Economic surprises drive EUR, GBP gains

Asian markets retreated while European equities and US stock index futures failed to sustain recent rebound, turning red on Wednesday. Dollar index rebounded after a dip to the February low of 89.70 amid renewed bearish pressure in risk assets.

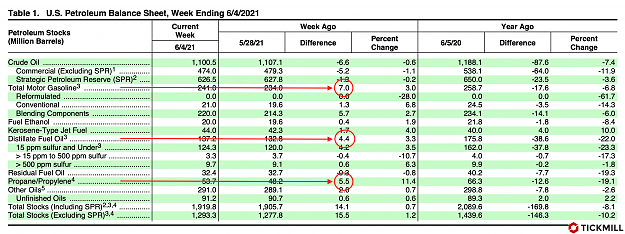

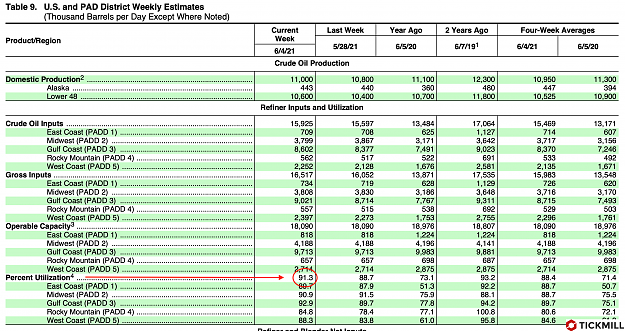

Oil has once again failed the task of gaining a foothold above the key resistance ($70 for Brent) and went down. In addition, a negative news background arrived in time - progress on the Iran deal and an unexpected increase in commercial oil reserves in the United States.

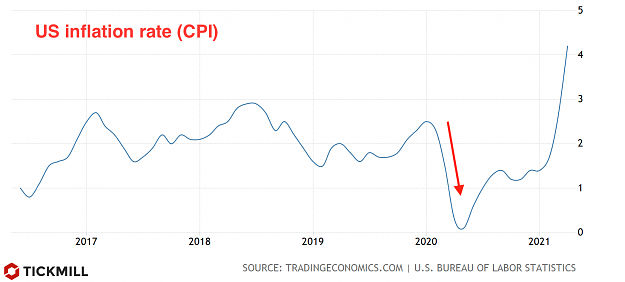

The UK inflation data showed that the economy could not escape the fate of other countries - production prices rose strongly amid signs of raw materials shortages and supply bottlenecks. The demand for inventories is rising at the fastest pace in years due to the overreaction of firms to consumer demand boom. Firms are trying to replenish inventories with some excess anticipating more shortage, which basically creates a self-reinforcing loop. Building pressures in producer prices are expected to eventually find way to consumer prices, so pressure on central banks stemming from economic data will likely remain on the rise.

Inflation of retail goods in Britain beat forecast, which is expected to prompt the Bank of England to be among the first to use more aggressive rhetoric. Despite USD bouncing off February lows and adding pressure on the Pound, the British currency appears to be targeting highs of 2021, and then of April 2018 thanks to strong fundamental component (April employment + inflation) and the fact that the uptrend on the daily timeframe still has a large margin of movement - the price is below the median line of the bullish channel:

The European currency continues to stay strong in the pair with USD against the background of the weakening of the latter. The news flow related to easing of restrictions in European countries subdues risks for economic growth which pressures risk premium in EU equities and bonds. Since information of this kind on the US economy were priced in 1-2 months earlier, the equilibrium in expectations should have been restored when the Old World moved to the final phase of lifting lockdowns.

From a technical point of view, the picture for EURUSD is similar to GPBUSD - the peaks of 2021 and 2018 have yet to be overcome:

