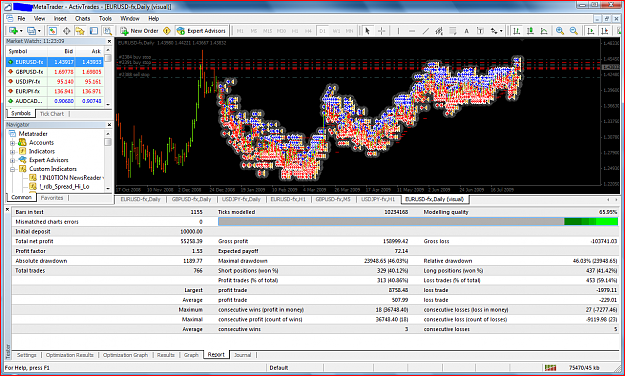

I wrote a couple of week ago on this forum and would like to give an update on my activities writing an ATS.

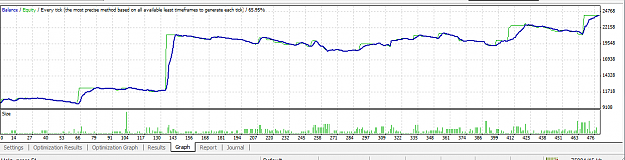

I have Basically been loading tick by tick data in a database(for 8 currencies), allowing it to play back and testing my strategies. Not that much data yet but about 4 months now. I have incorporated a optimizer to allow for validating different stop loss levels. Try not to use the optimizer to avoid curve fitting. I haven't traded with real money yet as I am still in the process of writing different strategies and collecting more data.

Now i devised a simple comparing formula to compare strategies across currencies.

Total Profit/ABSOLUTE(Total Loss).

For this to work there has to be obviously some loss (to avoid division by 0) and quit a bit of data to not get spikes (like a few winners and 1 small looser). The good thing is that you can compare strategies across currencies and independant of units invested. The higher the ratio is i.e less risk for your profit. I find this quite a powerfull comparing method

The best strategy I have been able to come up with is averiging out on around 2 for EUR/USD. (example 4000 usd profit for a total of 2000 loss). This is with a stopLoss of a maximum of 60 pips per transaction.

Mikkon and others could you tell me what you would achieve when using this strategy valuing method. (with realistic stop losses) I want to know if I am expecting to much or if a value of 2 is pretty good.

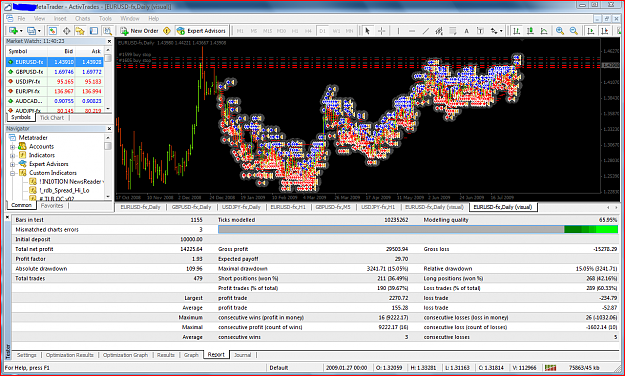

I have Basically been loading tick by tick data in a database(for 8 currencies), allowing it to play back and testing my strategies. Not that much data yet but about 4 months now. I have incorporated a optimizer to allow for validating different stop loss levels. Try not to use the optimizer to avoid curve fitting. I haven't traded with real money yet as I am still in the process of writing different strategies and collecting more data.

Now i devised a simple comparing formula to compare strategies across currencies.

Total Profit/ABSOLUTE(Total Loss).

For this to work there has to be obviously some loss (to avoid division by 0) and quit a bit of data to not get spikes (like a few winners and 1 small looser). The good thing is that you can compare strategies across currencies and independant of units invested. The higher the ratio is i.e less risk for your profit. I find this quite a powerfull comparing method

The best strategy I have been able to come up with is averiging out on around 2 for EUR/USD. (example 4000 usd profit for a total of 2000 loss). This is with a stopLoss of a maximum of 60 pips per transaction.

Mikkon and others could you tell me what you would achieve when using this strategy valuing method. (with realistic stop losses) I want to know if I am expecting to much or if a value of 2 is pretty good.