-

Records shatter as global stocks boom

A look at the day ahead in Asian markets. Investors in Asia could not be going into Friday's trading in more bullish spirits as the U.S.-led surge in mega tech fuels a global stock market boom, although there will be temptation to book some profit ahead of the weekend. Japan's Nikkei smashed its way to a new all-time high on Thursday after Nvidia's post-market surge following its fourth-quarter results, a path followed later in the day by Europe's Stoxx 600, the S&P 500 and the Dow Jones Industrials. The relentless rise around the world on Thursday, propelled by Nvidia's 16.5 per cent surge, should set the tone for ... (full story)

- Comments

- Subscribe

-

- Older Stories

From federalreserve.gov|Feb 22, 2024

From federalreserve.gov|Feb 22, 2024Thank you, Gianluca, and thank you for the opportunity to speak to you today.1 Let me begin by recognizing the Department of Economics at Princeton for its history of nurturing and supporting scholars in reaching their full potential. Some of the most important, transformative conversations I have had in my career have happened on this campus and with economists making significant contributions to the field. Let me start with the last time I was here. When I was a post doc at Stanford, I emailed Alan Krueger out of the blue and attached an early version of a new paper, asking him if he would meet with me for an hour to discuss it. Because of his experience with large data sets, and his curiosity, thoughtfulness, and generosity, one hour turned into three hours. And he brought along a new assistant professor, Dean Karlan. Not only did I learn a tremendous amount from Alan during that encounter, almost ten years later, I learned even more from him working as a senior economist at the Council of Economic Advisers when Alan was Chair. It is a great legacy of your department that you provided the conditions and support for Alan to make his seminal contributions to economics. I think similar conditions were in place at Princeton to allow Sir Arthur Lewis, the only person of African descent to receive the Nobel Prize in economics, to be productive and thrive. While I never met him, Sir Arthur has been an inspiration throughout my career, and I am grateful for his contribution that was aided by Princeton. The good work done here continues with the subject at hand today. The focus of this conference on macrofinance in the long run provides a good opportunity to reflect on what has changed and what has not changed since the onset of the pandemic four years ago. A feature of the past few years has been heightened uncertainty about how the economy would emerge from the turmoil of the pandemic and the subsequent recovery. I will talk about some types of uncertainty I see as having diminished recently and others that remain elevated. Then I will conclude with a discussion of my views on current monetary policy. post: Fed’s Cook: ‘I Would Like to Have Greater Confidence That Inflation’s Converging to 2% Before Beginning to Cut the Policy Rate’ Fed’s Cook: Disinflationary Process Has Been, and May Continue to Be, Bumpy and Uneven, as Highlighted by Last Week’s CPI & PPI post:

FED'S COOK: RESTRICTIVE MONETARY POLICY AND FAVORABLE SUPPLY DEVELOPMENTS HAVE PUT US IN GOOD POSITION TO ACHIEVE BOTH SIDES OF FOMC’S MANDATE. post: Fed’s Cook: Forecast of 12-Month PCE Inflation Converging to 2% Target Over Time Still Seems Reasonable as Baseline Outlook Fed’s Cook: Believe Our Current MonPol Stance is Restrictive post: FED'S COOK: I AM NOW WEIGHING THE POSSIBILITY OF EASING POLICY TOO SOON AND LETTING INFLATION STAY PERSISTENTLY HIGH VERSUS EASING POLICY TOO LATE AND CAUSING UNNECESSARY HARM TO THE ECONOMY.

FED'S COOK: RESTRICTIVE MONETARY POLICY AND FAVORABLE SUPPLY DEVELOPMENTS HAVE PUT US IN GOOD POSITION TO ACHIEVE BOTH SIDES OF FOMC’S MANDATE. post: Fed’s Cook: Forecast of 12-Month PCE Inflation Converging to 2% Target Over Time Still Seems Reasonable as Baseline Outlook Fed’s Cook: Believe Our Current MonPol Stance is Restrictive post: FED'S COOK: I AM NOW WEIGHING THE POSSIBILITY OF EASING POLICY TOO SOON AND LETTING INFLATION STAY PERSISTENTLY HIGH VERSUS EASING POLICY TOO LATE AND CAUSING UNNECESSARY HARM TO THE ECONOMY. From stats.govt.nz|Feb 22, 2024|1 comment

From stats.govt.nz|Feb 22, 2024|1 commentKey facts: For the December 2023 quarter compared with the September 2023 quarter, unless otherwise stated: • total volume of seasonally adjusted retail sales was $25 billion, ...

