Are there quant basket traders out there? I need a hand from those of you who use quantitative methods to size and time the opening and the closing of their basket trades --as opposed to "I close when I feel happy with my profit"--

I'm not myself a basket trader. My motivation comes from the fact that I'm trying to develop a system that some times, mainly in the ranging periods, is equivalent or at least very similar to basket trading.

I tried to find if there is an optimal method to open and close a trade under the assumption that the instrument is mean reverting. I found a very complicated method trying to solve this "double stopping problem" (in the pdf). The solution is based on the subjective cost of staying in the market longer vs the expected increase of the reward. But the interest rates are low nowadays. It may be interesting for people using options, because of the time decay, but it doesn't seem to fit my needs.

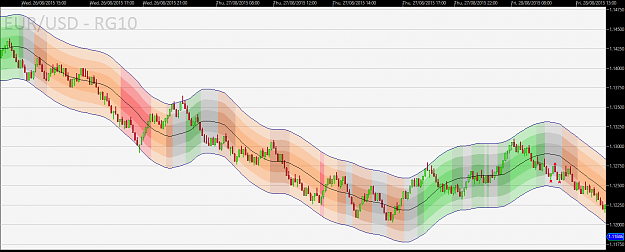

I also found a very simple method which consists in maintaining a lot size linearly proportional and opposite to the distance of the price to the mean measured in deviations. In short I add on my losers at every standard dev. A grid. But I don't get the rational behind this idea. Say the price is at the mean. I'm flat. It goes 1 SD below the mean. I open a lot long. It goes to the second SD below the mean. I add another 1 lot long. If the price returns at 1 SD shall I close one lot to keep the linear exposure?

In the case the price goes to the 3rd SD I've 3 positions open and a floating loss of (2+1+0=) 3 times the SD. I only get 3 SD if it returns straight to the mean but a 6 SD floating loss should it reach the 4th SD. At first it seems better to hold on and wait the price to come back to the mean and get a 6 SD profit. But since the price is wandering up and down before returning to the mean perhaps the method makes sense. If price goes -1, -2, -1, -2, -1, -2, -1, 0 the profit is 4 instead of 3. For sure I dislike the idea of adding on the losers while the price is going against my positions. Especially because I'm conscious the range won't last forever and I clearly don't want to add against a breakout. I checked the ranges don't last long enough to offset this loss.

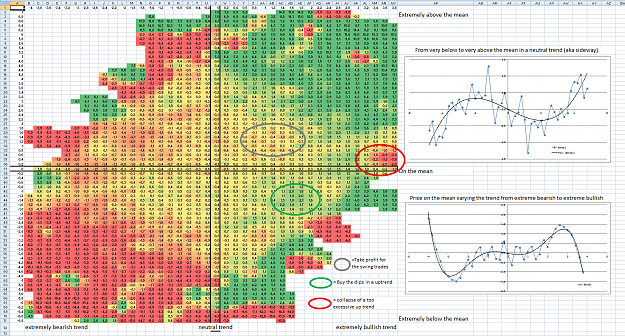

Because of the mean reversion assumption the probability of winning can't be used: per assumption/definition it is 100%! I kept thinking and found out that it would make sense to weight the exposure by the probability of being at a given level. I use a normal distribution to keep it simple. The most probable position of the price is on the mean. But it is the target level so no profit. The farther from the mean the more profit but also the less probability of being there. It is better to be more exposed when there is more potential. Let's multiply the potential profit (the distance in SD) by the probability N(x), N the normal distribution:

The exposure is maximal at 1 SD above or below the mean. Using the formula I scale out my losers. Sounds good in case of a breakout of the range. But I also scale out of the winners. And if the price ping-pongs between two levels I take a loss even if the price eventually reverts! Clearly not good. I feel like the exposure can't be solely based on the position of the price in the range.

How do you manage it?

I'm not myself a basket trader. My motivation comes from the fact that I'm trying to develop a system that some times, mainly in the ranging periods, is equivalent or at least very similar to basket trading.

I tried to find if there is an optimal method to open and close a trade under the assumption that the instrument is mean reverting. I found a very complicated method trying to solve this "double stopping problem" (in the pdf). The solution is based on the subjective cost of staying in the market longer vs the expected increase of the reward. But the interest rates are low nowadays. It may be interesting for people using options, because of the time decay, but it doesn't seem to fit my needs.

I also found a very simple method which consists in maintaining a lot size linearly proportional and opposite to the distance of the price to the mean measured in deviations. In short I add on my losers at every standard dev. A grid. But I don't get the rational behind this idea. Say the price is at the mean. I'm flat. It goes 1 SD below the mean. I open a lot long. It goes to the second SD below the mean. I add another 1 lot long. If the price returns at 1 SD shall I close one lot to keep the linear exposure?

In the case the price goes to the 3rd SD I've 3 positions open and a floating loss of (2+1+0=) 3 times the SD. I only get 3 SD if it returns straight to the mean but a 6 SD floating loss should it reach the 4th SD. At first it seems better to hold on and wait the price to come back to the mean and get a 6 SD profit. But since the price is wandering up and down before returning to the mean perhaps the method makes sense. If price goes -1, -2, -1, -2, -1, -2, -1, 0 the profit is 4 instead of 3. For sure I dislike the idea of adding on the losers while the price is going against my positions. Especially because I'm conscious the range won't last forever and I clearly don't want to add against a breakout. I checked the ranges don't last long enough to offset this loss.

Because of the mean reversion assumption the probability of winning can't be used: per assumption/definition it is 100%! I kept thinking and found out that it would make sense to weight the exposure by the probability of being at a given level. I use a normal distribution to keep it simple. The most probable position of the price is on the mean. But it is the target level so no profit. The farther from the mean the more profit but also the less probability of being there. It is better to be more exposed when there is more potential. Let's multiply the potential profit (the distance in SD) by the probability N(x), N the normal distribution:

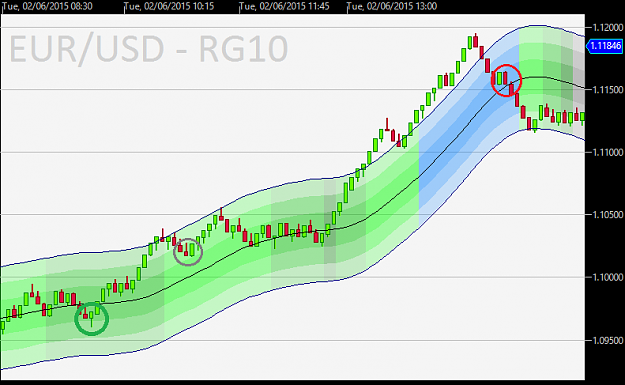

Attached Image

The exposure is maximal at 1 SD above or below the mean. Using the formula I scale out my losers. Sounds good in case of a breakout of the range. But I also scale out of the winners. And if the price ping-pongs between two levels I take a loss even if the price eventually reverts! Clearly not good. I feel like the exposure can't be solely based on the position of the price in the range.

How do you manage it?

Attached File(s)

No greed. No fear. Just maths.