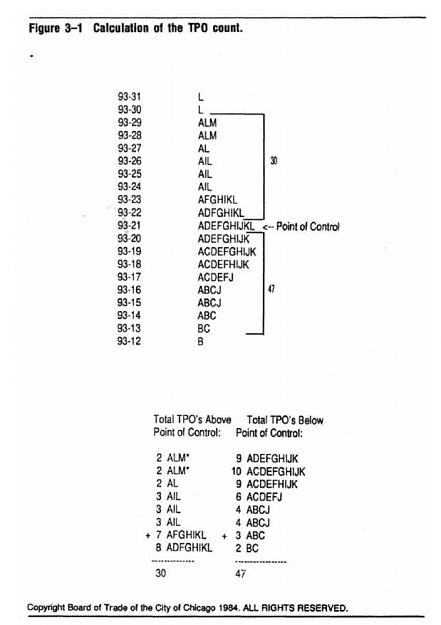

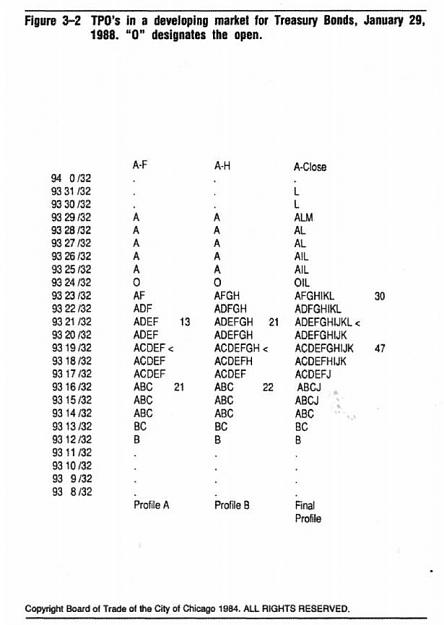

TPO Count The Time Price Opportunity is the smallest unit of market measurement. As mentioned earlier, TPO stands for Time, the market's regulator, and Price, the marker's advertiser, together creating the Opportunity to buy or sell at a given price at a particular time.

Monitoring the TPO count helps evaluate other timeframe control within the developing value area. Specifically, the TPO count measures the level of imbalance (when such an imbalance exists) between the other timeframe participant and the day timeframe (mostly local) trader.

The key to understanding how an imbalance can occur is to recognize that the other timeframe buyer does not deal directly with the other timeframe seller. Recall that the local, or scalper, acts as a middleman between these two longer-term participants. Thus, the other timeframe buyer generally buys from a local, and the other timeframe seller typically sells to a local. Imbalance occurs when there are more other timeframe buyers than sellers or more other timeframe sellers than buyers, leaving the local with an imbalance. Before we can learn how to measure this imbalance, we must first gain a better understanding of how the locals conduct their business.

The locals position themselves between the flow of outside buy orders and outside sell orders (orders placed predominantly by off-floor, other timeframe participants). For example, suppose that a floor broker receives an order to sell 100 contracts at, say, $5.00 per contract. The locals would buy the contracts from the broker and then turn around and sell them to another floor broker who has an order to buy 100 contracts at $5.02. In this situation, the locals perform their role of facilitating trade and, in return, receive a small margin of profit.

The trade facilitation process is seldom so ideal, however. Often there are more other timeframe buyers than sellers—causing the local's inventory to become overloaded. For example, if an usually large number of sell orders enter the pit, the local's inventory begins to accumulate to a point where he gets "too long." In other words, the local has purchased too much from the other timeframe seller. If the other timeframe buyer does not appear relatively quickly, the local must bring his inventory back into balance in some other way. One's first thought would be that the local simply needs to sell off his excess inventory. However, this is not so easy, for reversing and selling would only serve to accentuate the selling that is already flowing into the market. Therefore, his first priority is to stop the flow of outside sell orders by dropping his bid in hopes that the market will stabilize and he can balance his inventory. If lower prices do not cut off selling, the local may then be forced to "Jump on the bandwagon" and sell (liquidate) his longs at a lower price.

