CBOE Volatility Indexes on US Equity Benchmarks (VIX, VXN, VXO, VXD, VIX3mo., RVX) and Put Call Ratio: signs of buy opportunity???

![]() ► By ... 0000-0001-5086-7401 & goo.gl/N8xLvv ◀

► By ... 0000-0001-5086-7401 & goo.gl/N8xLvv ◀![]()

☒ Aim of the post.

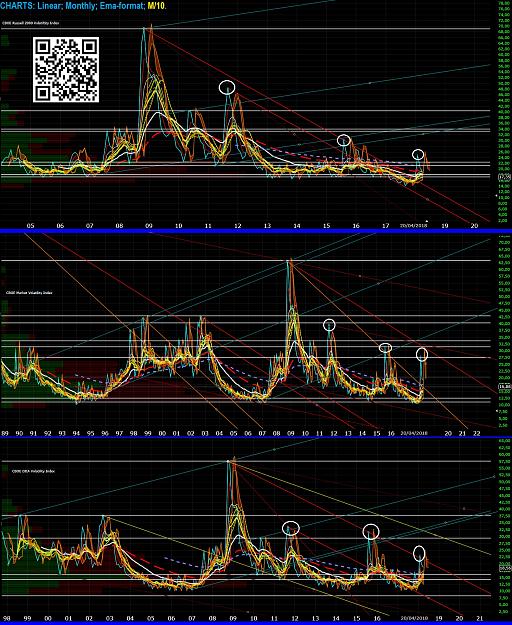

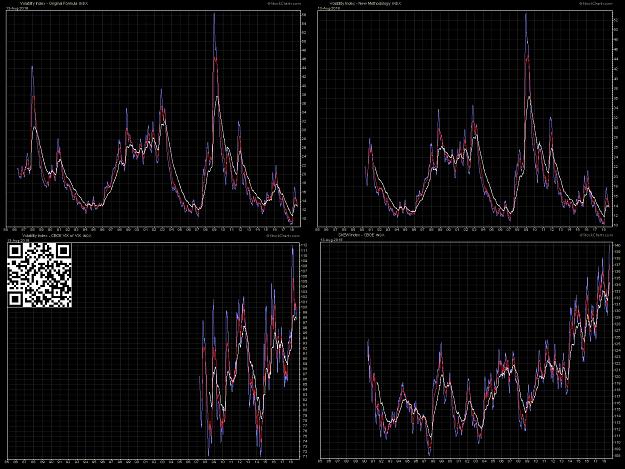

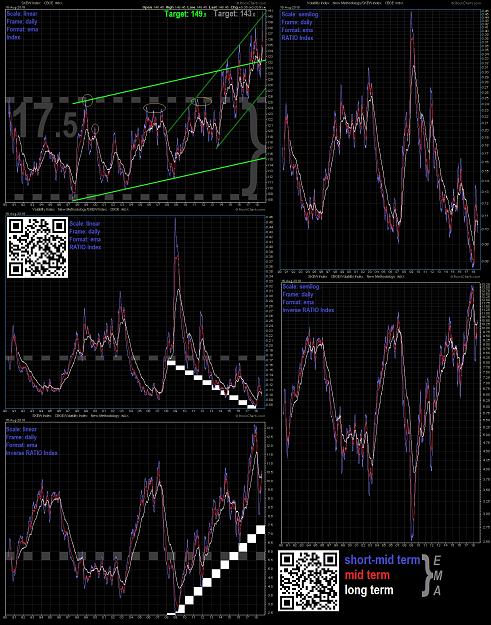

In this post there is a short up-date of the main CBOE volatility indexes based on US equity benchmarks, as S&P100 (VXO), S&P500 (VIX; VIX3m), Dow Jones (VXD), Nasdaq100 (VXN), Russell2k (RVX).

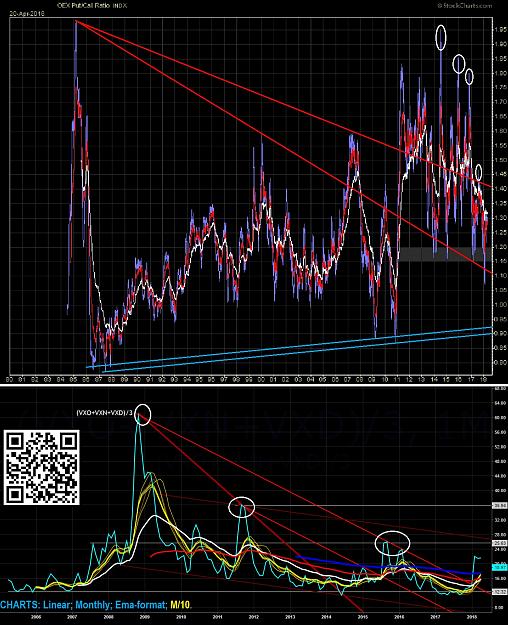

Graphical data obtained are used also with the average mash-up of VXO, VXN, VXD and also with the CBOE Put Call Ratio on S&P100.

