To learn how to swim , you first need to enter the water!

Similar Threads

Whats your best money management method? 52 replies

How to flow with the order flow? 26 replies

Money Management / Risk Management 24 replies

Money management model for multiple strategy trading method 16 replies

Most popular money management method. 7 replies

Money Flow Trading Method along with Risk Management

Money Flow Trading Method along with Risk Management

- #822

- Jan 4, 2017 2:29pm Jan 4, 2017 2:29pm

I'm having troubles transferring the pivots in Marketscope. There is a pivot indicator but it has the standard calculations, unlike Davit's pivots. Also there is no TDI indicator unfortunately which is a RSI+MA. The combined template looks difficult to understand and unnecessary. TDI is no needed if we use Awesome Oscillator.

I'll still study this aspect and update the situation.

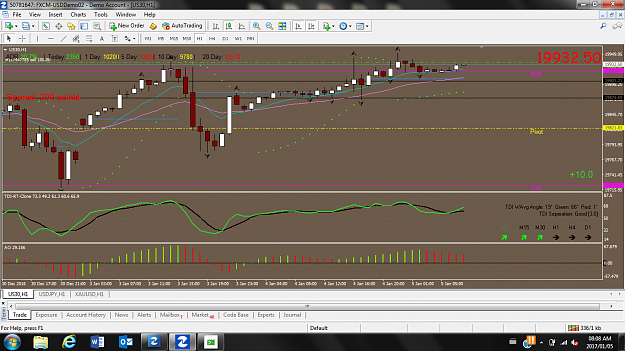

I'm long US30 as we speak. The FOMC spike up gave us room to short another batch now.

Regards

1

Disliked{quote} Of course USD is very strong at the moment in time. Look at both pairs USD/JPY and US30 on H4 and Daily TIME FRAMES. You will notice they both peaked near key resistance zone. USD/JPY is nowhere near that zone right now.Ignored

- #824

- Jan 4, 2017 2:44pm Jan 4, 2017 2:44pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

DislikedThere is two different directions last two days, so USD strong or weak? {image} {image}Ignored

NOTICE this time I did NOT use the words Demo Trading Account. There is a reason for that even though in FACT it is a FXCM UK $50,000 US Dollars Demo Trading Account.

From DAY one of your trading it visualize it as real funds and trade it not to lose money. In fact if you cannot earn at least 5% a month to show a Return on Investment of 5% a month for three consecutive months until March 31, 2017 while trading with NO REAL FEAR then trust me when I tell you that another business needs to be engaged in. Trading Forex is a BUSINESS and if you cannot make money in your business then do something else. If your business only has capital of $1000 US then the odds are that your business will fail.

I also just SHORTED another position of 100 units of SHORT USD/JPY and that is already in a small profit position as I am now using our Trade Plan number two.

This method works and after 13 years of my life learning it and using it and EARNING a Minimum of 10% each and every month that I trade then common sense and the facts make it so.

I doubt the Dow 30 will ever reach 20,000 unless MANIPULATED UP to make a point !!!

Benjaminis

1

- #827

- Jan 4, 2017 3:04pm Jan 4, 2017 3:04pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

WE see ADP tomorrow at 8:15 AM and The BIG BIG ONE FROM BLS on Friday , January 6, 2017 !!!

Do not put on many positions and try to be ALL in cash in both accounts. Real and Demo. Any comments or questions or good ideas ?

Please share them. This has been a very good learning day.

Benjaminis

Do not put on many positions and try to be ALL in cash in both accounts. Real and Demo. Any comments or questions or good ideas ?

Please share them. This has been a very good learning day.

Benjaminis

- #828

- Jan 4, 2017 3:21pm Jan 4, 2017 3:21pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

Disliked{quote} Benjamin, pls don't be angry. I'm not saying this method doesn't work, I'm just trying to understand it.Ignored

Just for the record one more time.

(1) 20% is of course the Forex Trader.

(2) 20% is Risk Management in case the Professional or Retail Forex Trader makes the wrong trading decision.

(3) 20% is the EDGE that lets you trade with the markets and NOT AGAINST them because the MARKETS WIN EVERY TIME !!! (MONEY FLOW)

(4) 20% is the Technical Indicators that I see clearly that you are skilled in.

(5) 20% is the Fundamental News released every day for everyone to see at the same time whether they are real or FAKE NEWS !!!

Notice how the two most common ones used by all Forex traders are Technical Indicators which includes Supply and Demand and Support and Resistance and Pivot Points or whatever system that has been developed in that field is number FOUR and Fundamentals is ranked number FIVE.

I think that this is the clearest explanation so far. For myself trading Forex is a way of life and I have the desire and love for it because it keeps me involved in the world and what is happening. I started this morning around 5:30 AM and here I am almost 11 hours later and ALL IS GOOD !!!

Benjaminis

1

- #829

- Jan 4, 2017 3:29pm Jan 4, 2017 3:29pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

DislikedSome of the followers also don't understand the method but pretend they do. wayfarer is going to sell dow and usdjpy, he's just doubling his risk due to the high correlation those. This is totally wrongIgnored

Your point is well taken however the Risk Management aspect covers that, along with the scaling in of the maximum 3 positions of any Trade Plan.

I think your Forex Trading results would improve because you have good technical knowledge. You also are quick on your feet. That is a compliment.

Thanks for your questions and your input and again Welcome Aboard as we head to "Paradise" in 2017, as long as we work hard.

Good Evening , I look forward to our next conversations !!!

Benjaminis

- #830

- Jan 4, 2017 7:16pm Jan 4, 2017 7:16pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

Disliked{quote} Our Number One Trade Plan is SHORT US 30 no more than 3 positions of 100 units each. That way on the absolute worst case scenario, the Risk is 6% of your Forex Trading Capital. NOTICE this time I did NOT use the words Demo Trading Account. There is a reason for that even though in FACT it is a FXCM UK $50,000 US Dollars Demo Trading Account. From DAY one of your trading it visualize it as real funds and trade it not to lose money. In fact if you cannot earn at least 5% a month to show a Return on Investment of 5% a month for three consecutive...Ignored

Written by Paul Brodsky. That is not however why I feel good. My USD/JPY SHORT was closed because I set my LIMIT OUT and I was not GREEDY !!

My profit is $634.19 US Dollars. It took less than 4 Hours. We all SEE where USD/JPY is now.

5 Minute Chart from Finviz for USD/JPY

http://finviz.com/forex_charts.ashx?t=USDJPY&tf=m5

Look at Gold now !!!

5 Minute Chart from Finviz for Gold.

http://finviz.com/futures_charts.ashx?t=GC&p=m5

I have a DRAW DOWN of $125 US Dollars on my SHORT US 30 of 100 Units or $100,000 US Dollars.

Benjaminis

1

- #831

- Edited 7:52pm Jan 4, 2017 7:39pm | Edited 7:52pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

http://www.zerohedge.com/news/2016-1...-dollar-stupid

by Tyler Durden

Dec 28, 2016 8:00 PM

Submitted by Paul Brodsky via Macro-Allocation.com,

We think the markets have it fundamentally wrong. US investors are anticipating a cyclical shift towards economic expansion via new tax incentives, business de-regulation and Keynesian government spending that promise to increase output, demand and asset prices. However, there is a far more influential driver of future asset prices – a structural shift that has begun but has yet to be acknowledged by economic and political authorities, and, judging by financial asset markets, by most investors. We expect weak equity markets and a strong treasury market beginning in 2017.

It’s the Dollar, Stupid.