-

- Newer Stories

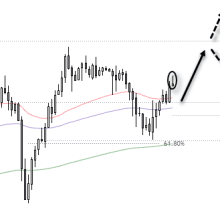

From cityindex.com|Feb 22, 2024

From cityindex.com|Feb 22, 2024The risk-on rally across on Thursday helped the ASX 200 extend its gains overnight. The 4-hour chart shows a strong rally from the 200-day EMA and 61.8% Fibonacci level, although ...

From bnnbloomberg.ca|Feb 22, 2024

From bnnbloomberg.ca|Feb 22, 2024Two top Federal Reserve officials hammered home the message Thursday that the US central bank is still on track to cut interest rates this year — just not anytime soon. Fed Vice ...

From federalreserve.gov|Feb 22, 2024|4 comments

From federalreserve.gov|Feb 22, 2024|4 commentsThank you, Dean Dunham and the University of St. Thomas for the opportunity to speak to you today. Given that this event is co-sponsored by the Notre Dame Club of Minnesota, and I taught at Notre Dame for 13 years, I will lead off with this thought: Go Irish! When I last spoke on January 16, the data we had received up to that point was very good—three- and six-month measures of core personal consumption expenditures (PCE) inflation were running right at 2 percent, which is our goal for total inflation, the labor market was cooling but still healthy, and real gross domestic product (GDP) was likewise growing but expected to moderate in the fourth quarter. I argued then that the data was "almost as good as it gets." And I argued that because the economy was doing so well, we could take our time and collect more data to ensure that inflation was on a sustainable 2 percent path. There was no rush to cut rates any time soon. Since then, we received data on fourth quarter GDP as well as January data on job growth and consumer product index (CPI) inflation. All three reports came in hotter than expected. GDP growth came in at 3.3 percent, well above forecasts. Jobs grew by 353,000, well over forecasts of less than 200,000, and monthly core CPI inflation came in at 0.4 percent, which was much higher than it had been for the previous six months. So, the data that we have received since my last speech has reinforced my view that we need to verify that the progress on inflation we saw in the last half of 2023 will continue and this means there is no rush to begin cutting interest rates to normalize monetary policy. Last week's report on consumer prices in January was a reminder that ongoing progress on inflation is not assured. The uptick in inflation in that report was spread widely among goods and services. This one month of data may have been driven by some odd seasonal factors or outsized increases in housing costs, or it may be a signal that inflation is stickier than we thought and will be harder to bring back down to our target. We just don't know yet. While I believe inflation is likely on track to reach 2 percent in a sustainable manner, I am going to need to see more data to sort out whether January's CPI inflation was more noise than signal. This means waiting longer before I have enough confidence that beginning to cut rates will keep us on a path to 2 percent inflation. post: Fed’s Waller: Data Received Since Last Speech on Jan 16 Has Reinforced My View We Need to Verify Inflation Progress From Last Half of 2023 Will Continue Fed’s Waller: This Means There’s No Rush to Begin Cutting Interest Rates post: Fed’s Waller: CPI Report Last Week is a Reminder That Ongoing Progress on Inflation’s Not Assured Waller: Need to See More Data to Know if January CPI Was ‘More Noise Than Signal’ Waller: Latest Data on Job Openings and Quits May Indicate Labor Mkt Moderation May Have Stalled post: Fed’s Waller: Cutting Too Soon Could Squander Inflation Progress and Risk Considerable Harm to Economy Fed’s Waller: Puzzled by Narrative That Delaying Cuts for a Meeting or Two Risks Causing a Recession Fed’s Waller: There Are No Indications of Imminent Recession post: Fed’s Waller: Recent Hotter-Than-Expected Data Validates Chair Powell’s ‘Careful Risk Management Approach’ Fed’s Waller: Still Expect to Ease Policy This Year Fed’s Waller: Several Indicators Suggest Some Slowing in Growth

- Story Stats

- Posted: Feb 22, 2024 5:46pm

- Submitted by:Category: Fundamental AnalysisComments: 0 / Views: 2,984