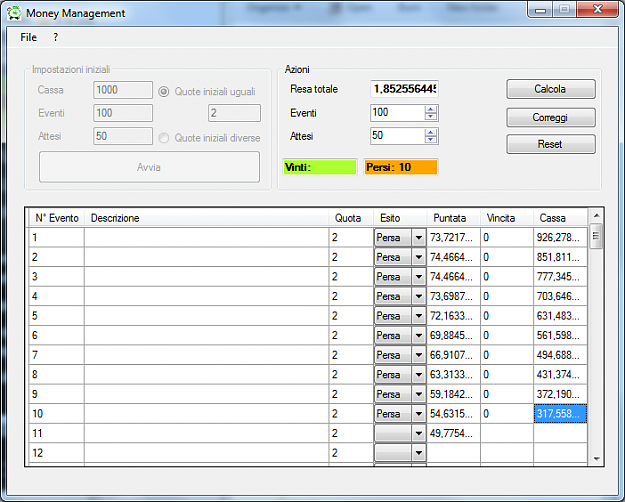

The results are fully in line with my previous posts. With a winrate=50% and RR=1 your MM starts betting 7.37% of the starting capital that I set to 1000.

If we bet 7.37% each time and get 10 losers the final result is 464.96. With your MM the result is 317.56. The risk increases to 14.68% => worse DD

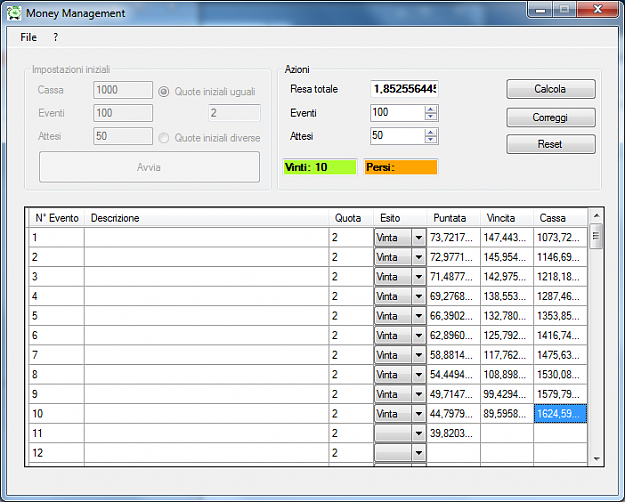

If we bet 7.37% each time and get 10 winners the final result is 2036.66. With your MM the result is 1624.59. The risk decreases to 2.84% => less profits

Yet if we alternate win and loss 5 times the result is better: 1003.97 instead of 973.

Clearly the Gambler's Fallacy at work. Such MM can't work as long as there is no serial correlation between the trade outcomes. In the long run you will get the same overall result but with a higher volatility of the equity curve (=higher risk of ruin)

If we bet 7.37% each time and get 10 losers the final result is 464.96. With your MM the result is 317.56. The risk increases to 14.68% => worse DD

If we bet 7.37% each time and get 10 winners the final result is 2036.66. With your MM the result is 1624.59. The risk decreases to 2.84% => less profits

Yet if we alternate win and loss 5 times the result is better: 1003.97 instead of 973.

Clearly the Gambler's Fallacy at work. Such MM can't work as long as there is no serial correlation between the trade outcomes. In the long run you will get the same overall result but with a higher volatility of the equity curve (=higher risk of ruin)

No greed. No fear. Just maths.