The financial model used by advanced economies since 1971 is quickly losing its ability to support economic growth and rising asset prices.1 Western economic policy, which had previously relied heavily on credit creation from 1971 to 2008, was replaced in 2009 by monetary policy that relied heavily on base money creation through asset purchases. The structural shift in central bank focus from credit to monetary creation marked a paradigm shift in the decades-long finance-based economic model - from the leveraging phase to the de-leveraging phase.

The Fed shifted to relying on a communications policy in 2013, which focused on renewing the broad perception that by “normalizing” US interest rates the economy would again begin to react to credit incentives it could manage. It also emphasized the need for fiscal stimulus, which would ostensibly create demand and stimulate production growth. Last month the Fed hiked overnight rates for the second time in two years and the markets expect it to hike rate three times in 2017.

Fed rate hikes tighten credit conditions in the US and, given the continued execution of QE by other major global central banks, increase the exchange value of the dollar. A stronger dollar theoretically increases other economies’ exports into the US, provided that US consumers and businesses are able to maintain the same level of demand for foreign goods and services. This is an open question.

Donald Trump’s election raised hope that new tax incentives, business de-regulation and Keynesian government spending will create sufficient demand. The dollar and US financial markets have reacted in sympathy with stock prices rising and bond prices falling…despite the Fed’s renewed credit tightening. A strong dollar would tend to attract global wealth to the US, wealth that theoretically could find its way into US risk assets including US equities. Thus, US equity strength since the election reflects a strong dollar, which is based on the combination of Fed rate hikes and renewed hope for US government stimulus.

http://www.zerohedge.com/sites/defau...228_MAI1_0.jpg

This is not the first time the Fed has had to actively increase the exchange value of the dollar. Paul Volcker’s Fed had to hike overnight rates to 20% in 1980-81 so the dollar would be reaffirmed as a store of global value for US trading partners, including OPEC. We believe the Fed is doing the same today, in spite of its de-stimulative impact, because it wants to attract global capital to US banks and asset markets. Doing so would ensure USD hegemony, which would be necessary if/when global leverage leads to hyperinflation and multilateral trade and currency wars. Once substantial wealth is held in dollars and dollar-denominated assets, the US political dimension and the Fed, through the BIS and IMF, would be able to control the terms of a global monetary reset, which in turn would de-leverage balance sheets across currencies and economies in a controlled manner; in effect, a pre-packaged bankruptcy in real terms.

Nothing has changed structurally (or cyclically) since the US election. Global central banks are de-leveraging their banks through QE, with the exception of the Fed, which already did. Commercial bank liquidity and solvency is a precondition for a global monetary reset. The table is being set for more, not less, central bank intervention in the form of monetary inflation, and more intervention from the political dimension, which would choose which non-bank creditors (and debtors) will experience credit deflation.

The markets have it wrong

We believe fiscal measures like those being speculated about now in the US, even if successfully executed, would fail to generate meaningful new production and demand within the US and global economies. Financial markets are vulnerable to a reversal of their recent trends.

We cannot place specific figures or exact times when benchmark equity and fixed-income indexes will reverse current trends; however, we are increasingly confident that US and global economies have begun to experience necessary structural changes that directly impact: 1) incentives to produce and consume, 2) the fundamental manner in which the political dimension approaches monetary and fiscal policies, and 3) the way in which investors think about assets, liabilities, economics and capital markets.

The secular US fixed income bull market, which began in 1981 when the Fed embarked on what would become a forty five-year credit easing regime that benefitted, treasury, mortgage, corporate, municipal, small enterprise and consumer borrowers, and would eventually spread globally to other advanced and emerging bond markets; which allowed the US government to deficit-spend (eventually without the expectation of recourse) its way to unrivaled military might that defeated and then contained potential hostile threats abroad; which provided primary funding for bank and shadow bank lending that gave the US dollar and financial markets status as the ultimate sanctuary of global wealth; which provided a platform on which global bank and non-bank counterparties could swap contingent liabilities amounting to many times the size of underlying cash markets without fear of regulatory interference; and which provided speculators across other asset markets (including real estate) to continually sponsor unsustainable valuations, no longer produces capital or serves an economic purpose, and is almost over.

The secular US equity bull market, which not coincidentally also began in 1981 and served as the principal funding mechanism for great advances in digital technologies, communications, finance, logistics, health care, energy, retail, and other industries; which helped raise and maintain competitive trade advantages for the US and its allies; which expanded capital expenditures, productive output and consumer demand; which helped collateralize expansive public and private credit issuance and debt assumption, in turn creating a positive feedback loop that further increased nominal production, consumption and asset prices, and which created nominal wealth for US and non-US asset holders, is also in its evanescence.

Stock and bond markets in advanced, financially-oriented economies, have devolved more into political imperatives necessary to maintain social services and the perception of wealth, rather than serving as the traditional means to build and price wealth and capital. They no longer serve societies or global trade.

In over-leveraged economies, stock and bond markets become co-dependent. To sustain market prices, debt and equity require nominal output growth. To sustain market values, they require real output growth. The only way to increase nominal output growth and raise nominal equity prices in a highly leveraged economy with leveraged currency is to raise the quantity of credit, which must eventually reduce real output and asset values. The question before us is whether “eventually” is occurring now.

The primary reason we think stocks are peaking is scale. Aggregate market caps, valuations, revenues and earnings of public companies cannot be sustained by the level of real production in the underlying US and global economy. We think bonds are on the eve of reconciliation for the same basic reason: the scale of systemic leverage has already begun to reduce incentives to expand credit for capital formation, which, in turn, promotes debt deflation.

We expect debt deflation coincident with central bank monetary inflation, which would offset the deflation…on paper (like feet in the oven, head in the freezer producing a reasonable average). Before this occurs, we expect a financial or economic event that focuses public attention on the leverage problem.

Drilling Down

The incentive to invest in the stock market is to build wealth, which is accomplished by generating positive real (inflation-adjusted) returns. This presents a problem looking forward. Many of the companies the market rewards most in terms of market cap drive goods and service prices lower by innovating and connecting buyers and sellers (e.g. Amazon, Facebook).

Against this backdrop, the Fed’s economic mandate from Congress is to work towards stable prices and full employment. To do so, it has a specific annual inflation target of 2%. If the Fed is successful in this target, then it will reduce the purchasing power of US dollars by more than 64% over the next 25 years:

http://www.zerohedge.com/sites/defau...228_MAI2_0.jpg

As the table above makes clear, through its specific economic mandates and acceptance of the Fed’s 2% inflation target, the US Congress effectively promotes a decline in the value of ongoing savings earned and amassed by American labor. For investors, the policy also acts as a hurdle over which investor returns must rise to create positive real returns (i.e., wealth).

On one hand, commercial competition is naturally driving prices lower, making goods and services more economical for producers and consumers, and equity markets are inflating the asset values of businesses that deflate prices. On the other hand, the Fed is trying to drive goods, services and asset prices higher, which would drive the purchasing power value of savings lower.

http://www.zerohedge.com/sites/defau...228_MAI3_0.jpg

Since 1998, asset prices (portrayed by the Wilshire 5000 on the graph above) have been supported in great part by Fed liquidity and debt-driven buybacks while US economic activity, (portrayed by monetary velocity), has been in secular decline. It is tough to sustain 2% inflation for very long through financial maneuverings when domestic economic activity continues to weaken. Any further inflation the Fed might help create (as it hikes rates!?) will not be demand driven, but rather the result of more financial leverage.

It can’t persist much longer

The current excitement among US equity and credit investors over the promise of a best-case stimulative mix of deregulation, tax cuts, and Keynesian government spending has created a very optimistic market tone. The Fed has further intimated December’s rate hike was the start of a new regime of interest rate normalization. Together, these dynamics have caused treasury yields across the curve to rise. Rising treasury yields in past business cycles have further signaled economic recovery, which has seemed to confirm to most investors that economic and equity market optimism are warranted. We disagree.

