this guy can write an article.. The Mind-Body Response by JupaFX Trading is a very difficult job, not only because of the technical requirements but also because of the mental toughness and discipline it requires. As traders we are constantly making decisions and we hope for the best ... http://www.orderflowtrading.com/Articles.aspx {image}

Ignored

Nice picture.

Discussion is an exchange of knowledge;argument is an exchange of ignorance

EUR/USD was stuck in a tight range within close proximity to recent highs, just short of 1.3700. As was rumoured yesterday, buyers were loathe to challenge supposed barrier defence at 1.3700. But limited pullbacks drew sovereign and pension fund buying, the sort of accounts that would usually generate a following. EUR/GBP selling provided some counter balance to the EUR/USD demand, as did corporate hedging in EUR/USD. But with pullbacks so small, a break to new highs seems very likely, and players look to today’s US ISM to provide the next spark for trade. Significant resistance lies 1.3740-50

AMERICAS

The USD is mixed, being generally strong against most European currencies as relative growth and central

bank policy support the rally, but weak against many of the commodity currencies and the GBP. The CAD

has regained a steady appreciating tone since mid-March aided by low volatility in global financial markets,

recovering price dynamics in selective commodity markets and continued supportive growth. The MXN has

abandoned its appreciating path versus the USD as market participants assess recent monetary policy

actions and the likelihood of a pullback in the emerging-market rally of the past few months.

EUROPE

The EUR has found a technical support level following two months of weakness versus peer currencies.

The ECB will favour deeper monetary stimulus and unattractive interest rate differentials will weigh on the

EUR through the remainder of the year. The GBP retains a solid tone against both the USD and EUR on

the back of a strengthening economic environment and the most aggressive monetary tightening in the 18

months ahead. The RUB has sharply recovered the lost ground based upon widespread expectations that

the Russia/Ukraine conflict will de-escalate without energy supply disruptions in the near term.

ASIA / PACIFIC

The JPY remains well supported despite its weakening growth outlook associated with the negative effects

from tax reforms; its role as a safe-haven status in the Asia/Pacific region remains intact. The CNY regained

a stabilization tone following a period of sustained weakness driven by adjustments to introduce more

flexibility in exchange rate markets. The KRW continues to show strong performance within the Asia/Pacific

region supported by a solid macroeconomic outlook. The THB has consolidated a stable and comfortable

trading range year to date despite the lingering concerns about the domestic political environment.

Planning the week ahead

by JupaFX

In this weekly report, we will try to direct our attention to the currency pairs and assets that are most likely to offer trading opportunities during the coming week, based on a combination of sentiment, orderflow, and price action analysis. On the docket for this week

Taking a glance at our calendar, we can notice the more important news events for the week. The main events this week are:

Monday: AUD AiG construction index, GER Ind. Prod. (bearish expectations), CAD Ivey PMI + Building Permits Tuesday: NZD Nzier business conf., AUD NAB Business Confience, GER Trade Balance + CA Balance (bearish expectations), UK Ind. Prod. + Manuf. Prod. (bullish expectations), US Chain store sales + Redbook Wednesday: CNY CPI, AUD Westpac Cons. Sentiment, FOMC Minutes, Crude Oil Inventories Thursday: AUD Employment data (bullish expectation), CNY Trade Balance, UK Trade Balance (bullish expectations) + BOE Decision Friday: CAD Unemployment data Strong vs. Weak

Looking at the CME FX futures market, we can see that:

DXY has closed last week with a neutral stance, finding bids around 80 and offers around 80.50.

GBP has a bullish bias

CAD has a bullish bias

EUR has a bearish bias

So if we combine and filter the most evident FX pairs to analyze, we come up with:

EURGBP short bias

EURCAD short bias

GBPUSD long bias

Sentiment Analysis on relevant assets

Markets continue to favor the permissive monetary policy stances of the ECB and the FED, carry trades are still in play and risk appetite is still alive. Some analysts see growth starting to improve on a global scale without any signs of inflationary pressure and central banks do not see an urgent need to adjust the very accommodative monetary policy stance. In the past week it has become clear that concerns about financial stability are unlikely to force central banks to remove some of the accommodation. Janet Yellen in a speech at the IMF headquarters this week also argued strongly that monetary policy should be solely focused on price stability and employment while containing financial risk should be left mainly to macro-prudential policies. If you missed the speech, here it is.

