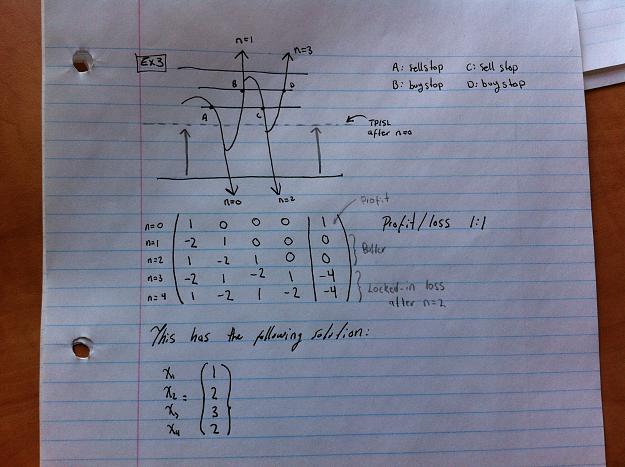

Disliked{quote} Yes. Exactly! I used 1s because it was easy— but yes it could be any number greater than or equal to zero (actually, negative numbers [representing a loss] should also be considered but I will discuss this later). In fact, if we make the final column (1, 0, 0, 0, 0), the solution becomes (1, 2, 3, 6, 12). The goal here would be to minimize the exponential growth of martingale as much as possible. The zero would represent a scenario in which we break-even (however in reality I don’t think it would be this ideal because of the bid/ask spread)....Ignored

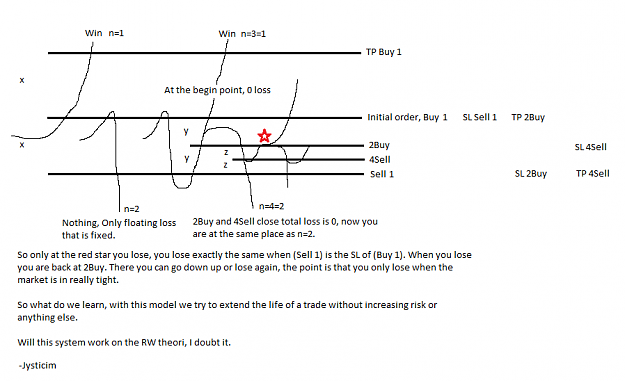

If the price comes back to the original price you open a buy. If the SL is hit you lose the previous gain and you're BE. The BE doesn't come from the smart way of arranging the orders. The next coin flip just loses the previous gain.

After either scenario n=0 or n=1 happended, either the price comes back and you play again from the original level or you can start the process again from another price level. But since you assume a RW, the starting level is irrelevant and the previous PnL have no influence on the future.

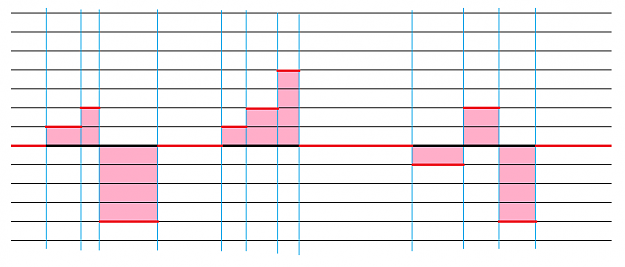

Now it is trivial to see that the system either wins 1 or loses 1 with 50% chance each and is therefore BE long term before spread. From this fact it is pointless to try to mix it with any other system, including the (2).

Now by thinking in term of exposure, I leave you as an exercice to discover that the second system is actually the very same as the (1). And, therefore, has the same 0 expectancy.

No greed. No fear. Just maths.