Any fear of demand-driven goods and service inflation is un-warranted given 1) the already-leveraged nature of public and private sector balance sheets, 2) the need to perpetuate the relative strength of the dollar, and 3) the expectation of further Fed rate hikes. Even a successful multi-trillion dollar US government spending program that provides a few jobs and necessary American capital improvements could not provide sufficient consumer demand to overcome US and global balance sheet leverage and the attendant necessity to maintain US dollar strength to sustain the current monetary system.

The graph below plots the secular decline in long-duration treasuries against the year-over-year rate of US goods and service inflation. (The gap in 30-year treasuries is due to the elimination of Long Bond issuance from August 2001 to February 2006.) We believe the rise at the extreme right of the graph representing their most recent trends is not indicative of the next big move for long-duration treasuries.

http://www.zerohedge.com/sites/defau...228_MAI4_0.jpg

Given the need to maintain the US dollar as the fulcrum of the US monetary system, the most influential input for future treasury yields has become global output, which is in secular decline. This trend is logical, established and seems to be accelerating. It is logical because the secular post-War decline in global output growth was only interrupted by the emergence over the least twenty years of large new economies like the BRICs. The continuation of that secular downward trend would make sense once those emerging economies are established. The graphs below confirm that balance sheet leverage within emerging economies have surpassed those in developed economies and that, not surprisingly, global output growth is truly struggling. As a result, we expect one last spasm that takes long-term treasury yields to new lows.

http://www.zerohedge.com/sites/defau...228_MAI5_0.jpg

http://www.zerohedge.com/sites/defau...228_MAI6_0.jpg

Relevant Economics for Equity Investors

Investors will soon be forced to better understand the macro world around them. The perception of the deflation/inflation metric should determine near term and secular debt and equity market directions.

Prices are determined by supply/demand equilibriums – where the supply of goods, services, labor and assets meets the demand for each. This is theoretically true in classical economics. However, in the current flexible exchange rate monetary system administered by banking systems and the political dimension (i.e., a fiat regime), both supply and demand are determined by the prevailing quantity of credit available to producers of supply and the quantity of credit available to consumers who create demand. (Credit is simply a claim on base money, which is created by central banks.)

The most insipid structural problem threatening economic vitality and equity market returns is public and private sector leverage. High and rising debt-to-GDP ratios, which threaten economic liquidity, and high and rising debt-to-base money ratios, which threaten balance sheet solvency, must eventually be reconciled. Aging demographics within the world’s largest economies is accelerating the timing of the necessary reconciliation, which must occur through debt deflation, monetary inflation, or both.

Thus, investors seeking to create wealth by investing in broad equity markets face a fundamental structural problem caused by the irreconcilability of 1) naturally occurring commercial deflation, 2) economies and political systems that rely on inflation, and 3) the crowding out of consumption and investment by necessary debt service.

http://www.zerohedge.com/sites/defau...228_MAI7_0.jpg

Consider the 2% inflation target established by the Fed and accepted by most political economists. See table, page 4.) The target ostensibly limits the annual loss of purchasing power to 2%, and therefore it is generally thought that having such a target is in the best interest of American workers. Such an argument is inaccurate, nave and disingenuous. As the graph on the previous page shows, the Fed was unable to cap goods and service inflation when energy prices spiked from limited supply in the 1970s, and unable to cap inflation at 2% throughout the credit-led secular bull market in corporate and property equity in the 1980s, 1990s and 2000s.

Goods and service inflation more recently has struggled to rise to 1.7%, where it stands today. A 2% inflation target has shifted from a target to preserve the purchasing power of the dollar to a target to ruin it. Nowhere in the public discussion has this been mentioned. As discussed above, we think the Fed’s “fear of inflation”, which is ostensibly driving the new rate hike regime, is a necessary public narrative that will let the Fed pursue its true objective – a stronger dollar and deflation amid a contracting real economy.

Even if US domestic economic activity were to somehow reverse its secular downtrend enough to warrant current equity valuations, it is difficult to conceive how much more asset prices could rise – especially in real terms. Simple math, anachronistic economic policies and poor demographics pose insurmountable barriers for creating wealth through public share ownership. (We further discussed the current negative implications of over-valuation and the negatively convex nature of equity markets in The Grift.)

Can the Establishment really be that wrong?

In classic economics, both employment and inflation are derived from production. Political economists, a moniker that defines the academic discipline from which the great majority of contemporary economists spring, argue that a fully-employed labor force suggests that rising labor inflation will lead to rising goods and service inflation. Thus, the Fed is trying to raise rates currently, citing the second Fed mandate - full employment - which threatens stable prices. The ultimate policy goal is to protect the US (and global) economy from shrinking.

According to logic and classic economics, there is nothing wrong with a shrinking economy. Why? Because an economy should shrink commensurate with a rise in leisure time. Seriously. An economy is theoretically supposed to serve its factors of production. The more economical it is, the more leisure time it produces for its participants. (We suspect economies are called “economies” because they were formed naturally as systems that actually economized.)

In such an economy, only theoretical today, deflation would be a good thing because it would increase the purchasing power value of savings produced from past labor. In fact, an increase in deflation (i.e., an increase in declining prices) would actually raise real (inflation-adjusted) GDP because the gain in the dollar’s purchasing power from deflation would offset the declining volume of goods and services (nominal GDP). (We suspect this fundamental economic truth is the reason Congress’s mandate to the Fed includes only stable prices and employment, and not economic growth.)

The graph below shows the decline in the American work force since 2000. It should not strike you as alarming, given 1) all the great new innovations and technologies replacing human capital and 2) the expansion of global human capital from emerging economies. Tell us again, we ask sarcastically, what “full employment” is?

http://www.zerohedge.com/sites/defau...228_MAI8_0.jpg

Market cap-weighted indexes notwithstanding, it may be worthwhile here to ask yourself again why an increase in the majority of US equity shares is generally perceived as a given as the US economy becomes more efficient.

Why it is all about the Dollar Now?

In today’s global monetary system, currencies are tranched liabilities of: 1) commercial banks that create deposits through the lending process; 2) central banks on the hook to collateralize member commercial banks that create deposits and credit without commensurate reserves or circulated currency (base money), and; 3) treasury ministries that ask constituent factors of production to have faith that its taxing authority and, as has been demonstrated throughout history, its ability to wage war to loot enough resources outside its taxing domain to protect its currency’s purchasing power value.

As liabilities without directly-linked offsetting assets, the purchasing power value of currencies are always susceptible to dilution. Dilution comes in the form of credit issued by banks (and, potentially, non-bank lenders) that is either not collateralized by assets or collateralized by assets that themselves are liabilities (like Treasury notes). The wider the gap separating the amount of un-collateralized credit denominated in a currency from that currency’s base money (bank reserves and currency in float) – the ratio that determines monetary leverage - the greater the amount of future monetary de-leveraging will have to occur. (De-leveraging must ultimately occur so that debtors can service or repay their obligations and so producers have incentive to continue to supply goods and services in exchange for that currency.)

We expect global monetary authorities to protect the dollar as long as they can and we expect them to fail. Stocks and bonds will react violently; stocks and weak credits falling, treasuries prices rising (at first). That failure will lead to hyperinflation – not driven by demand, but rather by central bank money printing. A new global monetary understanding will then emerge.

We expect weak equities and a strong treasury market in 2017, as they begin to discount this fundamental structural shift.