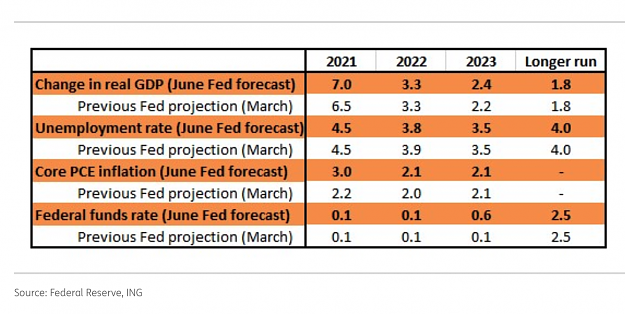

The Fed is to release the minutes of the April meeting today. The Central Bank has more or less definitely expressed its stance, but the markets do not really believe that the Fed will tolerate growing inflation risks. The content of the Minutes is expected to focus on the pledge to keep rates low, which could potentially have a moderately downside impact on the US currency. However, the risk of resumption of decline in the US markets is increasing, which may again provide unexpected support for the USD.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Asian markets retreated while European equities and US stock index futures failed to sustain recent rebound, turning red on Wednesday. Dollar index rebounded after a dip to the February low of 89.70 amid renewed bearish pressure in risk assets.

Oil has once again failed the task of gaining a foothold above the key resistance ($70 for Brent) and went down. In addition, a negative news background arrived in time - progress on the Iran deal and an unexpected increase in commercial oil reserves in the United States.

The UK inflation data showed that the economy could not escape the fate of other countries - production prices rose strongly amid signs of raw materials shortages and supply bottlenecks. The demand for inventories is rising at the fastest pace in years due to the overreaction of firms to consumer demand boom. Firms are trying to replenish inventories with some excess anticipating more shortage, which basically creates a self-reinforcing loop. Building pressures in producer prices are expected to eventually find way to consumer prices, so pressure on central banks stemming from economic data will likely remain on the rise.

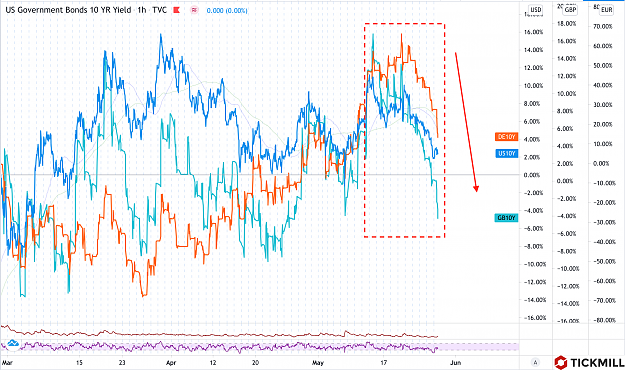

Inflation of retail goods in Britain beat forecast, which is expected to prompt the Bank of England to be among the first to use more aggressive rhetoric. Despite USD bouncing off February lows and adding pressure on the Pound, the British currency appears to be targeting highs of 2021, and then of April 2018 thanks to strong fundamental component (April employment + inflation) and the fact that the uptrend on the daily timeframe still has a large margin of movement - the price is below the median line of the bullish channel:

Attached Image (click to enlarge)

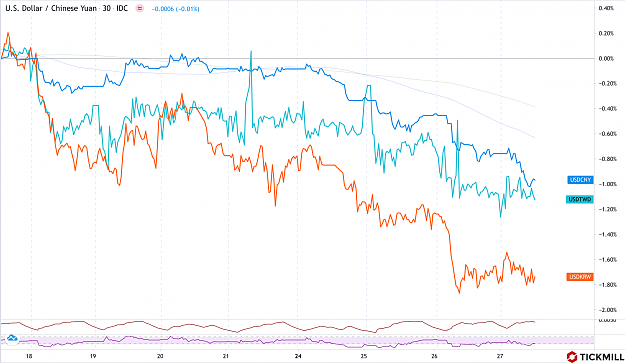

The European currency continues to stay strong in the pair with USD against the background of the weakening of the latter. The news flow related to easing of restrictions in European countries subdues risks for economic growth which pressures risk premium in EU equities and bonds. Since information of this kind on the US economy were priced in 1-2 months earlier, the equilibrium in expectations should have been restored when the Old World moved to the final phase of lifting lockdowns.

From a technical point of view, the picture for EURUSD is similar to GPBUSD - the peaks of 2021 and 2018 have yet to be overcome:

Attached Image (click to enlarge)

The Fed is to release the minutes of the April meeting today. The Central Bank has more or less definitely expressed its stance, but the markets do not really believe that the Fed will tolerate growing inflation risks. The content of the Minutes is expected to focus on the pledge to keep rates low, which could potentially have a moderately downside impact on the US currency. However, the risk of resumption of decline in the US markets is increasing, which may again provide unexpected support for the USD.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 75% and 72% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.