I'm gonna show you a simple initial approach to the "pattern detection" idea. I will use the open of the last 7 bars to define a "pattern" which will be the relationships between these values. I then look into the past to see if there are enough examples to train my machine learning algo. This is a function to perform this task, it returns 1 if there are enough examples in the historical data, 0 if there are not enough:

If there are enough examples I then build the input/output array using the matching patterns I have located in the past. In this case the inputs are a past number of returns and the outputs are the outcomes of long and short trades managed with a simple trailing stop where the SL is moved to the starting SL value distance from the current open if this stop is more favorable than the present stop:

With these two functions I can build the machine learning functions. This time I decided to use a neural network as the machine learning algo:

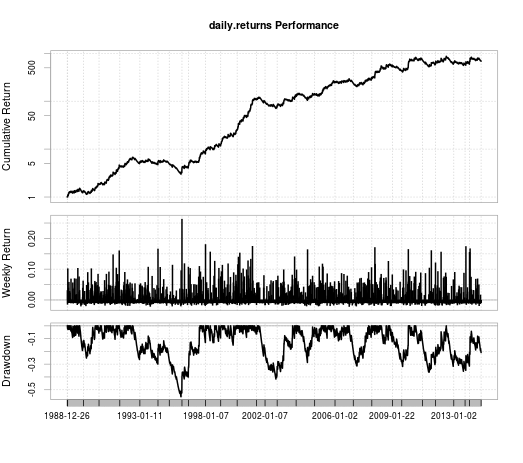

In this case the algorithm is retrained and relaunched on every hourly bar where there are enough examples. I then performed an optimization to see if I could find anything worth it on the EUR/USD 1H and found some interesting stuff. Here is a linear system example I found:

starting SL = 150% ATR20

B = 75 (number of examples used per training)

C = 8 (number of input returns used per example)

D = 185 (frontier for the trade output)

This algo does not use any hourly filters on the 1H chart, for this reason it's very different from everything I have shared so far on the 1H. Thoughts, always appreciated...

Inserted Code

int is_viable_examplesByStructure(int examplesNeeded, int frontier){

int tl = frontier;

double open1, open2, open3, open4, open5, open6, open7;

open1 = iOpen(0,1);

open2 = iOpen(0,2);

open3 = iOpen(0,3);

open4 = iOpen(0,4);

open5 = iOpen(0,5);

open6 = iOpen(0,6);

open7 = iOpen(0,7);

int i = 0, j = 0, n=0, m = 0;

while(m<examplesNeeded && i+tl+500<iBars(0)){

if (

((iOpen(0,i+tl+1) > iOpen(0,i+tl+2)) == (open1 > open2)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+3)) == (open1 > open3)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+4)) == (open1 > open4)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+5)) == (open1 > open5)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+6)) == (open1 > open6)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+7)) == (open1 > open7)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+3)) == (open2 > open3)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+4)) == (open2 > open4)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+5)) == (open2 > open5)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+6)) == (open2 > open6)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+7)) == (open2 > open7)) &&

((iOpen(0,i+tl+3) > iOpen(0,i+tl+4)) == (open3 > open4)) &&

((iOpen(0,i+tl+3) > iOpen(0,i+tl+5)) == (open3 > open5)) &&

((iOpen(0,i+tl+3) > iOpen(0,i+tl+6)) == (open3 > open6)) &&

((iOpen(0,i+tl+3) > iOpen(0,i+tl+7)) == (open3 > open7)) &&

((iOpen(0,i+tl+4) > iOpen(0,i+tl+5)) == (open4 > open5)) &&

((iOpen(0,i+tl+4) > iOpen(0,i+tl+6)) == (open4 > open6)) &&

((iOpen(0,i+tl+4) > iOpen(0,i+tl+7)) == (open4 > open7)) &&

((iOpen(0,i+tl+5) > iOpen(0,i+tl+6)) == (open5 > open6)) &&

((iOpen(0,i+tl+5) > iOpen(0,i+tl+7)) == (open5 > open7)) &&

((iOpen(0,i+tl+6) > iOpen(0,i+tl+7)) == (open6 > open7))

)

{

m++;

}

i++;

}

if (m<examplesNeeded){ return(0) ;} else { return(1); }

} If there are enough examples I then build the input/output array using the matching patterns I have located in the past. In this case the inputs are a past number of returns and the outputs are the outcomes of long and short trades managed with a simple trailing stop where the SL is moved to the starting SL value distance from the current open if this stop is more favorable than the present stop:

Inserted Code

RegressionDataset regression_i_simpleReturn_o_tradeOutcome_examplesByStructure(int period, int barsUsed, double initial_SL, int frontier, double minStop){

Data<RealVector> inputs(period,RealVector(barsUsed));

Data<RealVector> labels(period,RealVector(2));

double openPrice;

double SL_long, SL_short, new_SL;

double atr;

int tl = frontier;

double open1, open2, open3, open4, open5, open6, open7;

open1 = iOpen(0,1);

open2 = iOpen(0,2);

open3 = iOpen(0,3);

open4 = iOpen(0,4);

open5 = iOpen(0,5);

open6 = iOpen(0,6);

open7 = iOpen(0,7);

int i = 0, j = 0, n=0, m = 0;

while(m<period){

if (

((iOpen(0,i+tl+1) > iOpen(0,i+tl+2)) == (open1 > open2)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+3)) == (open1 > open3)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+4)) == (open1 > open4)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+5)) == (open1 > open5)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+6)) == (open1 > open6)) &&