Comments from Benjaminis: PLEASE READ THIS VERY VERY CAREFULLY. IT TELLS YOU THE MOST LIKELY SCENARIO THAT WILL UNFOLD IN THE NEXT SIX MONTHS !!! PLEASE GIVE ME YOUR OVERVIEW OF WHAT YOU READ. Thank you.

by Tyler Durden

Dec 28, 2016 8:00 PM

Submitted by Paul Brodsky via Macro-Allocation.com,

We think the markets have it fundamentally wrong. US investors are anticipating a cyclical shift towards economic expansion via new tax incentives, business de-regulation and Keynesian government spending that promise to increase output, demand and asset prices. However, there is a far more influential driver of future asset prices – a structural shift that has begun but has yet to be acknowledged by economic and political authorities, and, judging by financial asset markets, by most investors. We expect weak equity markets and a strong treasury market beginning in 2017.

It’s the Dollar, Stupid.

The financial model used by advanced economies since 1971 is quickly losing its ability to support economic growth and rising asset prices.1 Western economic policy, which had previously relied heavily on credit creation from 1971 to 2008, was replaced in 2009 by monetary policy that relied heavily on base money creation through asset purchases. The structural shift in central bank focus from credit to monetary creation marked a paradigm shift in the decades-long finance-based economic model - from the leveraging phase to the de-leveraging phase.

The Fed shifted to relying on a communications policy in 2013, which focused on renewing the broad perception that by “normalizing” US interest rates the economy would again begin to react to credit incentives it could manage. It also emphasized the need for fiscal stimulus, which would ostensibly create demand and stimulate production growth. Last month the Fed hiked overnight rates for the second time in two years and the markets expect it to hike rate three times in 2017.

Fed rate hikes tighten credit conditions in the US and, given the continued execution of QE by other major global central banks, increase the exchange value of the dollar. A stronger dollar theoretically increases other economies’ exports into the US, provided that US consumers and businesses are able to maintain the same level of demand for foreign goods and services. This is an open question.

Donald Trump’s election raised hope that new tax incentives, business de-regulation and Keynesian government spending will create sufficient demand. The dollar and US financial markets have reacted in sympathy with stock prices rising and bond prices falling…despite the Fed’s renewed credit tightening. A strong dollar would tend to attract global wealth to the US, wealth that theoretically could find its way into US risk assets including US equities. Thus, US equity strength since the election reflects a strong dollar, which is based on the combination of Fed rate hikes and renewed hope for US government stimulus.

http://www.zerohedge.com/sites/defau...228_MAI1_0.jpg

This is not the first time the Fed has had to actively increase the exchange value of the dollar. Paul Volcker’s Fed had to hike overnight rates to 20% in 1980-81 so the dollar would be reaffirmed as a store of global value for US trading partners, including OPEC. We believe the Fed is doing the same today, in spite of its de-stimulative impact, because it wants to attract global capital to US banks and asset markets. Doing so would ensure USD hegemony, which would be necessary if/when global leverage leads to hyperinflation and multilateral trade and currency wars. Once substantial wealth is held in dollars and dollar-denominated assets, the US political dimension and the Fed, through the BIS and IMF, would be able to control the terms of a global monetary reset, which in turn would de-leverage balance sheets across currencies and economies in a controlled manner; in effect, a pre-packaged bankruptcy in real terms.

Nothing has changed structurally (or cyclically) since the US election. Global central banks are de-leveraging their banks through QE, with the exception of the Fed, which already did. Commercial bank liquidity and solvency is a precondition for a global monetary reset. The table is being set for more, not less, central bank intervention in the form of monetary inflation, and more intervention from the political dimension, which would choose which non-bank creditors (and debtors) will experience credit deflation.

The markets have it wrong

We believe fiscal measures like those being speculated about now in the US, even if successfully executed, would fail to generate meaningful new production and demand within the US and global economies. Financial markets are vulnerable to a reversal of their recent trends.

We cannot place specific figures or exact times when benchmark equity and fixed-income indexes will reverse current trends; however, we are increasingly confident that US and global economies have begun to experience necessary structural changes that directly impact: 1) incentives to produce and consume, 2) the fundamental manner in which the political dimension approaches monetary and fiscal policies, and 3) the way in which investors think about assets, liabilities, economics and capital markets.

The secular US fixed income bull market, which began in 1981 when the Fed embarked on what would become a forty five-year credit easing regime that benefitted, treasury, mortgage, corporate, municipal, small enterprise and consumer borrowers, and would eventually spread globally to other advanced and emerging bond markets; which allowed the US government to deficit-spend (eventually without the expectation of recourse) its way to unrivaled military might that defeated and then contained potential hostile threats abroad; which provided primary funding for bank and shadow bank lending that gave the US dollar and financial markets status as the ultimate sanctuary of global wealth; which provided a platform on which global bank and non-bank counterparties could swap contingent liabilities amounting to many times the size of underlying cash markets without fear of regulatory interference; and which provided speculators across other asset markets (including real estate) to continually sponsor unsustainable valuations, no longer produces capital or serves an economic purpose, and is almost over.

The secular US equity bull market, which not coincidentally also began in 1981 and served as the principal funding mechanism for great advances in digital technologies, communications, finance, logistics, health care, energy, retail, and other industries; which helped raise and maintain competitive trade advantages for the US and its allies; which expanded capital expenditures, productive output and consumer demand; which helped collateralize expansive public and private credit issuance and debt assumption, in turn creating a positive feedback loop that further increased nominal production, consumption and asset prices, and which created nominal wealth for US and non-US asset holders, is also in its evanescence.

Stock and bond markets in advanced, financially-oriented economies, have devolved more into political imperatives necessary to maintain social services and the perception of wealth, rather than serving as the traditional means to build and price wealth and capital. They no longer serve societies or global trade.

In over-leveraged economies, stock and bond markets become co-dependent. To sustain market prices, debt and equity require nominal output growth. To sustain market values, they require real output growth. The only way to increase nominal output growth and raise nominal equity prices in a highly leveraged economy with leveraged currency is to raise the quantity of credit, which must eventually reduce real output and asset values. The question before us is whether “eventually” is occurring now.

The primary reason we think stocks are peaking is scale. Aggregate market caps, valuations, revenues and earnings of public companies cannot be sustained by the level of real production in the underlying US and global economy. We think bonds are on the eve of reconciliation for the same basic reason: the scale of systemic leverage has already begun to reduce incentives to expand credit for capital formation, which, in turn, promotes debt deflation.

We expect debt deflation coincident with central bank monetary inflation, which would offset the deflation…on paper (like feet in the oven, head in the freezer producing a reasonable average). Before this occurs, we expect a financial or economic event that focuses public attention on the leverage problem.

Drilling Down

The incentive to invest in the stock market is to build wealth, which is accomplished by generating positive real (inflation-adjusted) returns. This presents a problem looking forward. Many of the companies the market rewards most in terms of market cap drive goods and service prices lower by innovating and connecting buyers and sellers (e.g. Amazon, Facebook).

Against this backdrop, the Fed’s economic mandate from Congress is to work towards stable prices and full employment. To do so, it has a specific annual inflation target of 2%. If the Fed is successful in this target, then it will reduce the purchasing power of US dollars by more than 64% over the next 25 years:

http://www.zerohedge.com/sites/defau...228_MAI2_0.jpg

As the table above makes clear, through its specific economic mandates and acceptance of the Fed’s 2% inflation target, the US Congress effectively promotes a decline in the value of ongoing savings earned and amassed by American labor. For investors, the policy also acts as a hurdle over which investor returns must rise to create positive real returns (i.e., wealth).