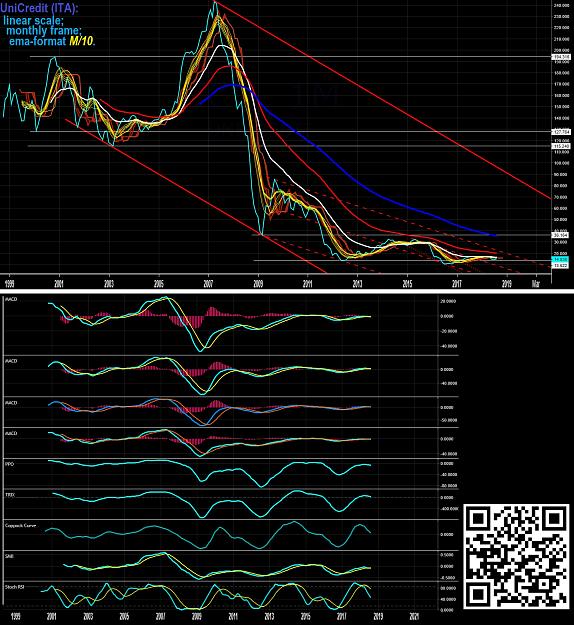

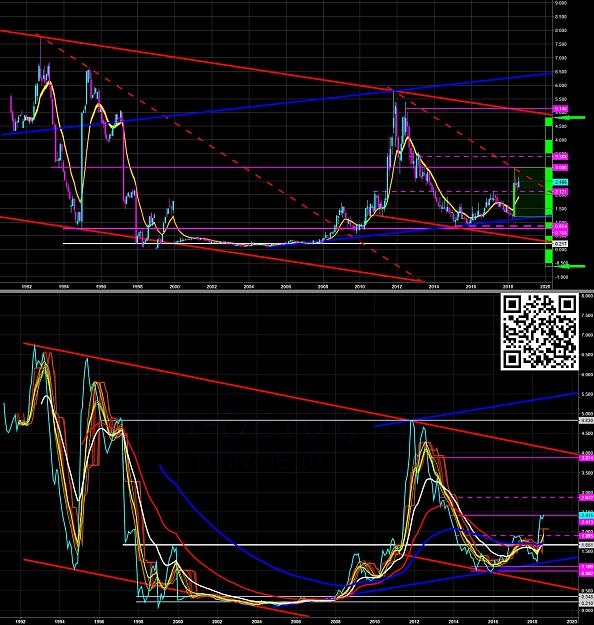

M/10 or Multiple 10mo. average, is a combination of the following yellow-orange lines: sma, ema, fwma,vwma,AL-ma, triangular-ma, Wilders-ma, Envelope-ema, Ichimoku Transformed}.

☒ Graphical Elements & Data.

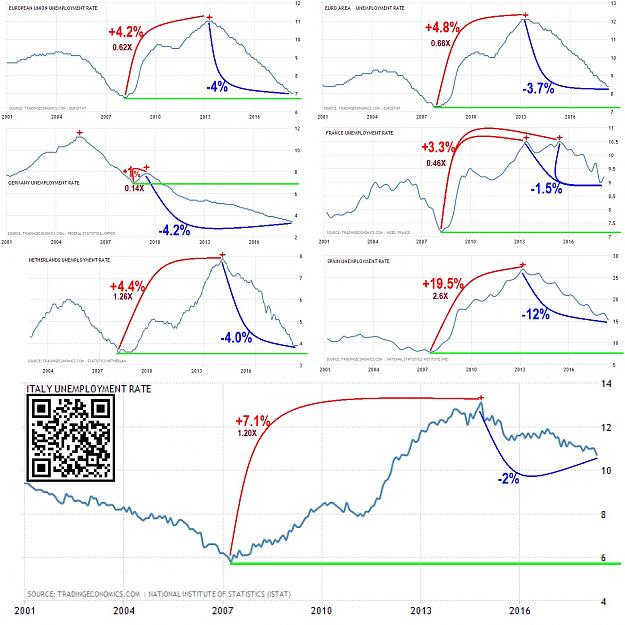

The key tops from 2008/2009 are in descending array.

The historical low is centered in 2017 for all volatility curves (except VXD), also for the averaged US curve.

Put Call Ratio shows a continuation-bear according to main volatility indexes.

Until now there are not signals of long-term reversal of the main trend.

The descending array of tops is an interesting buy signs on equity benchmarks, but only if volatility prices go below M/10.

☒ Chart sources.

❖ FreeStockCharts - StockCharts - TradingView.

☒ Sorry for my bad English. I hope that this post is at least minimally useful { Contact }.

Tuned on main trend, but follows short-medium term signs from underlying prices, for a correct & real-time set-up.

It is very important do not anticipate the main trend of the underlying financial instruments.

☻/♪ ❖ EARTH.pk, Alert 2.O !!! ❖

/▌

/|

I.M.O. by Sa!Vi ►►♡

#Ke'SaddhaPha'Pe'Kampa': #BundaBunda EMPIRE

Attached Image(s) (click to enlarge)