Moreover, the BIS has finally caught up to the curve, and has “discovered” something that has been evident for years: it insists on the need to recognize that financial booms and busts have become a major threat to macroeconomic stability. In the short term, because monetary policy has been excessively burdened for too long, the risk of normalizing too slowly and too late must deserve special attention. Well, at least they came out and said it...better late than never...

Since many are talking about it, but few really know what we're talking about and even less have the courage to ask, here's a chart taken from Borio (2003) explaining macro-prudential and micro-prudential. Wikipedia can help with the rest. http://www.orderflowtrading.com/Port...e002_thumb.png

USD: sentiment is neutral. While US jobs growth was strong, key details like earnings and part-time work are still consistent with the kind of slack in the labor market that will keep the FED cautious. Also, the absence of stronger wage growth suggests that inflationary pressures could remain subdued (to use a term that Draghi is so fond of). Euro: sentiment is negative. Recent data suggests that the euro area has lost a bit of momentum recently, particularly in France but also in Germany. Growth momentum continues to favor the US and this should continue to cap EURUSD. Draghi is of the same opinion as Yellen regarding the use of monetary policy to address financial stability: Draghi indicated that macro-prudential measures and regulation is the first line of defense, not monetary policy (price and quantity of money). Monetary policy seems to be less effective as an instrument and operates with unpredictable lags. Macro-prudential policy and regulatory efforts are more precise and can be implemented almost immediately. This is part of the new orthodoxy, which is a natural overcompensation after the lack of enforcement that brought us to the 2007 crisis. CAD: sentiment is positive. Ex-post, there were some diverse drivers of CAD strength for this recent trend: 1) the Canadian domestic story, specifically rising inflationary pressures and encouraging data releases, in particular exports; 2) the U.S. economy, where an improvement in the high frequency data points allowed markets to look through the downward revisions to Q1 GDP; 3) rising oil prices; 4) massive short covering, assessed via COT data. All this dampens the likelihood that CAD may weaken from here. Just watch for any open-mouth ops from BOC that could discourage the markets from singing “O Canada...” for much longer. GBP: sentiment is positive. The MPC meeting in July is likely to be a non-event, but the recent flow of data has comforted the scenario of continued solid growth in the UK. While upbeat activity data increases the likelihood of a rate hike as soon as this year, it has not been accompanied so far by an increase in wage growth, which is a precondition for monetary policy tightening. As MPC member Martin Weale, historically on the hawkish spectrum of the MPC, pointed out in his recent speech “there is the continuing unusual weakness in wages …should wages growth fail to revive, that will, on its own, tip the scales further in favor of maintaining string monetary policy stimulus”.

For updates on sentiment as it progresses throughout the week, stay active in our Live Trading Floor.

To sum up: best looking charts & comments http://www.orderflowtrading.com/Port...e004_thumb.png

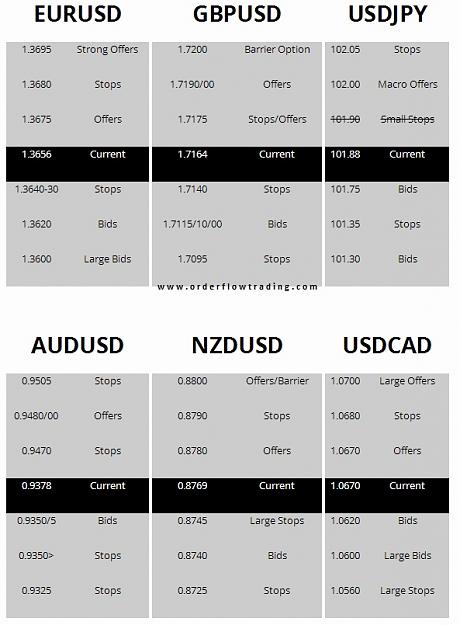

EURCAD Daily chart – The momentum selection continues to favor EURCAD shorts but common sense warrants caution. We are butting up against the 1.4400/30 zone which has already stopped price. http://www.orderflowtrading.com/Port...e006_thumb.png

EURGBP Weekly Chart – We have to dial out to a weekly view in order to gauge relevant downside targets.