On one hand, commercial competition is naturally driving prices lower, making goods and services more economical for producers and consumers, and equity markets are inflating the asset values of businesses that deflate prices. On the other hand, the Fed is trying to drive goods, services and asset prices higher, which would drive the purchasing power value of savings lower.

http://www.zerohedge.com/sites/defau...228_MAI3_0.jpg

Since 1998, asset prices (portrayed by the Wilshire 5000 on the graph above) have been supported in great part by Fed liquidity and debt-driven buybacks while US economic activity, (portrayed by monetary velocity), has been in secular decline. It is tough to sustain 2% inflation for very long through financial maneuverings when domestic economic activity continues to weaken. Any further inflation the Fed might help create (as it hikes rates!?) will not be demand driven, but rather the result of more financial leverage.

It can’t persist much longer

The current excitement among US equity and credit investors over the promise of a best-case stimulative mix of deregulation, tax cuts, and Keynesian government spending has created a very optimistic market tone. The Fed has further intimated December’s rate hike was the start of a new regime of interest rate normalization. Together, these dynamics have caused treasury yields across the curve to rise. Rising treasury yields in past business cycles have further signaled economic recovery, which has seemed to confirm to most investors that economic and equity market optimism are warranted. We disagree.

Any fear of demand-driven goods and service inflation is un-warranted given 1) the already-leveraged nature of public and private sector balance sheets, 2) the need to perpetuate the relative strength of the dollar, and 3) the expectation of further Fed rate hikes. Even a successful multi-trillion dollar US government spending program that provides a few jobs and necessary American capital improvements could not provide sufficient consumer demand to overcome US and global balance sheet leverage and the attendant necessity to maintain US dollar strength to sustain the current monetary system.

The graph below plots the secular decline in long-duration treasuries against the year-over-year rate of US goods and service inflation. (The gap in 30-year treasuries is due to the elimination of Long Bond issuance from August 2001 to February 2006.) We believe the rise at the extreme right of the graph representing their most recent trends is not indicative of the next big move for long-duration treasuries.

http://www.zerohedge.com/sites/defau...228_MAI4_0.jpg

Given the need to maintain the US dollar as the fulcrum of the US monetary system, the most influential input for future treasury yields has become global output, which is in secular decline. This trend is logical, established and seems to be accelerating. It is logical because the secular post-War decline in global output growth was only interrupted by the emergence over the least twenty years of large new economies like the BRICs. The continuation of that secular downward trend would make sense once those emerging economies are established. The graphs below confirm that balance sheet leverage within emerging economies have surpassed those in developed economies and that, not surprisingly, global output growth is truly struggling. As a result, we expect one last spasm that takes long-term treasury yields to new lows.

http://www.zerohedge.com/sites/defau...228_MAI5_0.jpg

http://www.zerohedge.com/sites/defau...228_MAI6_0.jpg

Relevant Economics for Equity Investors

Investors will soon be forced to better understand the macro world around them. The perception of the deflation/inflation metric should determine near term and secular debt and equity market directions.

Prices are determined by supply/demand equilibriums – where the supply of goods, services, labor and assets meets the demand for each. This is theoretically true in classical economics. However, in the current flexible exchange rate monetary system administered by banking systems and the political dimension (i.e., a fiat regime), both supply and demand are determined by the prevailing quantity of credit available to producers of supply and the quantity of credit available to consumers who create demand. (Credit is simply a claim on base money, which is created by central banks.)

The most insipid structural problem threatening economic vitality and equity market returns is public and private sector leverage. High and rising debt-to-GDP ratios, which threaten economic liquidity, and high and rising debt-to-base money ratios, which threaten balance sheet solvency, must eventually be reconciled. Aging demographics within the world’s largest economies is accelerating the timing of the necessary reconciliation, which must occur through debt deflation, monetary inflation, or both.

Thus, investors seeking to create wealth by investing in broad equity markets face a fundamental structural problem caused by the irreconcilability of 1) naturally occurring commercial deflation, 2) economies and political systems that rely on inflation, and 3) the crowding out of consumption and investment by necessary debt service.

http://www.zerohedge.com/sites/defau...228_MAI7_0.jpg

Consider the 2% inflation target established by the Fed and accepted by most political economists. See table, page 4.) The target ostensibly limits the annual loss of purchasing power to 2%, and therefore it is generally thought that having such a target is in the best interest of American workers. Such an argument is inaccurate, nave and disingenuous. As the graph on the previous page shows, the Fed was unable to cap goods and service inflation when energy prices spiked from limited supply in the 1970s, and unable to cap inflation at 2% throughout the credit-led secular bull market in corporate and property equity in the 1980s, 1990s and 2000s.

Goods and service inflation more recently has struggled to rise to 1.7%, where it stands today. A 2% inflation target has shifted from a target to preserve the purchasing power of the dollar to a target to ruin it. Nowhere in the public discussion has this been mentioned. As discussed above, we think the Fed’s “fear of inflation”, which is ostensibly driving the new rate hike regime, is a necessary public narrative that will let the Fed pursue its true objective – a stronger dollar and deflation amid a contracting real economy.

Even if US domestic economic activity were to somehow reverse its secular downtrend enough to warrant current equity valuations, it is difficult to conceive how much more asset prices could rise – especially in real terms. Simple math, anachronistic economic policies and poor demographics pose insurmountable barriers for creating wealth through public share ownership. (We further discussed the current negative implications of over-valuation and the negatively convex nature of equity markets in The Grift.)

Can the Establishment really be that wrong?

In classic economics, both employment and inflation are derived from production. Political economists, a moniker that defines the academic discipline from which the great majority of contemporary economists spring, argue that a fully-employed labor force suggests that rising labor inflation will lead to rising goods and service inflation. Thus, the Fed is trying to raise rates currently, citing the second Fed mandate - full employment - which threatens stable prices. The ultimate policy goal is to protect the US (and global) economy from shrinking.

According to logic and classic economics, there is nothing wrong with a shrinking economy. Why? Because an economy should shrink commensurate with a rise in leisure time. Seriously. An economy is theoretically supposed to serve its factors of production. The more economical it is, the more leisure time it produces for its participants. (We suspect economies are called “economies” because they were formed naturally as systems that actually economized.)

In such an economy, only theoretical today, deflation would be a good thing because it would increase the purchasing power value of savings produced from past labor. In fact, an increase in deflation (i.e., an increase in declining prices) would actually raise real (inflation-adjusted) GDP because the gain in the dollar’s purchasing power from deflation would offset the declining volume of goods and services (nominal GDP). (We suspect this fundamental economic truth is the reason Congress’s mandate to the Fed includes only stable prices and employment, and not economic growth.)

The graph below shows the decline in the American work force since 2000. It should not strike you as alarming, given 1) all the great new innovations and technologies replacing human capital and 2) the expansion of global human capital from emerging economies. Tell us again, we ask sarcastically, what “full employment” is?

http://www.zerohedge.com/sites/defau...228_MAI8_0.jpg

Market cap-weighted indexes notwithstanding, it may be worthwhile here to ask yourself again why an increase in the majority of US equity shares is generally perceived as a given as the US economy becomes more efficient.

Why it is all about the Dollar Now?

In today’s global monetary system, currencies are tranched liabilities of: 1) commercial banks that create deposits through the lending process; 2) central banks on the hook to collateralize member commercial banks that create deposits and credit without commensurate reserves or circulated currency (base money), and; 3) treasury ministries that ask constituent factors of production to have faith that its taxing authority and, as has been demonstrated throughout history, its ability to wage war to loot enough resources outside its taxing domain to protect its currency’s purchasing power value.

