i want to share my thoughts on money management.

i am a systematic trader so i like trading statistics. the biggest problem for me was how i can differentiate between normal or big drawdawn and system stopped working scenario and finding the risk/trade so then i can survive bad periods.

i found a solution for this. first of all you must define the system stopped working drawdawn, the maximum drawdawn you will allow yourself to have.

mine is at 30%. you can choose whatever you want...20%,40%

after deciding the maximum (system failed) drawdawn now we analyse the trading system's drawdawn. we are interested in finding the worst case scenario.

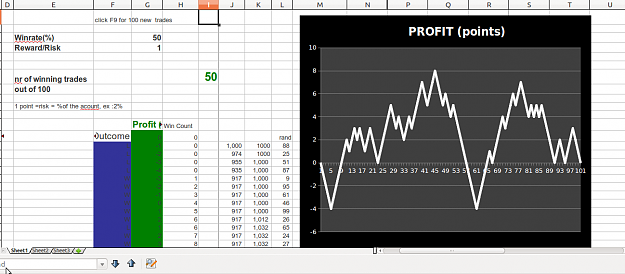

first of all we look at backtest and observe the worst drawdawn there. after that we are going to use the best tool in risk management that i know of: monte carlo simulations. after a big number of trade simulations we will find out the maximum drawdawn in terms of how much we had risked/trade.

i have atached the monte carlo simulator i use which is the file here http://www.forexfactory.com/showthread.php?t=17771 but modified because i think it wasn't calculating the profit right. let's calculate the risk/trade now.

well let's just say that we have D points maximum drawdawn according to simulations. i like to have a safety margin and i say that my system will have stopped working if i have a 1.5 D points drawdawn. so risk/trade will be 30%/(1.5*D). a bigger margin of safety will be D*2 points.

sorry for such a long post. the excel file is simple. type in winrate and reward/risk and have a nice time simulating and finding out the worst case scenario for you.

later edit. the profit formula didn't calculate wright in the file. now it works fine

later edit 2. there is a second simulator i've found that you can use http://www.automated-trading-system....culation-tool/

i am a systematic trader so i like trading statistics. the biggest problem for me was how i can differentiate between normal or big drawdawn and system stopped working scenario and finding the risk/trade so then i can survive bad periods.

i found a solution for this. first of all you must define the system stopped working drawdawn, the maximum drawdawn you will allow yourself to have.

mine is at 30%. you can choose whatever you want...20%,40%

after deciding the maximum (system failed) drawdawn now we analyse the trading system's drawdawn. we are interested in finding the worst case scenario.

first of all we look at backtest and observe the worst drawdawn there. after that we are going to use the best tool in risk management that i know of: monte carlo simulations. after a big number of trade simulations we will find out the maximum drawdawn in terms of how much we had risked/trade.

i have atached the monte carlo simulator i use which is the file here http://www.forexfactory.com/showthread.php?t=17771 but modified because i think it wasn't calculating the profit right. let's calculate the risk/trade now.

well let's just say that we have D points maximum drawdawn according to simulations. i like to have a safety margin and i say that my system will have stopped working if i have a 1.5 D points drawdawn. so risk/trade will be 30%/(1.5*D). a bigger margin of safety will be D*2 points.

sorry for such a long post. the excel file is simple. type in winrate and reward/risk and have a nice time simulating and finding out the worst case scenario for you.

later edit. the profit formula didn't calculate wright in the file. now it works fine

later edit 2. there is a second simulator i've found that you can use http://www.automated-trading-system....culation-tool/

Attached File(s)