That's how strong this trend is. Momentum is still down. http://www.orderflowtrading.com/Port...e008_thumb.png

GBPUSD Weekly Chart – in a similar fashion to EURGBP, we need a Weekly view to gauge upward levels. Just in case momentum dies into the week, keep an eye on the downside hurdle (red) for direction.

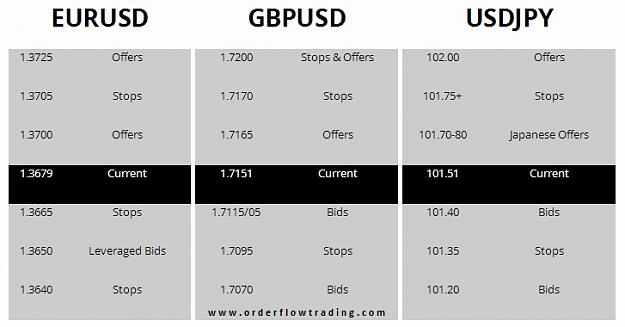

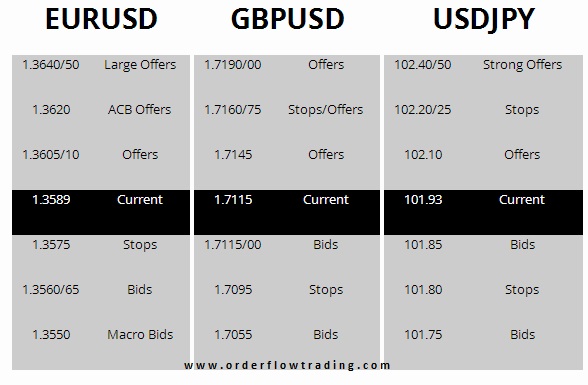

GBPUSD- stops build 1.7135/25, bids arrive 1.7115/00 [Dow Jones]--The U.K. data calendar is relatively light this week, with the Bank of England expected to keep rates unchanged at its July meeting on Thursday. According to analysts at J P Morgan, the publication of the labor market report next week will likely receive more market attention. "If employment continues to show strong gains with the unemployment rate falling, we could start to see more hawkish tones from MPC members that rates could start to rise without wages starting to show a significant pick-up."

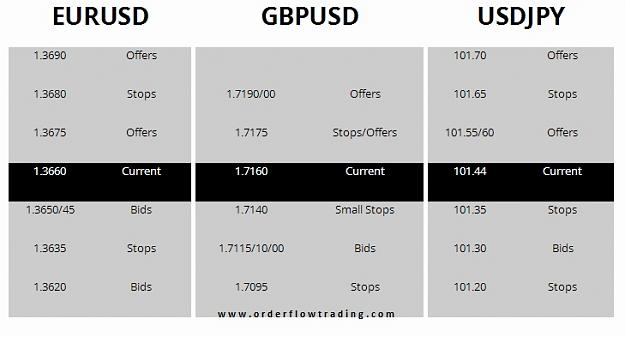

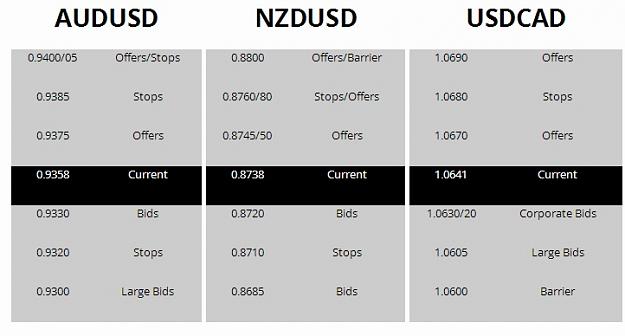

anybody else gettting that risk off feel? USDJPY- feeling pressured, heading toward stops below 101.70 with a bit of a risk off feel, Dax sells off as well