As liabilities without directly-linked offsetting assets, the purchasing power value of currencies are always susceptible to dilution. Dilution comes in the form of credit issued by banks (and, potentially, non-bank lenders) that is either not collateralized by assets or collateralized by assets that themselves are liabilities (like Treasury notes). The wider the gap separating the amount of un-collateralized credit denominated in a currency from that currency’s base money (bank reserves and currency in float) – the ratio that determines monetary leverage - the greater the amount of future monetary de-leveraging will have to occur. (De-leveraging must ultimately occur so that debtors can service or repay their obligations and so producers have incentive to continue to supply goods and services in exchange for that currency.)

We expect global monetary authorities to protect the dollar as long as they can and we expect them to fail. Stocks and bonds will react violently; stocks and weak credits falling, treasuries prices rising (at first). That failure will lead to hyperinflation – not driven by demand, but rather by central bank money printing. A new global monetary understanding will then emerge.

We expect weak equities and a strong treasury market in 2017, as they begin to discount this fundamental structural shift.

Comments from Benjaminis: PLEASE READ THIS VERY VERY CAREFULLY. IT TELLS YOU THE MOST LIKELY SCENARIO THAT WILL UNFOLD IN THE NEXT SIX MONTHS !!! PLEASE GIVE ME YOUR OVERVIEW OF WHAT YOU READ. Thank you.

- #832

- Jan 4, 2017 8:25pm Jan 4, 2017 8:25pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

5 Minute Futures Chart from Finviz on US 30

http://finviz.com/futures_charts.ashx?t=YM&p=m5

Benjaminis

http://finviz.com/futures_charts.ashx?t=YM&p=m5

Benjaminis

- #833

- Jan 4, 2017 9:08pm Jan 4, 2017 9:08pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

https://www.bullionstar.com/gold-uni...les-bank-china

People’s Bank of China

Introduction

Through it’s central bank, the People’s Republic of China holds the world’s 6th largest central bank gold holdings, with over 1800 tonnes of gold held in its official reserves of the People’s Bank of China. These gold reserves holdings are notable for having quadrupled since the early 2000s amid much secrecy. Since mid 2015, however, the Chinese government has embarked on a revised communication policy of releasing monthly updates on the size of its gold holdings. Although there is no official confirmation of gold storage arrangements, it is thought that the Chinese official gold reserves are vaulted in Beijing, China’s capital, and may be under the protection of the Chinese army.

Contents

People’s Bank of China

Introduction

Through it’s central bank, the People’s Republic of China holds the world’s 6th largest central bank gold holdings, with over 1800 tonnes of gold held in its official reserves of the People’s Bank of China. These gold reserves holdings are notable for having quadrupled since the early 2000s amid much secrecy. Since mid 2015, however, the Chinese government has embarked on a revised communication policy of releasing monthly updates on the size of its gold holdings. Although there is no official confirmation of gold storage arrangements, it is thought that the Chinese official gold reserves are vaulted in Beijing, China’s capital, and may be under the protection of the Chinese army.

Contents

- 1. Introduction

- 2. Ownership of Chinese Gold Reserves

- 3. PBoC – Accumulation of Gold Reserves

- 4. PBoC Gold Purchases on the International Market

- 5. PBoC Gold Storage

- 6. China’s Overall Reserve Assets

- 7. Reporting of PBoC Gold Reserves

- 8. Gold Transfers from other Chinese State entities

- 9. References and Links

Highlights

- China’s central bank, the People’s bank of China (PBoC), holds and manages China’s official monetary gold reserves. These gold reserves are now in excess of 1800 tonnes.

- The PBoC has pursued an active accumulation of monetary gold reserves since the early 2000s, but until 2015 did not provide regular updates on the extent of this accumulation policy.

- The PBoC quietly purchases gold on the international market and transports this gold back to China where it is said to be stored in vaults in Beijing, possibly under the protection of the Chinese army.

- Since China holds vast total foreign reserves in excess of US$ 3 trillion, China’s gold reserves, although substantial, only account for a relatively low 2% of total reserves.

Ownership of Chinese Gold Reserves

China’s official gold reserves are owned by the People’s Republic of China (PRC) and held and managed by the People’s Bank of China (PBoC). Although the PBoC was founded in 1948, it did not become the central bank of the People’s Republic of China (PRC) until 1983 when the PRC State Council granted the PBoC the functions of a central bank. The PBoC lists one of its responsibilities and tasks as:

“Holding and managing the state foreign exchange and gold reserves“[1]

PBoC – Accumulation of Gold Reserves

Chinese central bank gold reserves have more than quadrupled since the early 2000s, rising from approximately 400 tonnes in 2001 to over 1,800 tonnes today[2]. The actual accumulation pattern of this gold is hard to decipher. This is because from 2001 through to mid-2015, the PBoC only issued 4 public announcements in total addressing the size and growth of it’s gold reserves. These gold reserve increase announcements and their dates, are as follows:

- In Quarter 4 2001: From 394 to 500 tonnes

- In Quarter 4 2002: From 500 to 600 tonnes[3]

- In April 2009: From 600 to 1,054 tonnes[4]

- In July 2015: From 1,054 to 1,658 tonnes[5]

PBoC Gold Purchases on the International Market

In July 2015, when the PBoC announced the first update to its gold holdings since 2009, it also stated that the “major channels of accumulation” were from domestic gold production, secondary domestic scrap sources, purchases in foreign markets, and other transacting in the domestic market.

Beyond this general statement, neither the PBoC nor any other Chinese State entity comments on where the PBoC sources its gold purchases. On the surface, it would arguably be logical to assume that the PBoC buys gold on China’s main gold market, the Shanghai Gold Exchange (SGE)[6]. There are, however, many indications to suggest that the PBoC does not buy gold on the SGE. These indications include the following:

- Physical gold on the SGE is traded in Chinese Yuan. The PBoC has a preference to buy gold using US Dollars.

- The PBoC prefers to hold London Good Delivery (LGD) gold bars (400 oz or 12.5 kg bars). The SGE rarely trades LGD bars.

- The central bank sector, including the PBoC, has a motive to keep its gold purchases hidden so as not to cause market volatility. Gold bought on the PBoC is visible and shows up in the Exchange’s statistics.

- Central banks buy monetary gold or else buy non-monetary gold and monetize it, and do not have to report it through customs data channels. Gold imported into China for distribution on the SGE will show up in customs statistics of the supplying countries. Hence the PBoC would want to avoid this[7].

Additionally, anecdotal information from bullion banks and gold consultancies suggests that the PBoC purchases gold from counterparties on international wholesale markets using Chinese commercial banks such as ICBC and BoC as buying agents (proxies). These markets include the London Over-the-Counter (OTC) market using counterparties such as JP Morgan, and also South African and Swiss refinery counterparties. This would also suggest that Rand Refinery large gold bars and Swiss bar brands such as PAMP may be among the PBoC’s gold holdings.

According to the bullion banks and consultancy sources, the PBoC monetises its gold purchases into monetary gold prior to importing it into China. Since monetary gold crossing borders is exempt from disclosure, this approach would allow the PBoC to avoid reporting gold movements, for example from London to Beijing, through customs channels, thereby keeping Chinese central bank gold purchases ultra-secretive.

Between 2009 – 2010, the International Monetary Fund (IMF) sold 400 tonnes of gold in a series of on-market and off-market sales. The off-market sales were to a series of central banks including India and Bangladesh. At the time, China was said to be interested in purchasing some of the IMF gold, but it’s name failed to appear in the final off-market buyer list. The on-market sales, conducted from February to December 2010, were supposedly sales to the wider gold market. However, information about these on-market sales has remained classified and looks to have utilised the Bank for International Settlements (BIS) as selling agent. In this light, it’s distinctly possible that the IMF gold some of its gold to the PBoC in 2010, but that the transactions were hidden within the on-market sales process so as to prevent the identity of a Chinese state entity as buyer emerging. According to a China Gold Association (CGA) official at the time in 2010, a “purchase or even intent to do so [by China] would trigger market speculation and volatility“[8].

