Most talk about Forex trading on here is focused on technical analysis on rightfully so. However, I am not a technical trader, or that is I understand technical trading however I am a much longer-term view (which in FX, isn't always saying much) and focus more around fundamentals or structural nature of the currency. In particular, focusing on the real supply and demand of a currency.

Before someone tries to give me lecture on how important technical analysis is in FX, let me assure you that I use such analysis however it is not my primary method of determining the direction I trade/invest but rather as a method of determining an entry point and when that position is fully valued, or an exit point.

Much like a company, the product or service that company sells can only be as good as the companies management in the long term. I don't think currencies veer too far off that path as monetary officials (and at times politicians) and their policies will determine the value of the currency primarily because they control the supply side of the equation however it will also affect the demand side of equation, e.g. interest rates. In the end, there are more outlaying factors that monetary officials do not control that will drive demand for a currency, e.g. business investment.

In any case, I am hoping others out there can both discuss and trade idea's off of said analysis. I do not have any breakthrough analysis but I have been looking at some data points that have me quite concerned with currencies like GBP and CHF that I'd like to share and get some thoughts and feedback on.

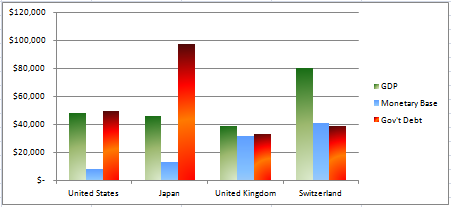

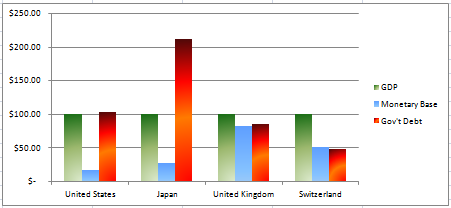

Starting with the Pound. The obvious fundamentals aren't pretty: recessionary environment with contracting GDP, low interest rate environment, monetary stimulus, high unemployment, high levels of debt to GDP, etc.

All of that said, the single most concerning thing on my radar for the pound is their monetary base and its rapid growth rate. Comparing the monetary base of the pound to the US dollar over the past 13 months (Sept 2011 - Sept 2012), we have seen an increase of 76% in the money supply while in the United States, believe it or not, the monetary base has decreased.

To make it clear, I look at the monetary base (M0 or narrow money) because it is the most liquid form of the money supply and a growth of the base will grow the other money supply measures due to the money multiplier effect.

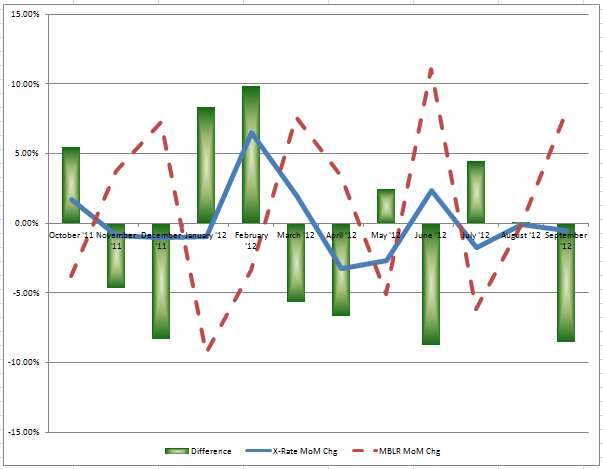

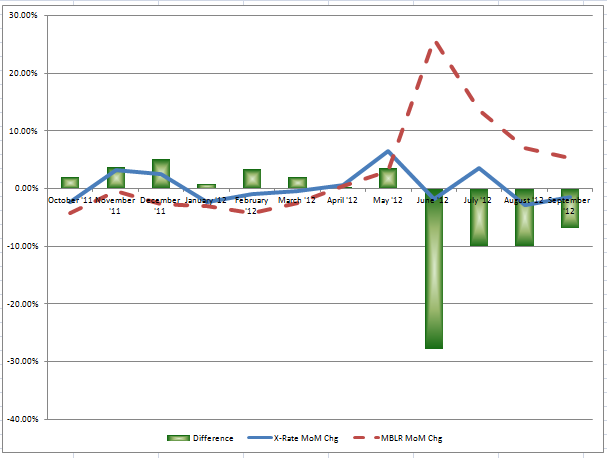

That said, the difference in the GBP/USD exchange rate relative to the GBP/USD monetary base ratio was 9.4% in September of 2011, or to say that the GBP/USD exchange rate was 1.56 (rounding) in September 2011 while the monetary base ratio was at 1.42.

