DislikedMathematician, Have you ever looked at co-integrated pairs and triplets? I did some work on it a while back, and will revisit after my current projects are finished and trading. Basically I did this: 1) Download 1 year of hourly closing data on 25 currency pairs. This is done daily. 2) Use R (an open source statistical analysis program) to merge all by Date / Hour 3) Remove missing data fields (4) and below are for 2 pairs X and Y, but if you do 3 pairs X, Y, and Z its similar ... just a bit more complicated 4) Run a linear regression of each pair...Ignored

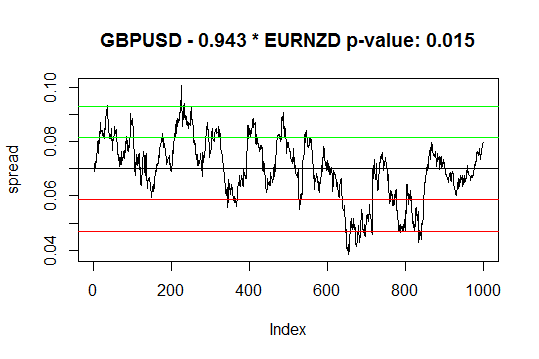

5) Calculate the spread. For 2 pairs, spread = X - Coef * Y

Is that right?