This view of the Chinese state not wanting to influence the gold market through its gold purchases was reiterated in a statement from the PBoC in July 2015 when it revealed an update to its gold holdings:

“On the basis of our assessment of the value of gold assets and our analysis of price changes, and on the premise of not creating disturbances in the market, we steadily accumulated gold reserves through a number of international and domestic channels.”[9]

PBoC Gold Storage

As with most things in the central bank gold market, information on the Chinese gold reserves is highly confidential, and the PBoC does not disclose where its official gold reserves are stored. One London source in the gold market has indicated that the Chinese official gold reserves are stored in vaults in Beijing. Another view stated that the gold reserves are under the control of the Chinese People’s Liberation Army (PLA)[10]. Therefore, the PBoC gold reserves may be stored in Beijing under the protection of the PLA. It’s notable that the headquarters of the PBoC is in Beijing, and not in China’s financial market capital, Shanghai.

China’s Overall Reserve Assets

Gold only represents a tiny fraction of China’s total holdings of foreign reserve assets. China holds over US$ 3 trillion in foreign reserve assets[11], predominantly as major foreign currency reserves. China’s reported gold holdings of approximately 1850 tonnes, although substantial, have a market value of approximately US $ 70 billion, which only comprises 2.3% of this US$ 3 trillion of total reserve assets. In comparison, Germany, France and Italy’s official gold holdings represent between 60 – 70% of those countries’ total reserve assets.

However, given that the PBoCs total reserves are so large, it would be difficult for the Chinese central bank to increase its gold reserves as a percentage of its total foreign reserves. As the PBoC stated in 2015[12]:

“Gold has a special risk-return characteristic, and at specific times is not a bad investment…But the capacity of the gold market is small compared with China’s foreign exchange reserves; if foreign exchange reserves were used to buy large amounts of gold in a short amount of time, it will easily affect the market.”

Therefore, either China’s gold holdings accumulation has a long way to go to even approach a meaningful level of diversification, or perhaps China has far larger official gold reserves than it reports and a level of gold holdings higher than 2% of total reserves.

Reporting of PBoC Gold Reserves

In mid 2015, when the PBoC announced that its official gold holdings had risen to 1,568 tonnes (53.32 million troy ounces) from the prior number of 1,054 tonnes (33.89 million troy ounces) reported in April 2009, the Chinese central bank also made a policy change to its gold reporting by announcing that going forward, it would release updates on the size of its official gold holdings on a monthly basis.

Monthly updates of the PBoC’s gold reserves are published on the State Administration of Foreign Exchange (SAFE) website in English under data category “Official Reserve Assets”[13]. The data for gold is only reported in US dollars and needs to be converted into ounces / tonnes using month-end US dollar gold prices. For example, at month-end November 2016, SAFE reported that China’s official gold reserves were valued at US$ 697.85 billion. At a November 2016 month-end gold price of US$ 1178.10 per troy ounce (LBMA Gold Price), China’s gold holdings equated to 59,235,209 ounces or 1842.5 tonnes. This is the same amount reported by China to the International Monetary Fund (IMF) and published on the IMF data website[14].

Gold Transfers from other Chinese State entities

All major parts of the Chinese gold market were established by and are owned by the Chinese state. As well as the PBoC, the State Administration of Foreign Exchange (SAFE) reports to a Communist Party of China (CPC) committee, and was split off from the Chinese central bank in 1983. The State Administration of Foreign Exchange (SAFE) manages China’s current and capital accounts, administers China’s balance of payments, and supervises the Chinese foreign exchange market. But its also carries out intervention operations using China’s foreign exchange and gold reserves.

Central Huijin Investment Company, through which the Chinese government maintains interests in China’s largest commercial banks, was created by SAFE in 2003, and since 2008 has been a fully-owned subsidiary of China’s sovereign wealth fund China Investment Corporation (CIC). CIC is itself owned by the People’s Republic of China (PRC). The Shanghai Gold Exchange (SGE) was launched by the PBoC in 2002 and is supervised by the PBoC. Prior to the formation of the SGE, the PBoC directly managed the entire Chinese gold market. The China Gold Association (CGA) was launched by the PRC and the State Economic and Trade Commission.

A number of large Chinese commercial banks such as ICBC, Bank of China, CCB, BoCom and ABC are heavily involved in the Chinese gold market. These banks are all Chinese state controlled. State-controlled Industrial and Commercial Bank of China (ICBC) has the Ministry of Finance and Central Huijin Investment Company as controlling shareholders. Bank of China (BoC), which until 1979 was actually managed by the PBoC, use to run SAFE. Central Huijin Investment Company now has a controlling interest in BoC. Central Huijin Investment Company is also a controlling shareholder of China Construction Bank (CCB).

Since the People’s Republic of China (PRC) is a centrally planned and controlled economy, it’s distinctly possible that other Chinese state controlled entities also accumulate gold reserves on behalf of the Chinese government and either transfer this gold to the PBoC at sporadic intervals or else maintain their own distinct gold holdings for future amalgamation. A gold accumulation strategic by the Chinese government utilising a number of state entities would therefore make the reporting of gold reserve holdings by the PBoC only one element of a broader long-term State gold buying strategy.

References and Links

1.^ About the PBoC, People’s Bank of China website http://www.pbc.gov.cn/english/130712/index.html

2.^ World Official Gold Reserves by country, World Gold Council http://www.gold.org/research/latest-...-gold-reserves

3.^ Quarterly time series of official gold reserves World Gold Council https://www.gold.org/research/quarte...-reserves-2000

4.^ “China’s gold reserves reach 1,054 tonnes”, Xinhua – China Daily, 24 April 2009 http://www.chinadaily.com.cn/china/2...nt_7714124.htm

5.^ “Analyzing PBOC Official Gold Reserves Increment”, BullionStar Blogs 19 July 2015, https://www.bullionstar.com/blogs/ko...serves-update/

6.^ Shanghai Gold Exchange, Chinese Gold Market, BullionStar Gold University https://www.bullionstar.com/gold-uni...rket#heading-5

7.^ “PBOC Gold Purchases: Separating Facts from Speculation”, BullionStar blogs, May 2015 https://www.bullionstar.com/blogs/ko...m-speculation/

8.^ “IMF Gold Sales – Where ‘Transparency’ means ‘Secrecy’”, BullionStar Blogs, September 2016 https://www.bullionstar.com/blogs/ro...means-secrecy/

9.^ “China gold holdings jump 57 pct in 6-year reserve update”, Reuters, July 2015 http://www.reuters.com/article/china...0ZX39R20150717

10.^ Gold author, James Rickards, tweet in relation to PBoC gold reserves security, August 2015 https://twitter.com/JamesGRickards/s...19732981784576

11.^ The Scale of China’s Foreign Exchange Reserves, SAFE website http://www.safe.gov.cn/wps/wcm/connect/87dcf3804c420ce0aa1caefd3fd7c3dc/The+Scale+of+China’s+Foreign+Exchange+Reserves((January+2016-Nov+2016).xls

12.^ “China breaks 6-year silence on gold reserves”, Financial Times, July 2015 https://www.ft.com/content/2c67f078-...3-e7aedbb7bdb7

13.^ China’s official reserve asset monthly updates, State Administration of Foreign Exchange (SAFE) website http://www.safe.gov.cn/wps/portal/english/Data

14.^ Official gold reserve holdings per country, IMF website, See International Financial Statistics (IFS) http://data.imf.org/

1

- #834

- Jan 4, 2017 9:19pm Jan 4, 2017 9:19pm

- | Commercial User | Joined Dec 2014 | 14,163 Posts

Disliked[Цитата = dttsomh; 9404333] {цитата} Денежный поток:. Акции / Облигации -> USDX -> USD30 и USD / JPY USD / JPY и USD30 -> USDX -> Акции / Облигации [/ цитата] Right, here money and flow...Ignored

Hello wayfarer

I just logged on to your account. You are doing very good. Keep up your excellent work. Thanks for your help as well. I am going to log off soon as I have put in more than a full day. See you soon. Good Evening.

