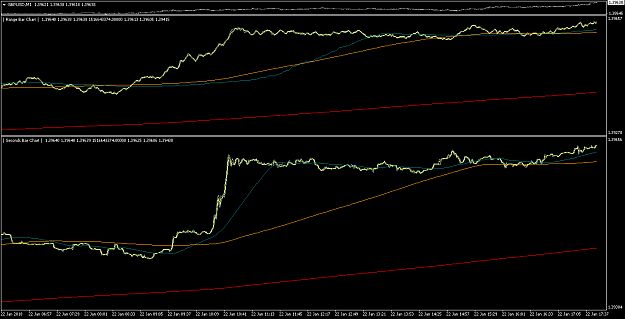

Just for the fun of it in MT4: I stretched the 1 min period (blue line) over the range bar chart, i.e. instead of continuous sampling there is now non-linear sampling based on actual bar time.

Staying with the "Greeks" perspective: assuming we wanted to derive Theta (time decay) to see the speed of "conversion to non-movement", this is obviously impossible with a range bar chart alone, but with the application of the above mentioned stretching we can possibly benefit from the smoother raw data without losing the dimension of time.

Assuming we use a very smooth Influx value as the derivative of price, we might be able to calculate some meaningful Greeks (=sensitivities to changes)...

Staying with the "Greeks" perspective: assuming we wanted to derive Theta (time decay) to see the speed of "conversion to non-movement", this is obviously impossible with a range bar chart alone, but with the application of the above mentioned stretching we can possibly benefit from the smoother raw data without losing the dimension of time.

Assuming we use a very smooth Influx value as the derivative of price, we might be able to calculate some meaningful Greeks (=sensitivities to changes)...

Attached Image (click to enlarge)

Augmenting Intelligence

2