Viewed from another perspective, suppose you decided to try to make extra spending money by scalping football tickets. A month before the chosen game you purchased twenty tickets from the box office at $10 each. In this case, the box office is the other timeframe seller and you are the day timeframe buyer. Over the ensuing month, your team loses every game and slips from first to fifth place. Not surprisingly, the attendance is dismal on the day of the game at which you intend to sell your tickets. Few other timeframe buyers (fans) show up. In order to get rid of your inventory and recover at least part of your costs, you are forced to sell your tickets at $8 instead of $12 or $15. In this example, there were more other timeframe seller than buyers. Consequently, price had to move lower to restore balance.

The same concepts apply to the futures marketplace. If we can identify imbalance before it corrects itself, then perhaps we can capitalize on it, too. Tails and range extension are more obvious forms of other timeframe presence, but on a volatile or choppy day, much of the imbalance occurs in more subtle ways within the value area.

The TPO count is an excellent method for evaluating day-to-day imbalance that occurs within the developing value area.

Monitoring the TPO count helps evaluate other timeframe control within the developing value area. Specifically, the TPO count measures the level of imbalance (when such an imbalance exists) between the other timeframe participant and the day timeframe (mostly local) trader.

The key to understanding how an imbalance can occur is to recognize that the other timeframe buyer does not deal directly with the other timeframe seller. Recall that the local, or scalper, acts as a middleman between these two longer-term participants. Thus, the other timeframe buyer generally buys from a local, and the other timeframe seller typically sells to a local. Imbalance occurs when there are more other timeframe buyers than sellers or more other timeframe sellers than buyers, leaving the local with an imbalance. Before we can learn how to measure this imbalance, we must first gain a better understanding of how the locals conduct their business.

The locals position themselves between the flow of outside buy orders and outside sell orders (orders placed predominantly by off-floor, other timeframe participants). For example, suppose that a floor broker receives an order to sell 100 contracts at, say, $5.00 per contract. The locals would buy the contracts from the broker and then turn around and sell them to another floor broker who has an order to buy 100 contracts at $5.02. In this situation, the locals perform their role of facilitating trade and, in return, receive a small margin of profit.

The trade facilitation process is seldom so ideal, however. Often there are more other timeframe buyers than sellers—causing the local's inventory to become overloaded. For example, if an usually large number of sell orders enter the pit, the local's inventory begins to accumulate to a point where he gets "too long." In other words, the local has purchased too much from the other timeframe seller. If the other timeframe buyer does not appear relatively quickly, the local must bring his inventory back into balance in some other way. One's first thought would be that the local simply needs to sell off his excess inventory. However, this is not so easy, for reversing and selling would only serve to accentuate the selling that is already flowing into the market. Therefore, his first priority is to stop the flow of outside sell orders by dropping his bid in hopes that the market will stabilize and he can balance his inventory. If lower prices do not cut off selling, the local may then be forced to "Jump on the bandwagon" and sell (liquidate) his longs at a lower price.

Viewed from another perspective, suppose you decided to try to make extra spending money by scalping football tickets. A month before the chosen game you purchased twenty tickets from the box office at $10 each. In this case, the box office is the other timeframe seller and you are the day timeframe buyer. Over the ensuing month, your team loses every game and slips from first to fifth place. Not surprisingly, the attendance is dismal on the day of the game at which you intend to sell your tickets. Few other timeframe buyers (fans) show up. In order to get rid of your inventory and recover at least part of your costs, you are forced to sell your tickets at $8 instead of $12 or $15. In this example, there were more other timeframe seller than buyers. Consequently, price had to move lower to restore balance.

The same concepts apply to the futures marketplace. If we can identify imbalance before it corrects itself, then perhaps we can capitalize on it, too. Tails and range extension are more obvious forms of other timeframe presence, but on a volatile or choppy day, much of the imbalance occurs in more subtle ways within the value area.

The TPO count is an excellent method for evaluating day-to-day imbalance that occurs within the developing value area.

Markets are not efficient, rather they are effective - Jones