Benjaminis

Good day

Hope everyone is doing well.

I must still catch up on the last few pages, was out with friends last night.

Here is the charts so long.

I added 1 x JPY & 1 x US30 short last night on my return home.

I closed my JPY with some nice profit this morning. Will look for a retracement, otherwise wait for Friday after news.

Hope everyone is doing well.

I must still catch up on the last few pages, was out with friends last night.

Here is the charts so long.

I added 1 x JPY & 1 x US30 short last night on my return home.

I closed my JPY with some nice profit this morning. Will look for a retracement, otherwise wait for Friday after news.

Attached Image(s) (click to enlarge)

- #836

- Edited 12:40am Jan 5, 2017 12:12am | Edited 12:40am

- | Joined Aug 2009 | Status: Trader | 46 Posts

Hello all!

Benjamin, still don't understand how we can use that .

Money flows from one financial instrument to another constantly . This is what the market is in total. What does it give us? We can say that if EURUSD is falling then USDCHF is rising , or money flows from EURUSD to USDCHF. But it gives us absolutely no any advantage. You can say if you know that money goes into USDCHF then buy it, but that means that money goes from EURUSD and if we know that we can just sell it, why do we need one more instrument to operate with? We could use that if one instrument has a delay before the other , it has a name the market imperfection. But we havent it. If you can predict a financial crysis (read as to predict where the money will flow) you don't need to buy gold you can just sell dow. Please explain the heart of your method .

Thank you

Benjamin, still don't understand how we can use that .

Money flows from one financial instrument to another constantly . This is what the market is in total. What does it give us? We can say that if EURUSD is falling then USDCHF is rising , or money flows from EURUSD to USDCHF. But it gives us absolutely no any advantage. You can say if you know that money goes into USDCHF then buy it, but that means that money goes from EURUSD and if we know that we can just sell it, why do we need one more instrument to operate with? We could use that if one instrument has a delay before the other , it has a name the market imperfection. But we havent it. If you can predict a financial crysis (read as to predict where the money will flow) you don't need to buy gold you can just sell dow. Please explain the heart of your method .

Thank you

DislikedMorning Thoughts - Daily https://www.theburningplatform.com/2...7/#more-139985 PLEASE READ THE WHOLE ARTICLE AND THEN SHARE YOUR THOUGHTS BRIEFLY ON WHAT YOU HAVE CONCLUDED. THANK YOU. Benjaminis Benjamin. Can Trump Fix The Economy In 2017? Guest Post by Paul Craig Roberts The Western world and that part of the world that partakes of Western explanations live in a fictional BenjaminisIgnored

There is a lot of fake propaganda going around, and most accepts it as the truth.

US corporations produce goods offshore, because of the much lower labour costs, which then results in higher profits and also higher stock prices for their shareholders.

Due too many US corporations that produce offshore, the work opportunities in US has declined, Median family incomes have fallen, real estate values in abandoned manufacturing’s has fallen. State and local government’s pension systems cannot meet their obligations.

The populations of a lot of manufacturing and industrial cities in US has declined.

The corrupt US economics profession and financial media have claims that offshoring is good for the economy, they want us to believe that the unemployment rate has fallen and that new jobs was created in November, but the real facts is that people is moved to the discouraged category, because the unemployment rate does not include discouraged workers.

The data released by the Bureau of Labour statistics show many problematic aspects of the data.

“The growth of real median family income ceased. Without increases in consumer spending to drive the economy, the Federal Reserve substituted a growth in consumer debt for the missing growth in real median family income. But the growth of consumer debt is limited by the lack of growth in consumer income. Thus, an economy dependent on debt expansion is limited in its ability to expand. Unlike the federal government, the American people cannot print money with which to pay their bills.”

The American economic future is one of continuing decline into Third World status.

Corporations such as Apple, almost entirely produced in Chinese factories, Apple plans to replace the inexpensive Chinese labour with robots, which do not have to be paid any wages.

He sums it up nicely here.

“There can be no fix unless the ladders of upward mobility that made the US an opportunity society can be put back in place. This will require bringing home the offshored middle class jobs or, assuming that new high value-added jobs could somehow be created, preventing the new jobs from being moved offshore.

Can Trump script “The Escape From Globalism?” He could lose the fight. Globalism has been institutionalized. The large corporations that have offshored their production for US markets would oppose moves against jobs offshoring. So would all their shills in the economics profession and financial media. I don’t know the extent to which globalism has taken root in people’s minds in Asia, Africa, and South America, but in Europe—even some in Putin’s Russia—people are brainwashed in the belief that they can’t exit globalism without paying a large economic price.”

DislikedHello all! Benjamin, still don't understand how we can use that . Money flows from one financial instrument to another constantly . This is what the market is in total. What does it give us? We can say that if EURUSD is falling then USDCHF is rising , or money flows from EURUSD to USDCHF. But it gives us absolutely no any advantage. You can say if you know that money goes into USDCHF then buy it, but that means that money goes from EURUSD and if we know that we can just sell it, why do we need one more instrument to operate with? We could use that...Ignored

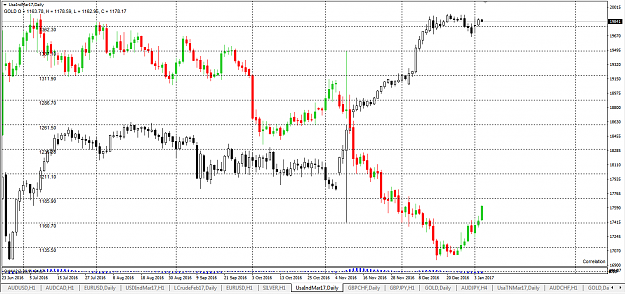

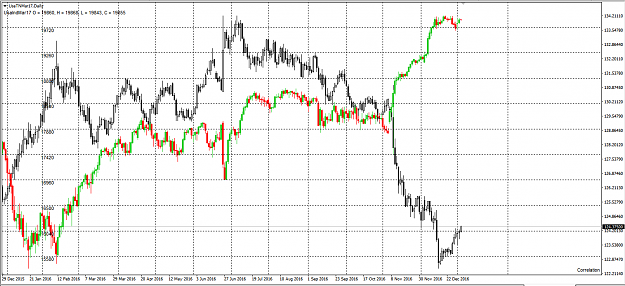

Not sure if this helps any but here are charts of the Dow and UJ. While there are correlations across instruments, they don't always move at the same time. On the 3rd they both moved in sync. Dow filled the gap and pushed back into highs. On the 4th while the Dow was finding resistance at the highs, UJ starting dropping again and has made a 200+ pip swing while Dow is still holding. As we use Money Flow for direction, instruments may take direction at different times, so we treat each instrument as a separate trade. Risking properly and taking larger gains(risk to reward) will keep us ahead. In this case if we were just trading the Dow, then there was a missed opportunity for at least a 1:3 return on UJ.

Attached Image(s) (click to enlarge)

2