Disliked{quote} Your rules and definitions are ok. Note that I do all calculations (including the ATR calculation) on daily data that has been corrected to GMT DST +2, non-DST +1. If you can please post some balance graphs so that I can take a quick look and see what might be wrong (sadly do not have time to go through and process txt files). Have you compared your predictions with the ones I posted before? Are they in alignment? Differences could be because of a few reasons, the ATR calculation (mine is done with the ATR as implemented in TA-lib) or the...Ignored

data (post #99) I get exactly the same result as you get. The algorithm I use for the ATR is the one described on Wikipedia except that I skip the week-end candles. I tried with and without the week-end with no noticeable change.

Note that I exclusively use tick data for the BT. My simulator simply can't use candles: I emulate a broker which feeds the ticks. My SL are executed at the bid or ask of the breaking tick. The spread is the spread at the time the order is executed. This may also make a difference.

EDIT: I forgot to say that I don't take any commission or swap into account.

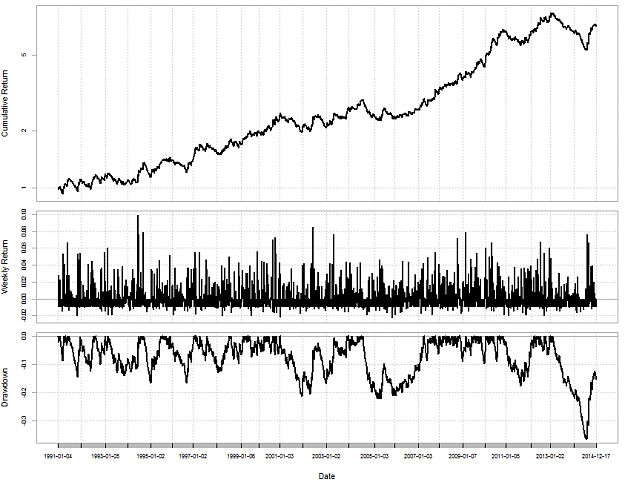

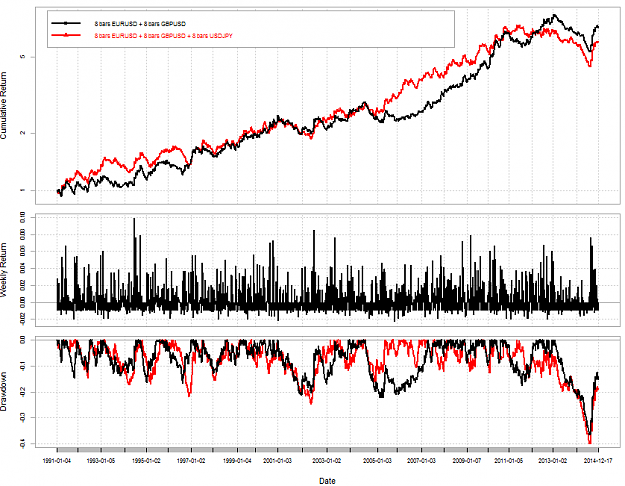

Attached Image (click to enlarge)

No greed. No fear. Just maths.