((iOpen(0,i+tl+1) > iOpen(0,i+tl+7)) == (open1 > open7)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+3)) == (open2 > open3)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+4)) == (open2 > open4)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+5)) == (open2 > open5)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+6)) == (open2 > open6)) &&

((iOpen(0,i+tl+2) > iOpen(0,i+tl+7)) == (open2 > open7)) &&

((iOpen(0,i+tl+3) > iOpen(0,i+tl+4)) == (open3 > open4)) &&

((iOpen(0,i+tl+3) > iOpen(0,i+tl+5)) == (open3 > open5)) &&

((iOpen(0,i+tl+3) > iOpen(0,i+tl+6)) == (open3 > open6)) &&

((iOpen(0,i+tl+3) > iOpen(0,i+tl+7)) == (open3 > open7)) &&

((iOpen(0,i+tl+4) > iOpen(0,i+tl+5)) == (open4 > open5)) &&

((iOpen(0,i+tl+4) > iOpen(0,i+tl+6)) == (open4 > open6)) &&

((iOpen(0,i+tl+4) > iOpen(0,i+tl+7)) == (open4 > open7)) &&

((iOpen(0,i+tl+5) > iOpen(0,i+tl+6)) == (open5 > open6)) &&

((iOpen(0,i+tl+5) > iOpen(0,i+tl+7)) == (open5 > open7)) &&

((iOpen(0,i+tl+6) > iOpen(0,i+tl+7)) == (open6 > open7))

){

atr = iAtrWholeDaysSimpleShift(PRIMARY_RATES, 20, i+tl+1);

openPrice = cOpen(i+tl);

SL_long = openPrice+spread()-atr*initial_SL;

SL_short = openPrice+atr*initial_SL;

n = 0;

while ((SL_long < low(i+tl-n)) && (n<tl)){

n += 1;

atr = iAtrWholeDaysSimpleShift(PRIMARY_RATES, 20, i+tl-n+1);

new_SL = cOpen(i+tl-n)+spread() - (initial_SL*atr);

if(new_SL <= SL_long){

new_SL = cOpen(i+tl-n);

}

if (cOpen(i+tl-n)-new_SL > minStop){

SL_long = new_SL;

}

}

labels.element(m)[0] = SL_long-(openPrice+spread());

n = 0;

while ((SL_short > high(i+tl-n)+spread()) && (n<tl)){

n += 1;

atr = iAtrWholeDaysSimpleShift(PRIMARY_RATES, 20, i+tl-n+1);

new_SL = cOpen(i+tl-n) + (initial_SL*atr);

if(new_SL >= SL_short){

new_SL = cOpen(i+tl-n);

}

if (new_SL-cOpen(i+tl-n) > minStop){

SL_short = new_SL;

}

}

labels.element(m)[1] = openPrice-SL_short;

for(j=0;j<barsUsed;j++){

inputs.element(m)[j] = (iOpen(0,tl+j+i)-iOpen(0,1+tl+j+i))/iOpen(0,1+tl+j+i);

}

m++;

}

i++;

}

RegressionDataset dataset(inputs,labels);

return dataset;

} With these two functions I can build the machine learning functions. This time I decided to use a neural network as the machine learning algo:

Inserted Code

double NN_Prediction_i_simpleReturn_o_tradeOutcome_examplesByStructure(int learningPeriod, int barsUsed, double initial_SL, int frontier, double minStop, int trainingEpochs)

{

int is_viable = is_viable_examplesByStructure(learningPeriod, frontier);

if (is_viable == 0) return(0);

RegressionDataset dataset = regression_i_simpleReturn_o_tradeOutcome_examplesByStructure(learningPeriod, barsUsed, initial_SL, frontier, minStop);

FFNet<FastSigmoidNeuron,FastSigmoidNeuron> network;

unsigned numInput=barsUsed;

unsigned numHidden=(int)((barsUsed+2)/2);

unsigned numOutput=2;

unsigned numberOfSteps=trainingEpochs;

unsigned step;

network.setStructure(numInput, numHidden, numOutput);

initRandomUniform(network,-0.5,0.5);

SquaredLoss<> loss;

ErrorFunction error(dataset, &network,&loss);

RpropMinus optimizer;

optimizer.init(error);

for(step = 0; step < numberOfSteps; ++step){

optimizer.step(error);

}

network.setParameterVector(optimizer.solution().point); // set weights to weights found by learning

Data<RealVector> testOutput;

RegressionDataset datasetInput = p_regression_i_simpleReturn(barsUsed);

testOutput = network(datasetInput.inputs());

if (testOutput.element(0)[0] > 0 && testOutput.element(0)[1] < 0) return(1);

if (testOutput.element(0)[1] > 0 && testOutput.element(0)[0] < 0) return(-1);

return(0);

} In this case the algorithm is retrained and relaunched on every hourly bar where there are enough examples. I then performed an optimization to see if I could find anything worth it on the EUR/USD 1H and found some interesting stuff. Here is a linear system example I found:

starting SL = 150% ATR20

B = 75 (number of examples used per training)

C = 8 (number of input returns used per example)

D = 185 (frontier for the trade output)

Attached Image

This algo does not use any hourly filters on the 1H chart, for this reason it's very different from everything I have shared so far on the 1H. Thoughts, always appreciated...