Today, the real exchange rate for the pair rests at 1.615 while the monetary base ratio is at a whopping low of 0.80. That is a difference of over 103% in one year. While many factors effect exchange rates, I am not sure why we would see such a variance in the real exchange rate compared to the monetary base ratio. I am not advocating that the monetary base ratio should per at par with the exchange rate, but the divergence is quite astonishing to say the least.

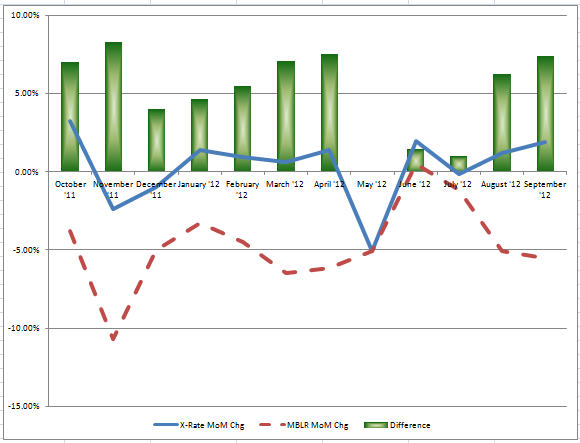

In comparison with the USD/JPY, we have seen the exchange rate move along with the monetary base ratio up until the last two months. Even when it has broken correlation in the past it seems to "catch up". Again, this is not a scenario where I am saying par is correct, however the pair seems to act (gain and lose) around supply.

Which leads me to my next point. If you deduced all other indicators and fundamentals factors for the pair, one could conclude that the monetary base differential has driven the direction of this pair. However, that same argument cannot be made for the GBP/USD.

So the questions begin:

- If we look at real supply as the real money in the system defined by a countries monetary base, then we could concluded that all being equal, if one country's supply of money grows faster than another, then that currency should depreciate (again, all else equal). Is this a fair conclusion?

- What would be the best way of defining demand? While we could broadly look at metrics like interest rates, current account balances, and growth metrics like GDP, are there more specific methods of determining real underlying demand outside of intraday price action?

More specific:

- If we can say that real supply = monetary base, then has there been such a demand to offset the GBP/USD monetary ratio difference to keep it elevated at these levels? More specific, could the Olympics in London have held the pair this high even while the monetary base ratio between the UK and the US has collapsed to 0.80? Or, was the market so forward-looking that it priced in a full blown QE by the US that will reverse the monetary base ratio back to normalized levels?

If the USD/JPY is moving on supply more than demand, as can be said over the past year, and GBP/USD is not moving on supply whatsoever, than that would imply that the GBP/USD has a massive bid under the pair.

The next logical question then would be:

- Assuming supply = monetary base then what components of the monetary base affect currency devaluation the most? I would assume the physical creation of notes and coins would do so, but there appears to be no "truthful" data on this.

I bring this point up because if one looks at the Swiss franc, the SNB has their monetary base driven up foreign exchange positions and the BoE has theirs in reserve balances, while the BoJ has most of its monetary base in notes and coins in circulation. That being said, the previous question would then be false right?

There are many factors that move a currency pair and this is only one variable, I understand that, however it is a variable to which I believe in a growth slowdown environment where monetary bases are not on their typical steady trend higher but rather going parabolic as Central Banks try to stave off deflation and spark economic growth, this variable has very high importance.

For hedge funds, a larger player in the FX world, the carry trade is almost nothing relative to 5 or 6 years ago, where they have to reach out to the AUD against USD, JPY, or CHF and yield very little. In short, it's becoming a very dangerous trade. This is how I would look at demand for a currency for the meantime, along with GDP per capita growth, unless we can define demand more substantially.

And on a final note, I have noticed recently that my broker is paying me above market rates in some cases to sell USD against other currencies or if buying the USD, is charging me above market rates for the carry. This tends to occur as they profit from the market rate to their rate and its differential however the spreads (interest rate spreads) between my broker and the market are widening out to points which I cannot remember them being this wide in the past two years. And it's all centered around the US dollar as the cross currencies seem to be the same as before.

The question: do you think my broker is experiencing some type of dollar shortage, is their a dollar shortage, or are they just trying to increase their business in this lower trading environment? And please answer if you actually have a good idea to why this is happening with some facts. By the way, I won't disclose my broker so please do not ask, but I do need to move.

Sorry for the length again. Looking to hear what some of you other fundamental traders have for thoughts on this plus other idea's.