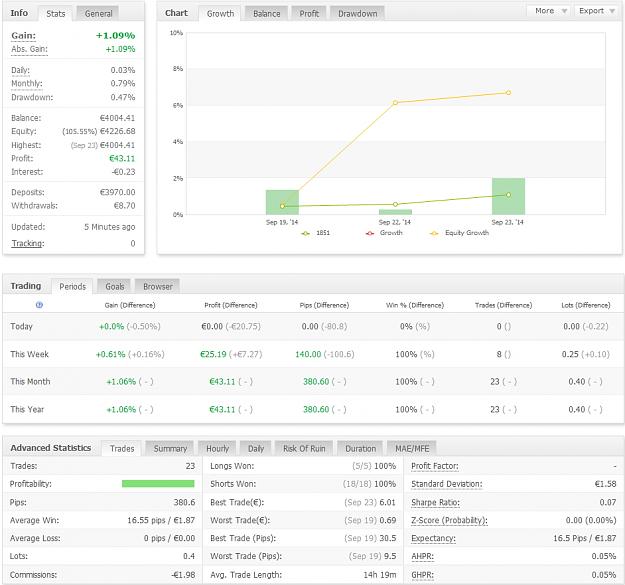

MGH strategy can be adjusted many ways, so it will not be easy to find the best parameters for the "best" results, especially that "best" is a very subjective term. For me "best" means safest with a decent profit return.

Short term-optimization might help, especially that the strategy parameters should be adjusted to the ever-changing market conditions. In other words long-term backtesting and long-term optimization (with the same parameters) might be counterproductive.

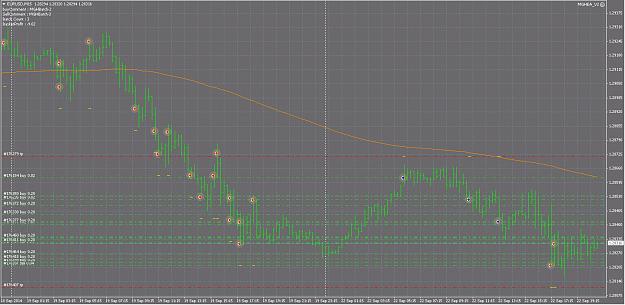

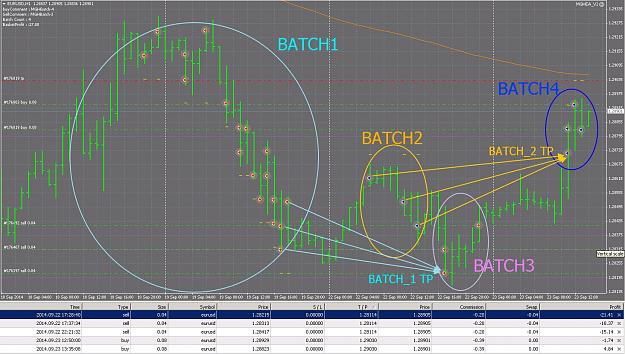

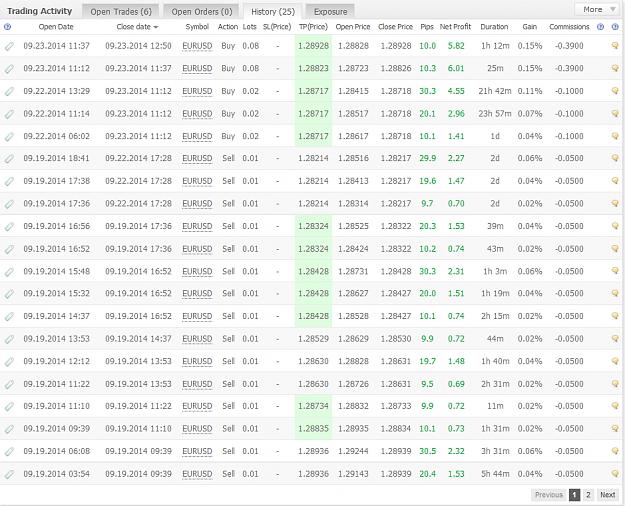

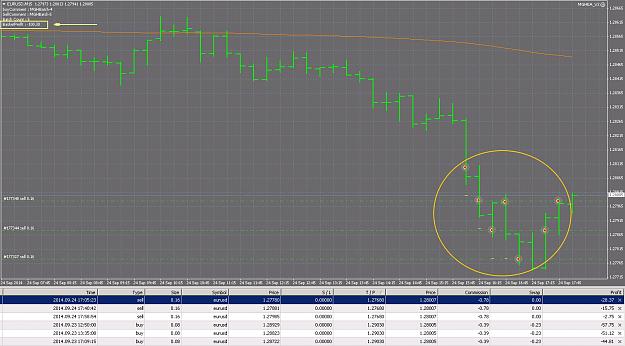

My beta live forward test has the following parameters:

Grid step: 10 pips (as per original strategy).

Levels in each batch: 3 (as per original strategy)

Max. batches: 5

Potential profits in Batch1: 10 or 30 or 60 pips. (as per modified strategy)

Basket Profit: 60 pips (modified), i.e. 0.6% on a 1k account.

(Once a Hedge2 trade is opened, the strategy switches to "Basket Mode", i.e. calculating profits for the entire basket, incl. closed and floating P&L.)

Stop Loss: -2000 pips (which is about 20% of a 1k account).

Short term-optimization might help, especially that the strategy parameters should be adjusted to the ever-changing market conditions. In other words long-term backtesting and long-term optimization (with the same parameters) might be counterproductive.

My beta live forward test has the following parameters:

Grid step: 10 pips (as per original strategy).

Levels in each batch: 3 (as per original strategy)

Max. batches: 5

Potential profits in Batch1: 10 or 30 or 60 pips. (as per modified strategy)

Basket Profit: 60 pips (modified), i.e. 0.6% on a 1k account.

(Once a Hedge2 trade is opened, the strategy switches to "Basket Mode", i.e. calculating profits for the entire basket, incl. closed and floating P&L.)

Stop Loss: -2000 pips (which is about 20% of a 1k account).