0.01 for first 3 trades, 0.02 for the next two trades and then 0.03 lots until MaxTradesPerSymbolAllowed is reached). Both variants open the first trade only when min level of the ATR band of 3 is reached and also have a hard stop if ATR band 6 is reached! The broker used has fixed spreads per symbol and charges no commissions per trade.

I just implemented the strategy described in Post 1 in MQL5 and did a backtest based on real ticks from 2017-01-01 until 2018-07-30 on GBPUSD,H1 starting with 2000 USD capital: {image} I observed that the big losses are mostly due to days that price trends in one direction. We may get better results if we can filter those days.

Ignored

nice work.

can you show backtest for EURUSD on the same period?

{quote} So you took every trade (on every new high/low), no minimum ATR band level or something else? I try to limit the losses with the hard stop at ATR band level 6 and only take trades in the H4 EMA direction with my 2nd method (magic nr. 9990) for example. Last week (2018.07.30 - 2018.08.03) wasn't a good week for this method in general, we often had such situations where price trends in one direction the whole day. Therefore the original method from post 1 had its first red week. With my method I got still a good green week (because of Dow)!...

Ignored

The EA opens a maximum number of trades based on fixed distance (100 points). I will test it with a percentage of the daily ATR value to see the results.

The idea of using ATR band levels plus a trend filter seems valid to me. Good work!

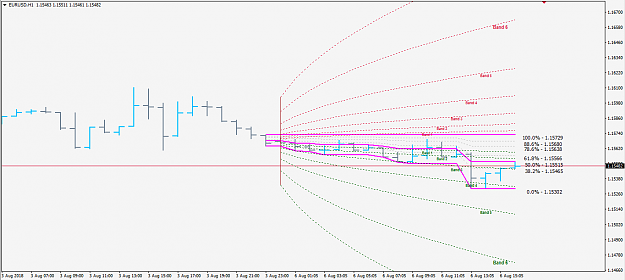

Just wondering if any trader here has found any advantage of using Alphaomegas Sqrt(t) formulas ? {image} Masterrmind.............

Ignored

Don't think that there's any edge per se. However, the variance of a (pseudo) random walk increases with the square root of the time. That is what i shows ... where you can expect to see prize after x candles on average ...

{quote} Don't think that there's any edge per se. However, the variance of a (pseudo) random walk increases with the square root of the time. That is what i shows ... where you can expect to see prize after x candles on average ...

Ignored

Perhaps we'll have to wait and see what other tests get posted here and the commentary that follows.

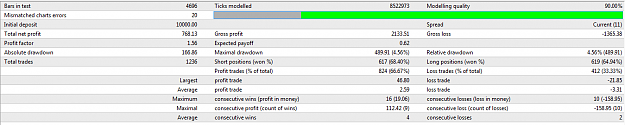

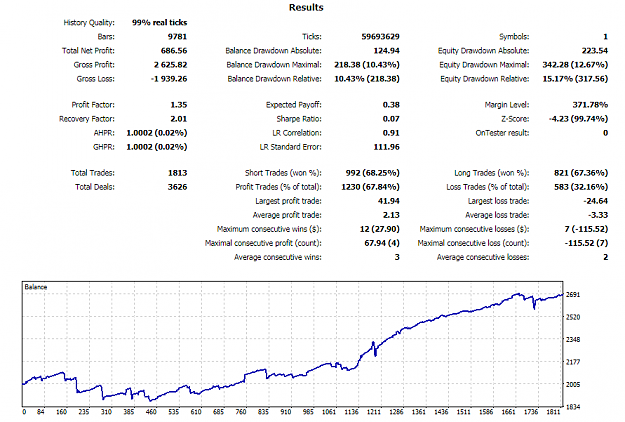

A backtest based on real ticks from 2017-01-01 until 2018-07-30 on EURGBP,H1 starting with 2000 USD capital: {image} As expected, the strategy seems to work a bit better on ranging currency pairs.

As suggested by alphaomega in Post 1, the EA closes all open positions at 25% and 50% retracement depending on the time of day (one cycle). I am going to make some modifications to the original strategy. In case of any improvement, I will post the results here.

{quote} take your profits quickly and hold on to your losses longer=mean reversion Avg losses always greater than avg profit=mean reversion Novice traders like mean reversion because of high win rate 60-90% Why? because its not a mental beating ie for the weak minded

Ignored

Perhaps some novice traders like mean reversion but they also might like martingale or trend trading or swing trading or any other type of trading.

Certainly do not recommend it as a standalone trading strategy.

Plenty of highly intelligent minds are parked in this space though.

Attached Image (click to enlarge)

You never know you just might learn something useful.

{quote} take your profits quickly and hold on to your losses longer=mean reversion Avg losses always greater than avg profit=mean reversion Novice traders like mean reversion because of high win rate 60-90% Why? because its not a mental beating ie for the weak minded

Ignored

what matters is not the win rate, or the average win/loss. what matters is the PNL

I certainly beleive that novice traders like to use tight stop losses; and be the broker's bitc*es